Advertisement

- Sweden

- /

- Real Estate

- /

- OM:SBB B

Samhällsbyggnadsbolaget i Norden (STO:SBB B) Seems To Be Using A Lot Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Samhällsbyggnadsbolaget i Norden AB (publ) (STO:SBB B) does carry debt. But the real question is whether this debt is making the company risky.

Our free stock report includes 1 warning sign investors should be aware of before investing in Samhällsbyggnadsbolaget i Norden. Read for free now.When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

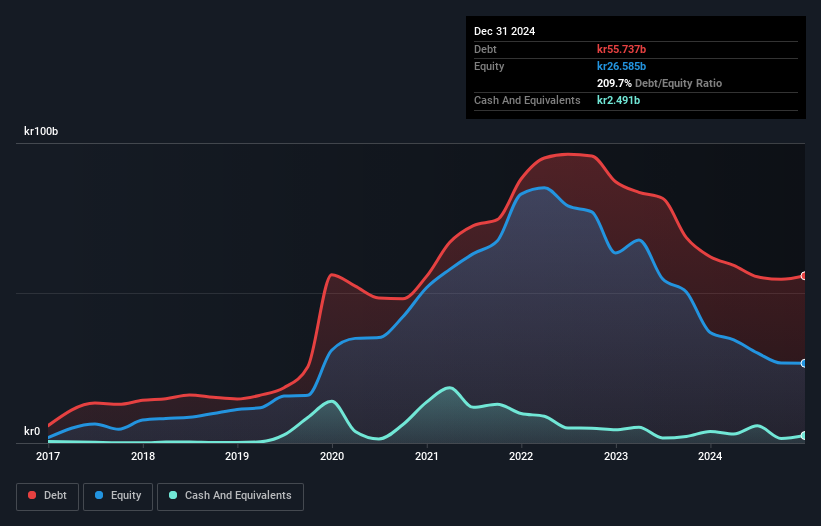

What Is Samhällsbyggnadsbolaget i Norden's Debt?

The image below, which you can click on for greater detail, shows that Samhällsbyggnadsbolaget i Norden had debt of kr55.7b at the end of December 2024, a reduction from kr62.1b over a year. On the flip side, it has kr2.49b in cash leading to net debt of about kr53.2b.

How Strong Is Samhällsbyggnadsbolaget i Norden's Balance Sheet?

We can see from the most recent balance sheet that Samhällsbyggnadsbolaget i Norden had liabilities of kr9.43b falling due within a year, and liabilities of kr50.9b due beyond that. Offsetting these obligations, it had cash of kr2.49b as well as receivables valued at kr1.34b due within 12 months. So its liabilities total kr56.4b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the kr6.39b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Samhällsbyggnadsbolaget i Norden would likely require a major re-capitalisation if it had to pay its creditors today.

Check out our latest analysis for Samhällsbyggnadsbolaget i Norden

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Samhällsbyggnadsbolaget i Norden shareholders face the double whammy of a high net debt to EBITDA ratio (37.2), and fairly weak interest coverage, since EBIT is just 2.3 times the interest expense. This means we'd consider it to have a heavy debt load. Worse, Samhällsbyggnadsbolaget i Norden's EBIT was down 39% over the last year. If earnings keep going like that over the long term, it has a snowball's chance in hell of paying off that debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Samhällsbyggnadsbolaget i Norden's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Samhällsbyggnadsbolaget i Norden recorded free cash flow of 48% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

On the face of it, Samhällsbyggnadsbolaget i Norden's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. After considering the datapoints discussed, we think Samhällsbyggnadsbolaget i Norden has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 1 warning sign for Samhällsbyggnadsbolaget i Norden that you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:SBB B

Samhällsbyggnadsbolaget i Norden

Owns, develops, and manages residential and social infrastructure properties in Sweden, Norway, Finland, and Denmark.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|6.3% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|0.9% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.9% undervalued

ZW

Community Contributor