Advertisement

Market Sentiment Around Loss-Making Lipigon Pharmaceuticals AB (publ) (STO:LPGO)

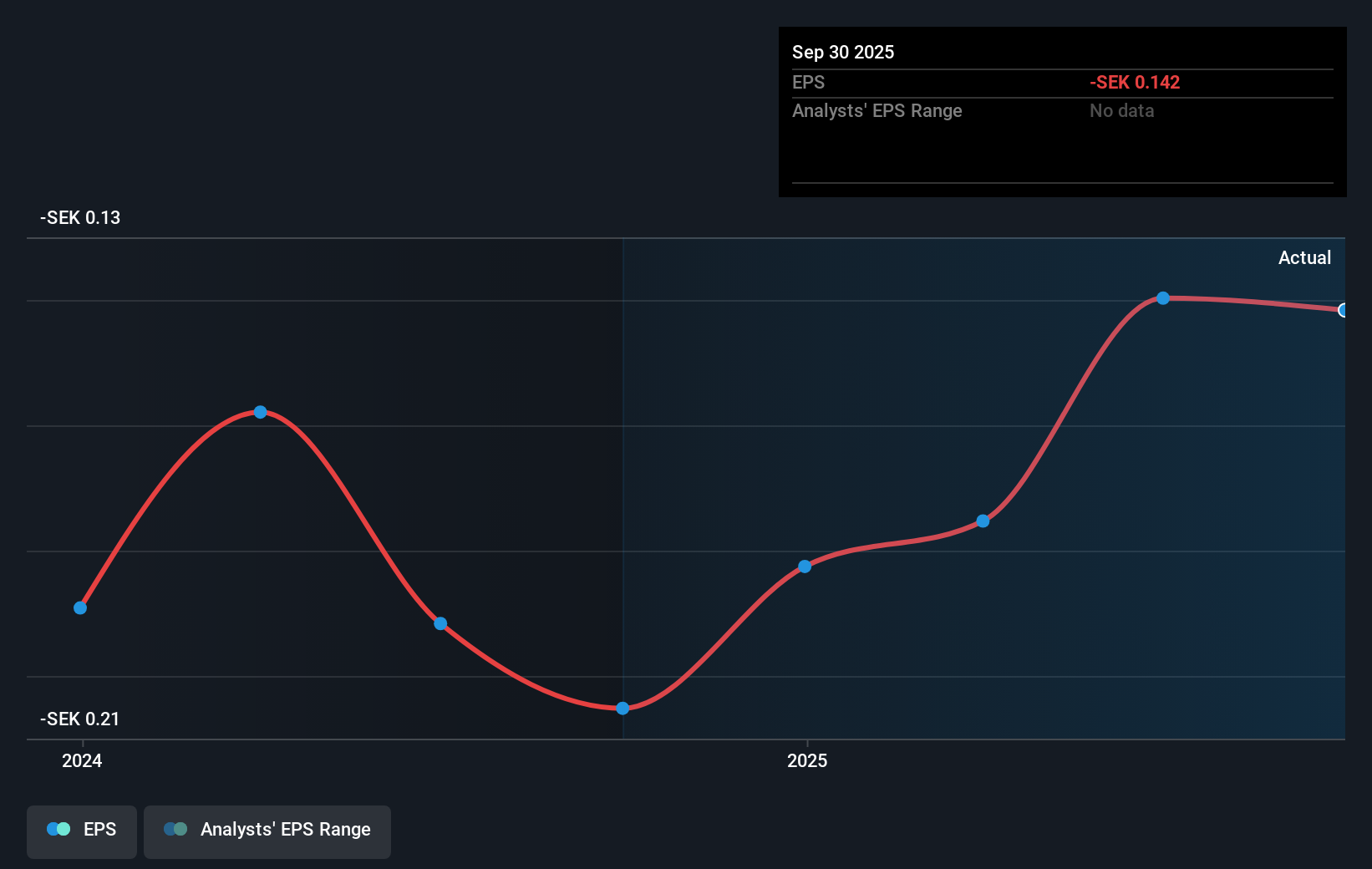

With the business potentially at an important milestone, we thought we'd take a closer look at Lipigon Pharmaceuticals AB (publ)'s (STO:LPGO) future prospects. Lipigon Pharmaceuticals AB (publ) develops drugs for lipid related diseases in Sweden. The company’s loss has recently broadened since it announced a kr25m loss in the full financial year, compared to the latest trailing-twelve-month loss of kr36m, moving it further away from breakeven. Many investors are wondering about the rate at which Lipigon Pharmaceuticals will turn a profit, with the big question being “when will the company breakeven?” In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

According to some industry analysts covering Lipigon Pharmaceuticals, breakeven is near. They anticipate the company to incur a final loss in 2026, before generating positive profits of kr127m in 2027. Therefore, the company is expected to breakeven roughly 2 years from today. In order to meet this breakeven date, we calculated the rate at which the company must grow year-on-year. It turns out an average annual growth rate of 123% is expected, which is extremely buoyant. Should the business grow at a slower rate, it will become profitable at a later date than expected.

Given this is a high-level overview, we won’t go into details of Lipigon Pharmaceuticals' upcoming projects, though, bear in mind that generally a biotech has lumpy cash flows which are contingent on the product type and stage of development the company is in. This means that a high growth rate is not unusual, especially if the company is currently in an investment period.

See our latest analysis for Lipigon Pharmaceuticals

One thing we’d like to point out is that Lipigon Pharmaceuticals has no debt on its balance sheet, which is quite unusual for a cash-burning biotech, which typically has high debt relative to its equity. This means that the company has been operating purely on its equity investment and has no debt burden. This aspect reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of Lipigon Pharmaceuticals to cover in one brief article, but the key fundamentals for the company can all be found in one place – Lipigon Pharmaceuticals' company page on Simply Wall St. We've also compiled a list of important factors you should further examine:

- Historical Track Record: What has Lipigon Pharmaceuticals' performance been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Lipigon Pharmaceuticals' board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LPGO

Lipigon Pharmaceuticals

Develops drugs for lipid related diseases in Sweden.

High growth potential with moderate risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1161.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative