Advertisement

We Think AlzeCure Pharma (STO:ALZCUR) Can Afford To Drive Business Growth

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

Given this risk, we thought we'd take a look at whether AlzeCure Pharma (STO:ALZCUR) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

Check out our latest analysis for AlzeCure Pharma

Does AlzeCure Pharma Have A Long Cash Runway?

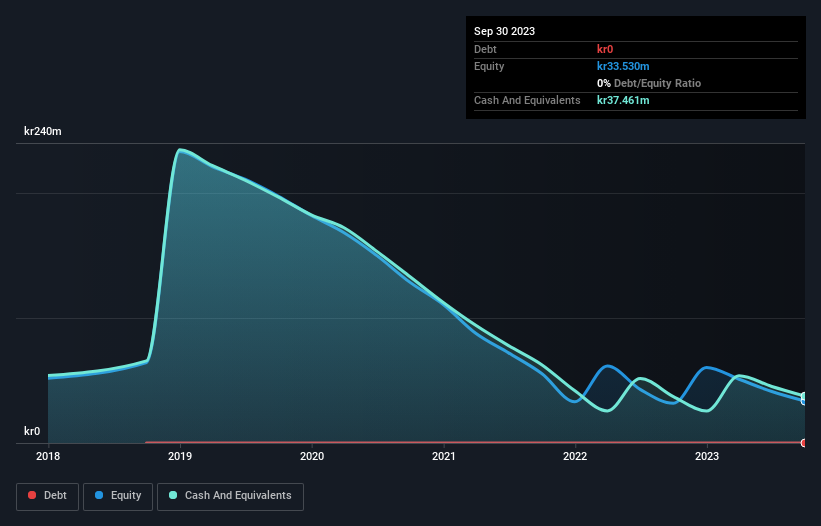

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In September 2023, AlzeCure Pharma had kr37m in cash, and was debt-free. Looking at the last year, the company burnt through kr40m. Therefore, from September 2023 it had roughly 11 months of cash runway. Notably, however, the one analyst we see covering the stock thinks that AlzeCure Pharma will break even (at a free cash flow level) before then. In that case, it may never reach the end of its cash runway. You can see how its cash balance has changed over time in the image below.

How Is AlzeCure Pharma's Cash Burn Changing Over Time?

AlzeCure Pharma didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. As it happens, the company's cash burn reduced by 43% over the last year, which suggests that management are mindful of the possibility of running out of cash. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Easily Can AlzeCure Pharma Raise Cash?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for AlzeCure Pharma to raise more cash in the future. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

AlzeCure Pharma has a market capitalisation of kr209m and burnt through kr40m last year, which is 19% of the company's market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

How Risky Is AlzeCure Pharma's Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way AlzeCure Pharma is burning through its cash. In particular, we think its cash burn reduction stands out as evidence that the company is well on top of its spending. Although its cash runway does give us reason for pause, the other metrics we discussed in this article form a positive picture overall. It's clearly very positive to see that at least one analyst is forecasting the company will break even fairly soon. Considering all the factors discussed in this article, we're not overly concerned about the company's cash burn, although we do think shareholders should keep an eye on how it develops. On another note, we conducted an in-depth investigation of the company, and identified 5 warning signs for AlzeCure Pharma (1 is concerning!) that you should be aware of before investing here.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:ALZCUR

AlzeCure Pharma

Operates as a pharmaceutical company that develops drug therapies for the treatment of severe diseases and conditions that affect the central nervous system.

High growth potential moderate.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor