Advertisement

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Lovisagruvan (NGM:LOVI). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

Check out our latest analysis for Lovisagruvan

How Quickly Is Lovisagruvan Increasing Earnings Per Share?

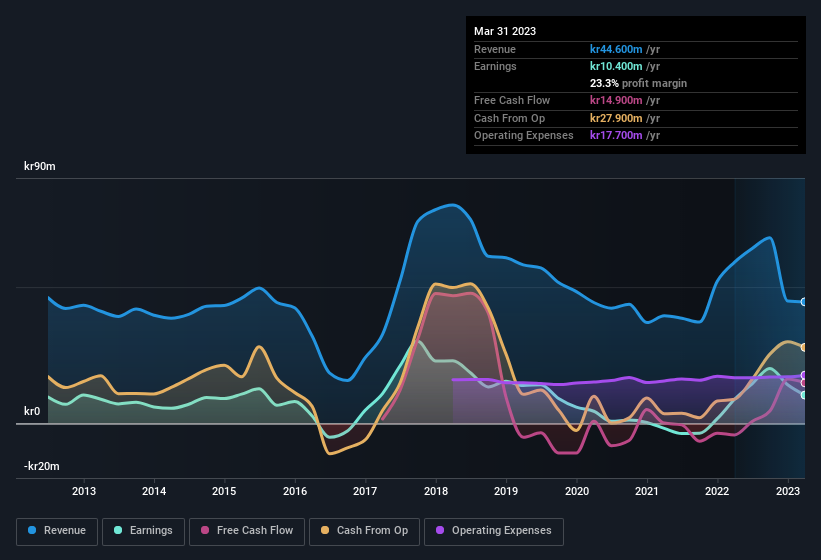

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That makes EPS growth an attractive quality for any company. Shareholders will be happy to know that Lovisagruvan's EPS has grown 32% each year, compound, over three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be beaming.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Lovisagruvan's EBIT margins have actually improved by 12.9 percentage points in the last year, to reach 32%, but, on the flip side, revenue was down 25%. That falls short of ideal.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

Lovisagruvan isn't a huge company, given its market capitalisation of kr131m. That makes it extra important to check on its balance sheet strength.

Are Lovisagruvan Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

One positive for Lovisagruvan, is that company insiders spent kr151k acquiring shares in the last year. While this investment may be modest, it is great considering the lack of insider selling. We also note that it was the Director, Johan Wiklund, who made the biggest single acquisition, paying kr74k for shares at about kr36.83 each.

These recent buys aren't the only encouraging sign for shareholders, as a look at the shareholder registry for Lovisagruvan will reveal that insiders own a significant piece of the pie. In fact, they own 43% of the shares, making insiders a very influential shareholder group. Those who are comforted by solid insider ownership like this should be happy, as it implies that those running the business are genuinely motivated to create shareholder value. Although, with Lovisagruvan being valued at kr131m, this is a small company we're talking about. So despite a large proportional holding, insiders only have kr56m worth of stock. That might not be a huge sum but it should be enough to keep insiders motivated!

Should You Add Lovisagruvan To Your Watchlist?

For growth investors, Lovisagruvan's raw rate of earnings growth is a beacon in the night. Furthermore, company insiders have been adding to their significant stake in the company. These things considered, this is one stock worth watching. Even so, be aware that Lovisagruvan is showing 5 warning signs in our investment analysis , and 1 of those is concerning...

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Lovisagruvan, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NGM:LOVI

Lovisagruvan

Lovisagruvan AB (publ) engages in the mining activities in Sweden.

Unattractive dividend payer and overvalued.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor