European Growth Companies With High Insider Ownership In April 2025

Reviewed by Simply Wall St

As European markets navigate a challenging landscape marked by new trade tariffs and economic uncertainties, investors are increasingly seeking companies that demonstrate resilience and potential for growth. In this environment, growth companies with high insider ownership can be particularly appealing, as they often indicate strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Elicera Therapeutics (OM:ELIC) | 27.8% | 97.2% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Bergen Carbon Solutions (OB:BCS) | 12% | 50.8% |

| XTPL (WSE:XTP) | 27.9% | 118% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| CD Projekt (WSE:CDR) | 29.7% | 36.8% |

| Ortoma (OM:ORT B) | 27.7% | 68.6% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Circus (XTRA:CA1) | 26% | 51.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

P/F Bakkafrost (OB:BAKKA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: P/F Bakkafrost, along with its subsidiaries, is engaged in the production and sale of salmon products across North America, Western Europe, Eastern Europe, Asia, and other international markets; it has a market cap of NOK29.34 billion.

Operations: The company generates revenue from various segments, including Sales and Other (DKK10.21 billion), Farming Faroe Islands (DKK3.97 billion), Fishmeal, Oil and Feed (DKK2.73 billion), Farming Scotland (DKK1.84 billion), Services (DKK894.61 million), Freshwater Faroe Islands (DKK782.05 million), and Freshwater Scotland (DKK117.26 million).

Insider Ownership: 13.3%

Earnings Growth Forecast: 36.6% p.a.

P/F Bakkafrost, a company with significant insider ownership, has demonstrated mixed financial performance recently. Although its net income decreased to DKK 656.6 million from DKK 955.57 million year-on-year, the company's earnings are forecasted to grow significantly by 36.55% annually, outpacing the Norwegian market's growth rate of 7.9%. Despite trading at a substantial discount to its estimated fair value and experiencing lower profit margins than last year, revenue is expected to increase by 13.5% annually.

- Unlock comprehensive insights into our analysis of P/F Bakkafrost stock in this growth report.

- Our valuation report unveils the possibility P/F Bakkafrost's shares may be trading at a discount.

RaySearch Laboratories (OM:RAY B)

Simply Wall St Growth Rating: ★★★★★☆

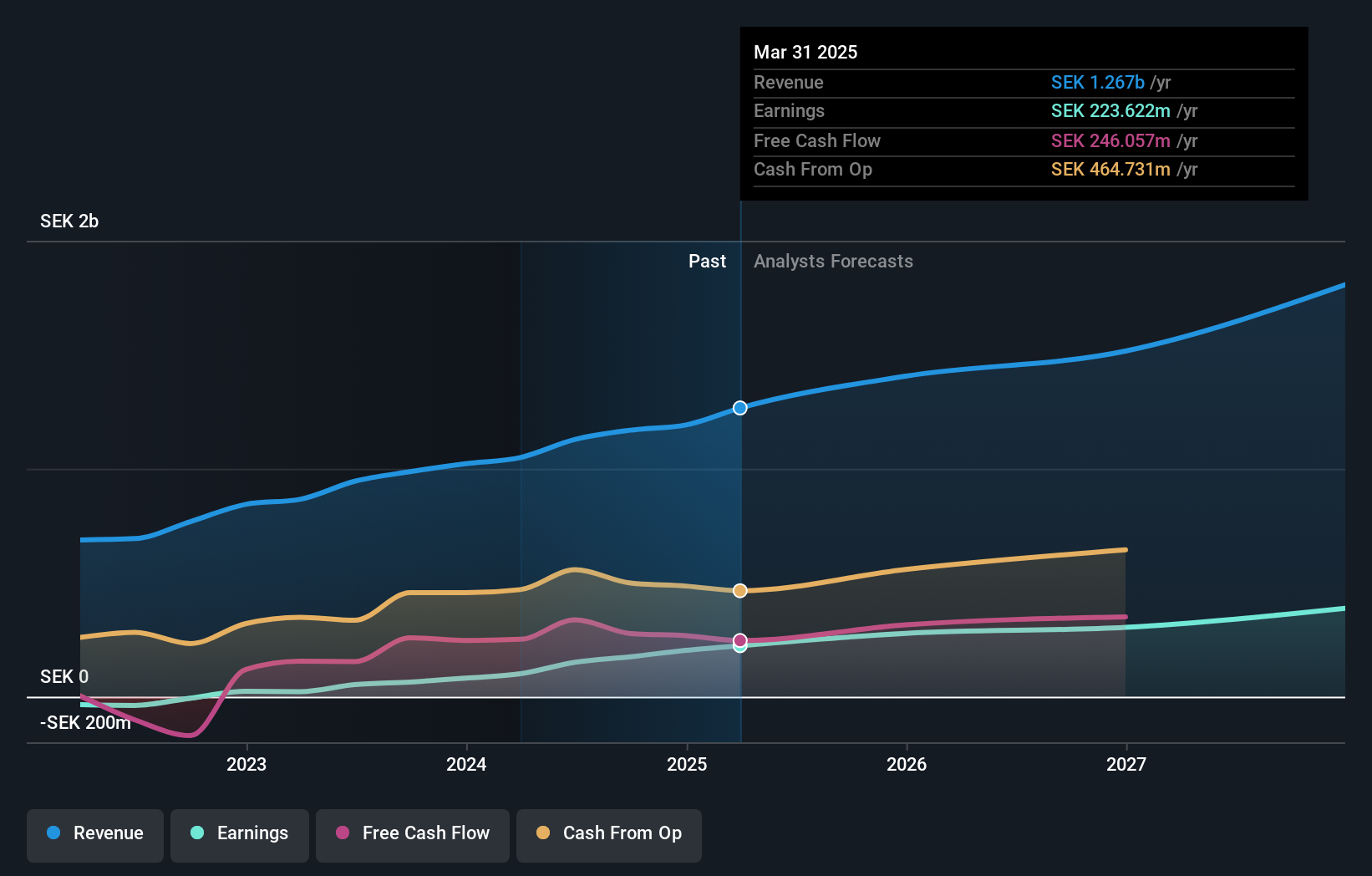

Overview: RaySearch Laboratories AB (publ) is a medical technology company that offers software solutions for cancer care across various regions including the Americas, Europe, Africa, the Asia-Pacific, and the Middle East, with a market cap of SEK7.71 billion.

Operations: The company's revenue primarily comes from its healthcare software segment, which generated SEK1.19 billion.

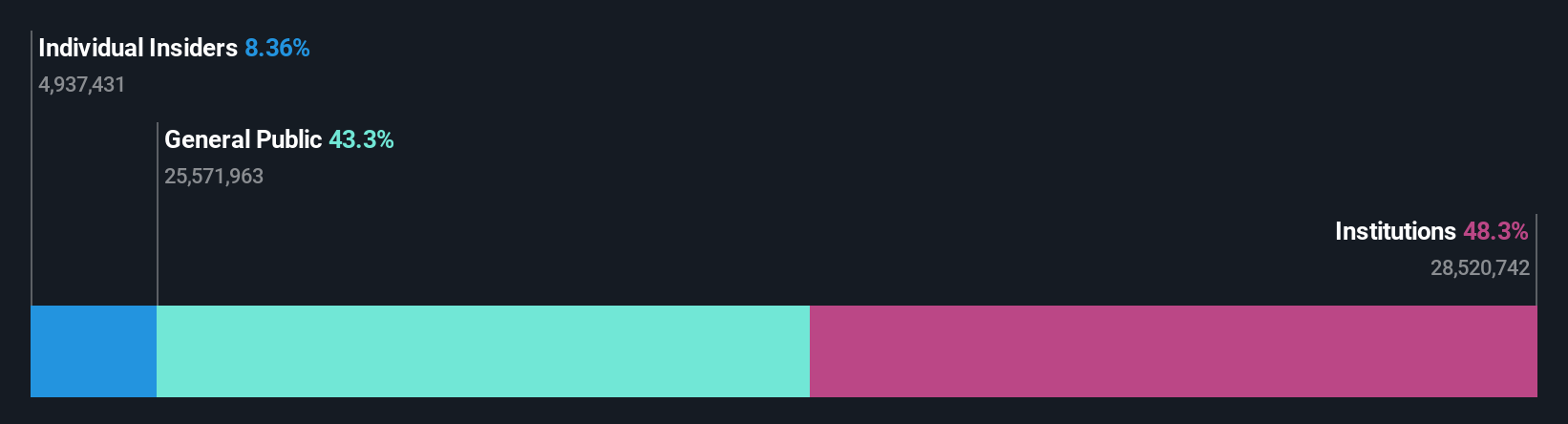

Insider Ownership: 17.8%

Earnings Growth Forecast: 23.7% p.a.

RaySearch Laboratories, with high insider ownership, is experiencing robust growth prospects. Earnings are expected to grow at 23.7% annually, surpassing the Swedish market's rate of 9.1%. Recent financials show a net income increase to SEK 60 million from SEK 31.54 million year-on-year, supported by significant orders like the RMB 51 million deal with Heyou Hospital in China. Despite substantial insider selling recently, the company's strategic positioning in particle treatment planning strengthens its competitive edge.

- Click here and access our complete growth analysis report to understand the dynamics of RaySearch Laboratories.

- Our expertly prepared valuation report RaySearch Laboratories implies its share price may be too high.

Shoper (WSE:SHO)

Simply Wall St Growth Rating: ★★★★★☆

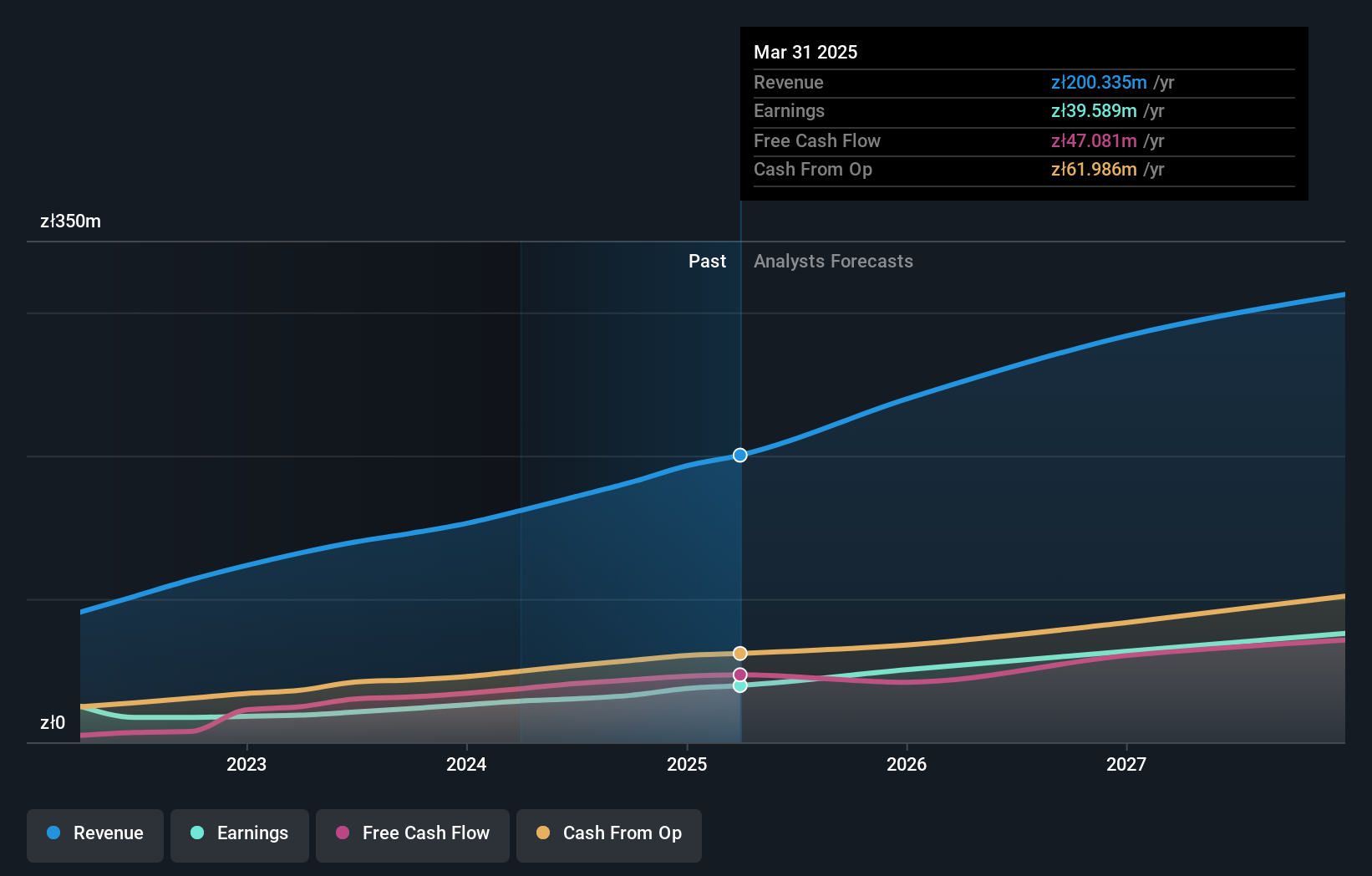

Overview: Shoper SA offers Software as a Service solutions for e-commerce in Poland, with a market capitalization of PLN1.13 billion.

Operations: The company's revenue is derived from two main segments: Solutions, contributing PLN141.44 million, and Subscriptions, accounting for PLN39.87 million.

Insider Ownership: 23.6%

Earnings Growth Forecast: 26.6% p.a.

Shoper's earnings are projected to grow significantly at 26.6% annually, outpacing the Polish market's 12.8% rate, although revenue growth is slower at 14.8%. The stock trades at a discount of 24.4% below its estimated fair value, with analysts expecting a price rise of 26.7%. Despite no recent insider trading activity, Shoper maintains strong financial health and high insider ownership, with its Return on Equity forecasted to reach a very high level of 55.2%.

- Dive into the specifics of Shoper here with our thorough growth forecast report.

- Our valuation report here indicates Shoper may be undervalued.

Where To Now?

- Investigate our full lineup of 237 Fast Growing European Companies With High Insider Ownership right here.

- Searching for a Fresh Perspective? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:BAKKA

P/F Bakkafrost

Produces and sells salmon products in North America, Western Europe, Eastern Europe, Asia, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives