Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that iZafe Group AB (publ) (STO:IZAFE B) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for iZafe Group

What Is iZafe Group's Net Debt?

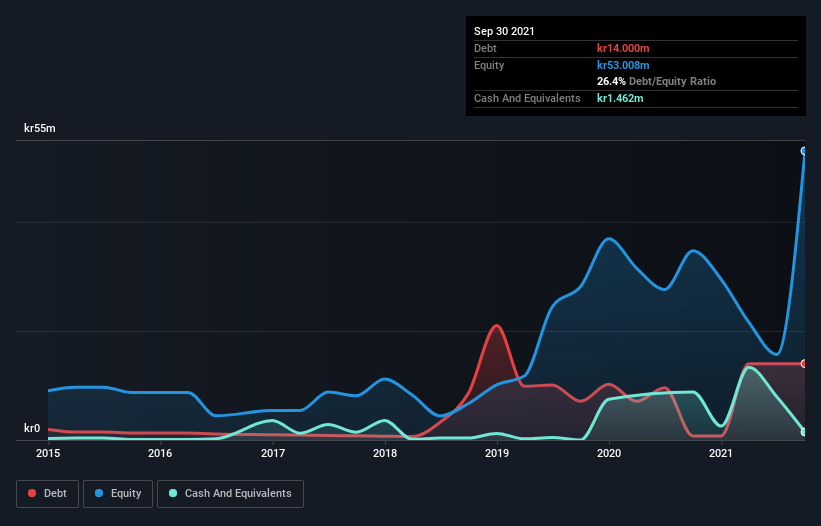

The image below, which you can click on for greater detail, shows that at September 2021 iZafe Group had debt of kr14.0m, up from kr750.0k in one year. However, because it has a cash reserve of kr1.46m, its net debt is less, at about kr12.5m.

How Healthy Is iZafe Group's Balance Sheet?

The latest balance sheet data shows that iZafe Group had liabilities of kr28.1m due within a year, and liabilities of kr3.96m falling due after that. Offsetting this, it had kr1.46m in cash and kr54.5m in receivables that were due within 12 months. So it can boast kr23.8m more liquid assets than total liabilities.

This excess liquidity is a great indication that iZafe Group's balance sheet is almost as strong as Fort Knox. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. There's no doubt that we learn most about debt from the balance sheet. But it is iZafe Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

It seems likely shareholders hope that iZafe Group can significantly advance the business plan before too long, because it doesn't have any significant revenue at the moment.

Caveat Emptor

Not only did iZafe Group's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable kr30m at the EBIT level. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. This one is a bit too risky for our liking. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 6 warning signs for iZafe Group (5 shouldn't be ignored) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if iZafe Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:IZAFE B

iZafe Group

A medical technology company, engages in the research, development, and marketing of digital medical solutions and services for safer drug management at home.

Moderate with imperfect balance sheet.

Market Insights

Community Narratives