David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Inission AB (publ) (STO:INISS B) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Inission

What Is Inission's Debt?

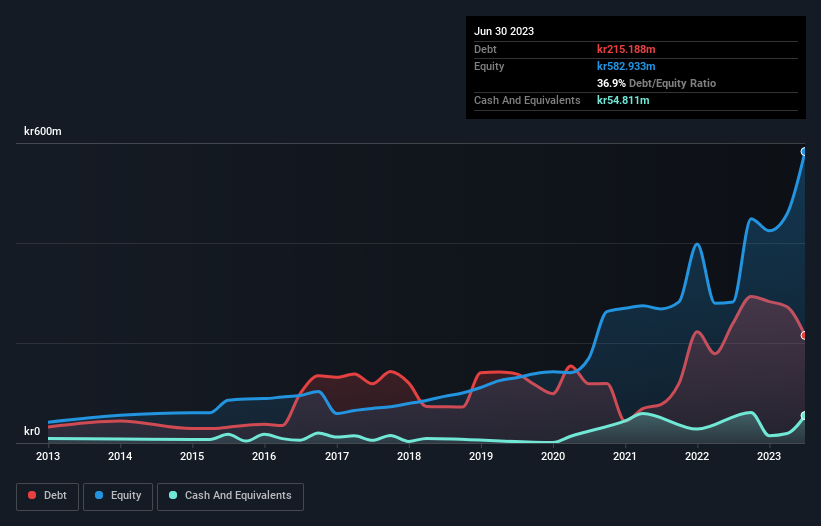

You can click the graphic below for the historical numbers, but it shows that Inission had kr215.2m of debt in June 2023, down from kr239.2m, one year before. On the flip side, it has kr54.8m in cash leading to net debt of about kr160.4m.

How Healthy Is Inission's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Inission had liabilities of kr836.3m due within 12 months and liabilities of kr324.7m due beyond that. Offsetting this, it had kr54.8m in cash and kr325.3m in receivables that were due within 12 months. So its liabilities total kr781.0m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of kr1.09b, so it does suggest shareholders should keep an eye on Inission's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Inission's low debt to EBITDA ratio of 0.80 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 5.1 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Pleasingly, Inission is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 17,715% gain in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Inission can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Inission's free cash flow amounted to 26% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

When it comes to the balance sheet, the standout positive for Inission was the fact that it seems able to grow its EBIT confidently. However, our other observations weren't so heartening. For instance it seems like it has to struggle a bit to handle its total liabilities. Looking at all this data makes us feel a little cautious about Inission's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example - Inission has 2 warning signs we think you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:INISS B

Inission

Engages in the supply of tailored manufacturing services and products in the field of industrial electronics and mechanics in Sweden, Finland, Estonia, Norway, the United States, and internationally.

Undervalued with adequate balance sheet.