Advertisement

- Saudi Arabia

- /

- Telecom Services and Carriers

- /

- SASE:7040

Exploring Undiscovered Gems With Potential For November 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate geopolitical tensions and economic uncertainties, smaller-cap indexes have shown resilience, outperforming their larger counterparts amid broad-based gains in major stock indices. With positive sentiment buoyed by strong labor market indicators and stabilizing mortgage rates, investors are increasingly interested in identifying promising opportunities within the small-cap space. In this environment, a good stock is often characterized by its ability to leverage prevailing economic trends while maintaining robust fundamentals that can withstand market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Marítima de Inversiones | NA | 82.67% | 21.14% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Segar Kumala Indonesia | NA | 21.81% | 18.21% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Watt's | 73.27% | 7.85% | -1.33% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Bhakti Multi Artha | 45.21% | 32.37% | -16.43% | ★★★★☆☆ |

| Krom Bank Indonesia | NA | 40.04% | 35.44% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

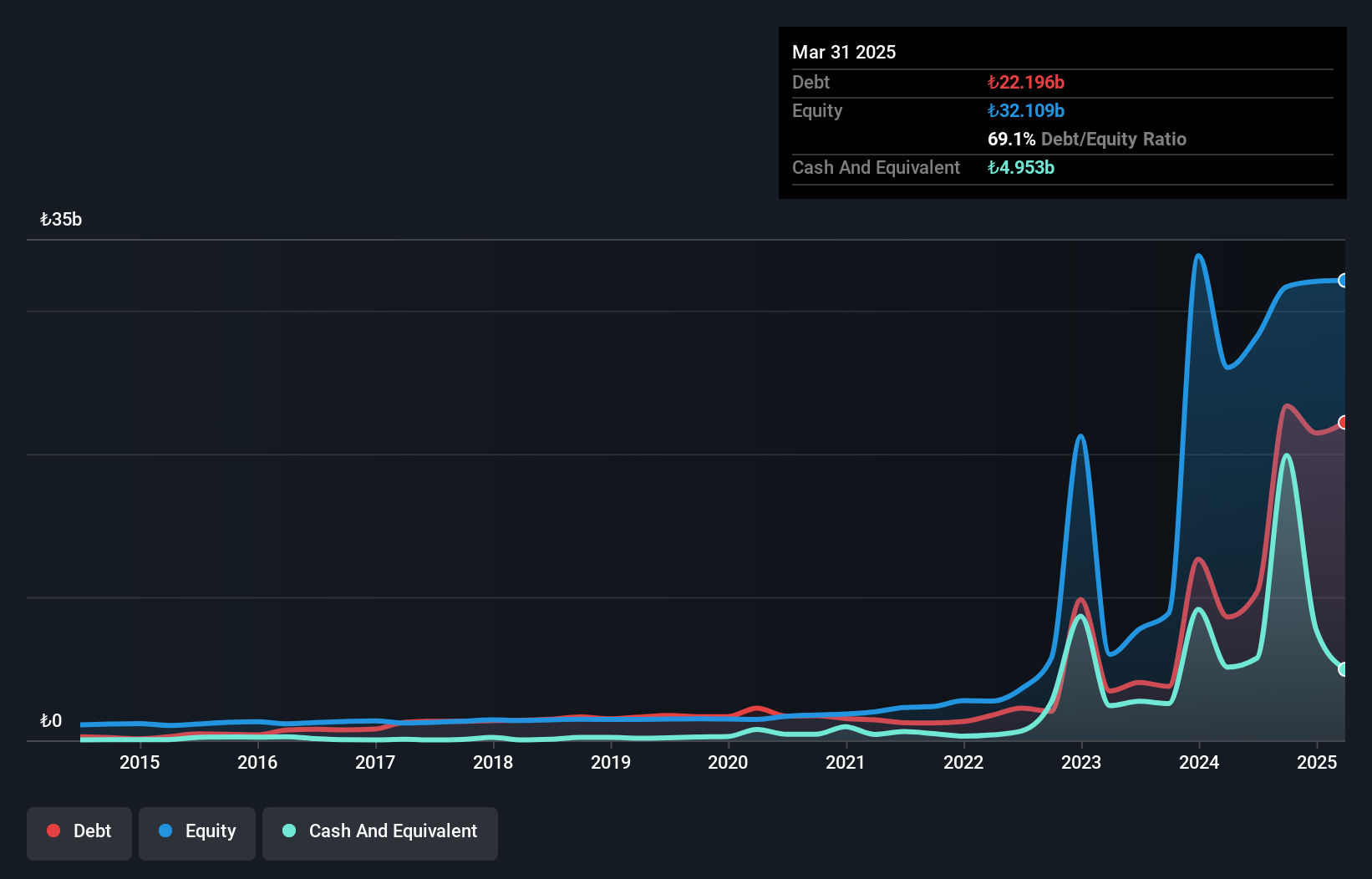

Çimsa Çimento Sanayi ve Ticaret (IBSE:CIMSA)

Simply Wall St Value Rating: ★★★★★★

Overview: Çimsa Çimento Sanayi ve Ticaret A.S. is a Turkish company involved in the production and sale of cement and building materials, with a market capitalization of TRY37.96 billion.

Operations: Çimsa derives its revenue primarily from cement sales, contributing TRY14.78 billion, and ready-mixed concrete sales, adding TRY4.20 billion. The company's net profit margin reflects key financial performance indicators in its sector.

Çimsa Çimento, a notable player in the cement industry, has shown impressive financial growth. Over the past year, earnings surged by 30%, outpacing the Basic Materials industry's 19%. The company's net debt to equity ratio stands at a satisfactory 11%, having decreased from 110% over five years. Recent earnings reports highlight robust performance with third-quarter net income soaring to TRY 1.16 billion from TRY 0.46 million last year, and EPS climbing to TRY 1.23 from TRY 0.0005. Despite sales dipping slightly, Çimsa's strong profitability and favorable debt metrics suggest promising prospects ahead.

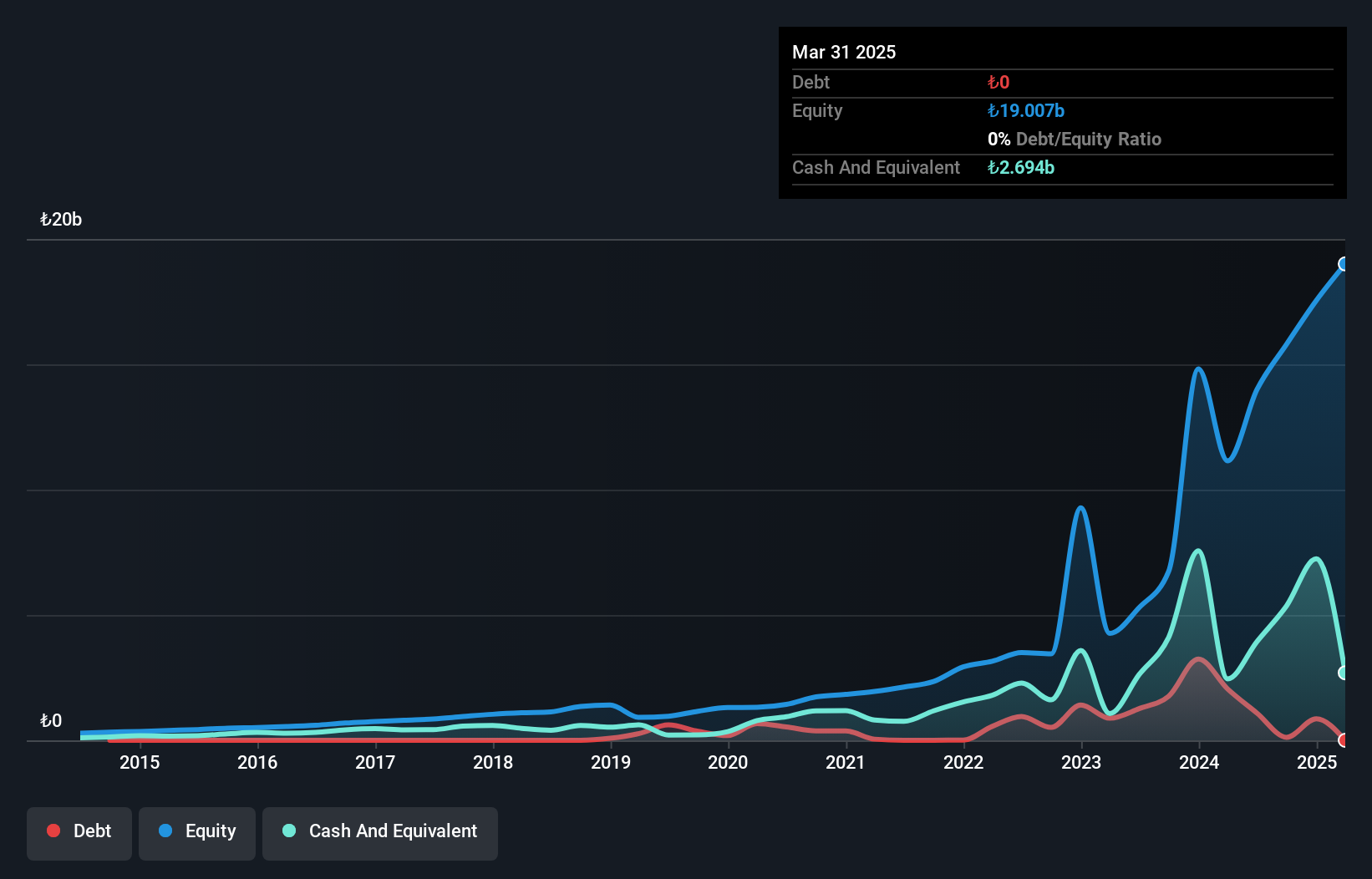

Türk Tuborg Bira ve Malt Sanayii (IBSE:TBORG)

Simply Wall St Value Rating: ★★★★★★

Overview: Türk Tuborg Bira ve Malt Sanayii A.S. is engaged in the production, sale, and distribution of beer and malt both within Turkey and internationally, with a market capitalization of TRY42.02 billion.

Operations: Türk Tuborg generates revenue primarily from its alcoholic beverages segment, amounting to TRY20.78 billion. The company's net profit margin reflects its profitability trends over time.

Türk Tuborg, a notable player in the beverage industry, has demonstrated impressive financial performance with earnings growth of 90.5% over the past year, outpacing the industry's 12.4%. The company reported third-quarter sales of TRY 8.65 billion and net income of TRY 1.69 billion, reflecting strong operational results compared to last year's figures. With a debt-to-equity ratio reduced to just 0.8% from 30.8% over five years and more cash than total debt, its financial health appears robust despite recent share price volatility. Earnings per share have also risen significantly to TRY 5.23 from TRY 2.33 a year ago, highlighting profitability improvements.

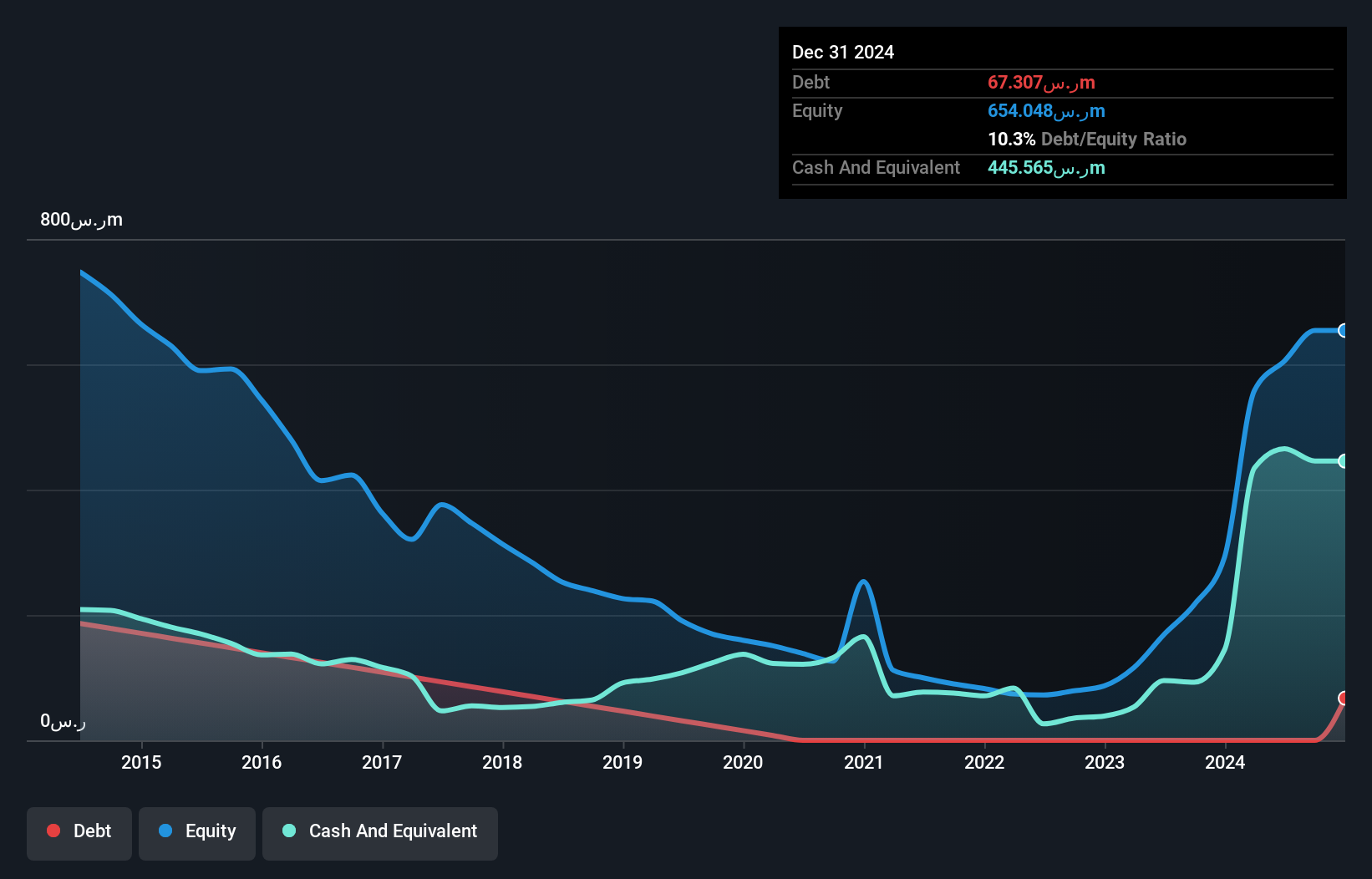

Etihad Atheeb Telecommunication (SASE:7040)

Simply Wall St Value Rating: ★★★★★★

Overview: Etihad Atheeb Telecommunication Company offers telecommunication products and services to individuals and businesses both within the Kingdom of Saudi Arabia and internationally, with a market cap of SAR3.97 billion.

Operations: The company's revenue is primarily derived from data services, generating SAR729.22 million, followed by voice services at SAR499.77 million.

Etihad Atheeb Telecommunication, a relatively small player in the telecom industry, is showing strong financial health with no debt compared to five years ago when its debt-to-equity ratio was 13.7%. The company reported a notable earnings growth of 44.6% over the past year, outpacing the industry's 1.3%, and has been trading at 73.5% below its estimated fair value. Recent results highlight sales of SAR346 million for Q2 2024, up from SAR238 million last year, while net income rose to SAR59 million from SAR48 million, reflecting robust operational performance despite substantial shareholder dilution recently.

Taking Advantage

- Click this link to deep-dive into the 4634 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Etihad Atheeb Telecommunication might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:7040

Etihad Atheeb Telecommunication

Provides telecommunication products and services for individuals and businesses in the Kingdom of Saudi Arabia and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor