Advertisement

- Saudi Arabia

- /

- Specialty Stores

- /

- SASE:4240

Fawaz Abdulaziz Al Hokair & Company (TADAWUL:4240) Analysts Just Trimmed Their Revenue Forecasts By 12%

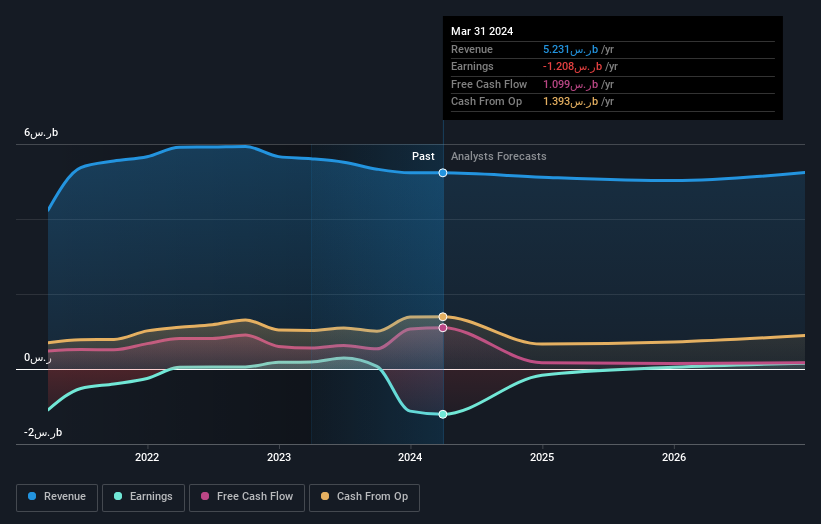

Today is shaping up negative for Fawaz Abdulaziz Al Hokair & Company (TADAWUL:4240) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Revenue estimates were cut sharply as the analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

Following the latest downgrade, the current consensus, from the six analysts covering Fawaz Abdulaziz Al Hokair, is for revenues of ر.س5.1b in 2024, which would reflect a small 2.2% reduction in Fawaz Abdulaziz Al Hokair's sales over the past 12 months. Before the latest update, the analysts were foreseeing ر.س5.8b of revenue in 2024. It looks like forecasts have become a fair bit less optimistic on Fawaz Abdulaziz Al Hokair, given the substantial drop in revenue estimates.

See our latest analysis for Fawaz Abdulaziz Al Hokair

Notably, the analysts have cut their price target 18% to ر.س12.72, suggesting concerns around Fawaz Abdulaziz Al Hokair's valuation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Fawaz Abdulaziz Al Hokair's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with a forecast 2.9% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 2.4% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 9.5% annually for the foreseeable future. It's pretty clear that Fawaz Abdulaziz Al Hokair's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They're also anticipating slower revenue growth than the wider market. Furthermore, there was a cut to the price target, suggesting that the latest news has led to more pessimism about the intrinsic value of the business. Given the stark change in sentiment, we'd understand if investors became more cautious on Fawaz Abdulaziz Al Hokair after today.

That said, the analysts might have good reason to be negative on Fawaz Abdulaziz Al Hokair, given a weak balance sheet. Learn more, and discover the 2 other risks we've identified, for free on our platform here.

You can also see our analysis of Fawaz Abdulaziz Al Hokair's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4240

Fawaz Abdulaziz Al Hokair

Operates as a franchise retailer of fashion products in the Kingdom of Saudi Arabia, Jordan, Egypt, the Republic of Kazakhstan, the United States, the Republic of Azerbaijan, Georgia, Armenia, and Morocco.

Reasonable growth potential slight.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor