Advertisement

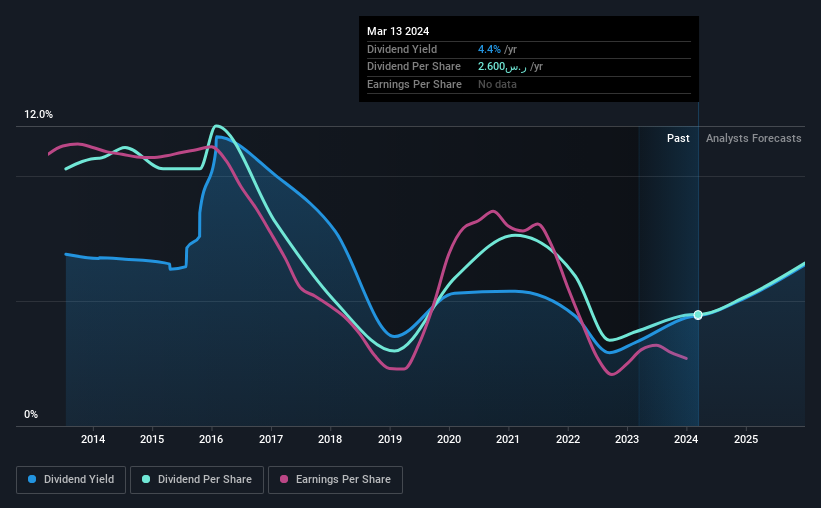

Qassim Cement Company (TADAWUL:3040) will pay a dividend of SAR0.65 on the 4th of April. This takes the annual payment to 4.4% of the current stock price, which is about average for the industry.

View our latest analysis for Qassim Cement

Qassim Cement Doesn't Earn Enough To Cover Its Payments

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Before this announcement, Qassim Cement was paying out 165% of what it was earning, and not generating any free cash flows either. This high of a dividend payment could start to put pressure on the balance sheet in the future.

Over the next year, EPS is forecast to expand by 25.7%. However, if the dividend continues along recent trends, it could start putting pressure on the balance sheet with the payout ratio reaching 117% over the next year.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2014, the annual payment back then was SAR6.00, compared to the most recent full-year payment of SAR2.60. This works out to be a decline of approximately 8.0% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

Qassim Cement May Find It Hard To Grow The Dividend

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Earnings has been rising at 3.3% per annum over the last five years, which admittedly is a bit slow. The earnings growth is anaemic, and the company is paying out 165% of its profit. Limited recent earnings growth and a high payout ratio makes it hard for us to envision strong future dividend growth, unless the company should have substantial pricing power or some form of competitive advantage.

Qassim Cement's Dividend Doesn't Look Sustainable

In summary, while it's always good to see the dividend being raised, we don't think Qassim Cement's payments are rock solid. The payments are bit high to be considered sustainable, and the track record isn't the best. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've identified 3 warning signs for Qassim Cement (2 are a bit concerning!) that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Qassim Cement might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:3040

Qassim Cement

Engages in the manufacture and selling of cement in the Kingdom of Saudi Arabia.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor