Advertisement

- Japan

- /

- Professional Services

- /

- TSE:6028

3 Global Stocks Estimated To Be 34.7% To 49.9% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

In the midst of heightened uncertainty and mixed economic signals, global markets have shown resilience with U.S. stocks closing higher and European indices snapping a streak of losses. As investors navigate this complex landscape, identifying undervalued stocks becomes crucial; these are companies whose market prices fall significantly below their intrinsic value, offering potential opportunities for growth even amid fluctuating market conditions.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Absolent Air Care Group (OM:ABSO) | SEK256.00 | SEK508.82 | 49.7% |

| RACCOON HOLDINGS (TSE:3031) | ¥957.00 | ¥1890.86 | 49.4% |

| Romsdal Sparebank (OB:ROMSB) | NOK130.70 | NOK258.18 | 49.4% |

| TechnoPro Holdings (TSE:6028) | ¥3306.00 | ¥6593.98 | 49.9% |

| S Foods (TSE:2292) | ¥2556.00 | ¥5084.09 | 49.7% |

| Bide Pharmatech (SHSE:688073) | CN¥54.00 | CN¥106.91 | 49.5% |

| APAC Realty (SGX:CLN) | SGD0.43 | SGD0.85 | 49.4% |

| ALUX (KOSDAQ:A475580) | ₩11250.00 | ₩22243.70 | 49.4% |

| dormakaba Holding (SWX:DOKA) | CHF684.00 | CHF1352.22 | 49.4% |

| Dino Polska (WSE:DNP) | PLN445.20 | PLN887.95 | 49.9% |

Here's a peek at a few of the choices from the screener.

Megacable Holdings S. A. B. de C. V (BMV:MEGA CPO)

Overview: Megacable Holdings S. A. B. de C. V., along with its subsidiaries, operates in the installation, operation, and maintenance of cable television, internet, and telephone signal distribution systems with a market cap of MX$37.09 billion.

Operations: Revenue segments for Megacable Holdings include cable television, internet, and telephone signal distribution systems.

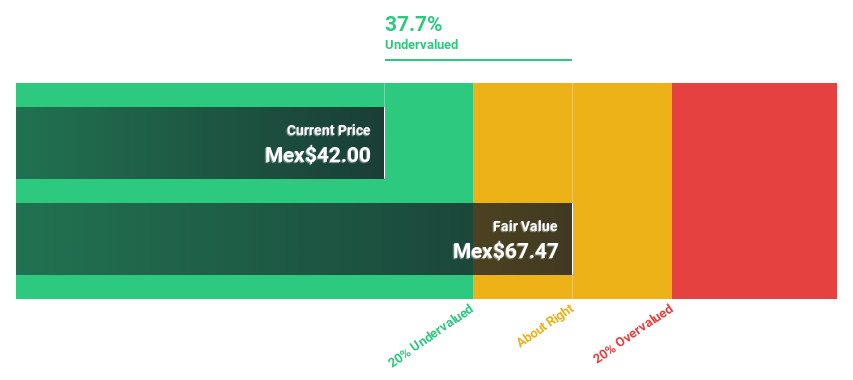

Estimated Discount To Fair Value: 36.1%

Megacable Holdings S. A. B. de C. V., trading at MX$43.2, is significantly undervalued based on discounted cash flow analysis with a fair value estimate of MX$67.59, representing a 36% discount to its intrinsic value. Despite low forecasted return on equity and inadequate interest coverage, projected earnings growth of 20.8% annually outpaces the Mexican market average, suggesting potential for substantial future cash flows despite recent declines in net income and earnings per share.

- Our growth report here indicates Megacable Holdings S. A. B. de C. V may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of Megacable Holdings S. A. B. de C. V stock in this financial health report.

Saudi Kayan Petrochemical (SASE:2350)

Overview: Saudi Kayan Petrochemical Company manufactures and sells chemicals, polymers, and specialty products, with a market cap of SAR9 billion.

Operations: The company's revenue is primarily derived from its petrochemicals segment, totaling SAR8.73 billion.

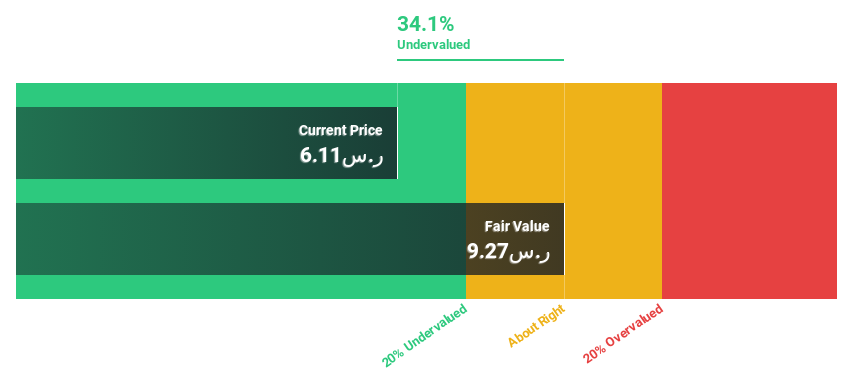

Estimated Discount To Fair Value: 34.7%

Saudi Kayan Petrochemical, trading at SAR6.04, is undervalued with a fair value estimate of SAR9.25, offering a 34.7% discount to intrinsic value. Despite low forecasted return on equity and recent net losses of SAR1.8 billion, the company is expected to achieve profitability within three years and grow earnings by 76.84% annually, outpacing average market growth and suggesting potential for improved cash flows relative to peers in the industry.

- Upon reviewing our latest growth report, Saudi Kayan Petrochemical's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Saudi Kayan Petrochemical.

TechnoPro Holdings (TSE:6028)

Overview: TechnoPro Holdings, Inc. operates as a temporary staffing and contract work company both in Japan and internationally, with a market cap of ¥341.33 billion.

Operations: The company's revenue segments include ¥17.83 billion from R&D Outsourcing Business, ¥24.46 billion from Construction Management Outsourcing, and ¥4.83 billion from Domestic Other Business, along with ¥25.42 billion generated by Overseas Businesses.

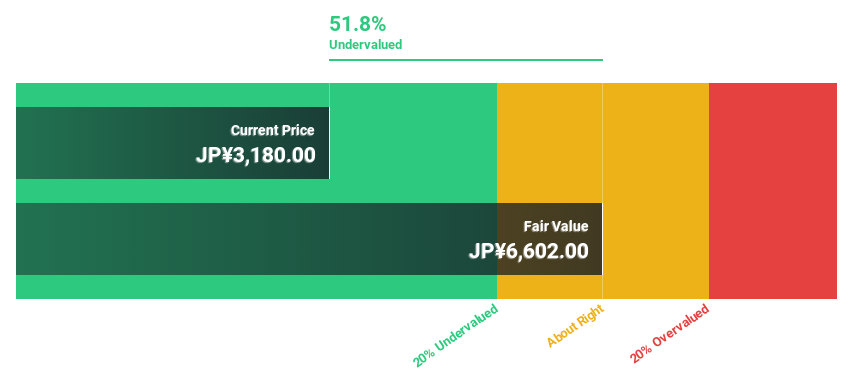

Estimated Discount To Fair Value: 49.9%

TechnoPro Holdings is trading at ¥3,306, significantly undervalued with a fair value estimate of ¥6,593.98, reflecting a discount of over 20%. Despite an unstable dividend track record, the company declared an interim dividend of JPY 30.00 per share and reaffirmed year-end guidance of JPY 60.00 per share for fiscal 2025. Earnings are forecast to grow at 13.22% annually, outpacing the Japanese market's average growth rate and supporting its undervaluation based on cash flows.

- Our earnings growth report unveils the potential for significant increases in TechnoPro Holdings' future results.

- Get an in-depth perspective on TechnoPro Holdings' balance sheet by reading our health report here.

Turning Ideas Into Actions

- Investigate our full lineup of 498 Undervalued Global Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TechnoPro Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6028

TechnoPro Holdings

Through its subsidiaries, operates as a temporary staffing and contract work company in Japan and internationally.

Flawless balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|38.7% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|30.8% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.6% undervalued

MA

Community Contributor