Advertisement

- Saudi Arabia

- /

- Metals and Mining

- /

- SASE:2200

Investors Will Want Arabian Pipes' (TADAWUL:2200) Growth In ROCE To Persist

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. With that in mind, we've noticed some promising trends at Arabian Pipes (TADAWUL:2200) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Arabian Pipes, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.05 = ر.س10m ÷ (ر.س766m - ر.س559m) (Based on the trailing twelve months to December 2022).

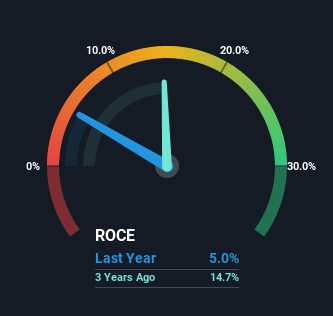

Therefore, Arabian Pipes has an ROCE of 5.0%. Ultimately, that's a low return and it under-performs the Metals and Mining industry average of 12%.

View our latest analysis for Arabian Pipes

Historical performance is a great place to start when researching a stock so above you can see the gauge for Arabian Pipes' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Arabian Pipes, check out these free graphs here.

SWOT Analysis for Arabian Pipes

Strength

- Debt is well covered by .

Weakness

- Interest payments on debt are not well covered.

Opportunity

- 2200's financial characteristics indicate limited near-term opportunities for shareholders.

- Lack of analyst coverage makes it difficult to determine 2200's earnings prospects.

Threat

- Debt is not well covered by operating cash flow.

How Are Returns Trending?

We're pretty happy with how the ROCE has been trending at Arabian Pipes. The data shows that returns on capital have increased by 30% over the trailing five years. The company is now earning ر.س0.05 per dollar of capital employed. In regards to capital employed, Arabian Pipes appears to been achieving more with less, since the business is using 69% less capital to run its operation. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 73% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

What We Can Learn From Arabian Pipes' ROCE

From what we've seen above, Arabian Pipes has managed to increase it's returns on capital all the while reducing it's capital base. Investors may not be impressed by the favorable underlying trends yet because over the last five years the stock has only returned 22% to shareholders. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

Arabian Pipes does have some risks, we noticed 3 warning signs (and 1 which is potentially serious) we think you should know about.

While Arabian Pipes may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:2200

Arabian Pipes

Engages in the production and marketing of steel tubes in the Kingdom of Saudi Arabia.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor