- Saudi Arabia

- /

- Basic Materials

- /

- SASE:2090

National Gypsum's (TADAWUL:2090) Problems Go Beyond Weak Profit

The subdued market reaction suggests that National Gypsum Company's (TADAWUL:2090) recent earnings didn't contain any surprises. However, we believe that investors should be aware of some underlying factors which may be of concern.

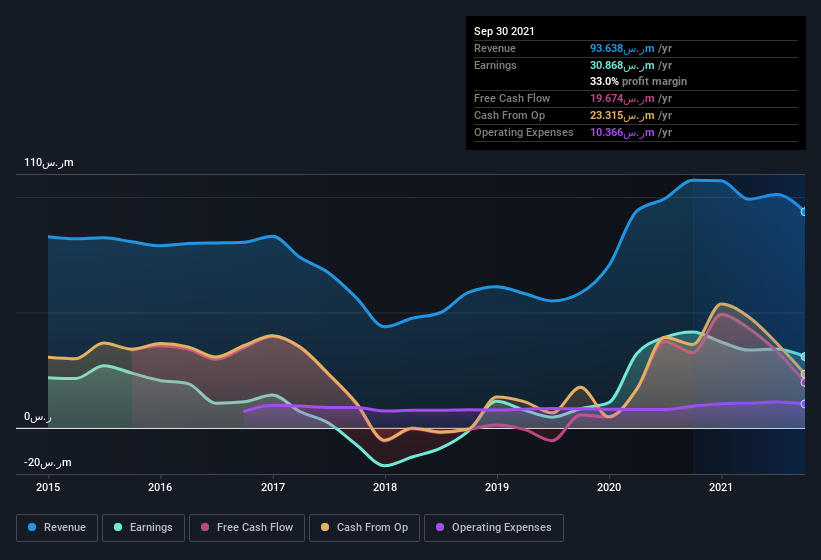

See our latest analysis for National Gypsum

The Impact Of Unusual Items On Profit

To properly understand National Gypsum's profit results, we need to consider the ر.س2.4m gain attributed to unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. If National Gypsum doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of National Gypsum.

Our Take On National Gypsum's Profit Performance

Arguably, National Gypsum's statutory earnings have been distorted by unusual items boosting profit. Because of this, we think that it may be that National Gypsum's statutory profits are better than its underlying earnings power. Sadly, its EPS was down over the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. While it's very important to consider the profit and loss statement, you can also learn a lot about a company by looking at its balance sheet. You can see our latest analysis on National Gypsum's balance sheet health here.

Today we've zoomed in on a single data point to better understand the nature of National Gypsum's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking to trade National Gypsum, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if National Gypsum might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:2090

National Gypsum

Engages in the manufacture and trading of gypsum and its derivatives in the Kingdom of Saudi Arabia.

Flawless balance sheet minimal.