- Saudi Arabia

- /

- Insurance

- /

- SASE:8250

Gulf Insurance Group's (TADAWUL:8250) Popularity With Investors Under Threat As Stock Sinks 26%

Gulf Insurance Group (TADAWUL:8250) shares have had a horrible month, losing 26% after a relatively good period beforehand. Indeed, the recent drop has reduced its annual gain to a relatively sedate 7.6% over the last twelve months.

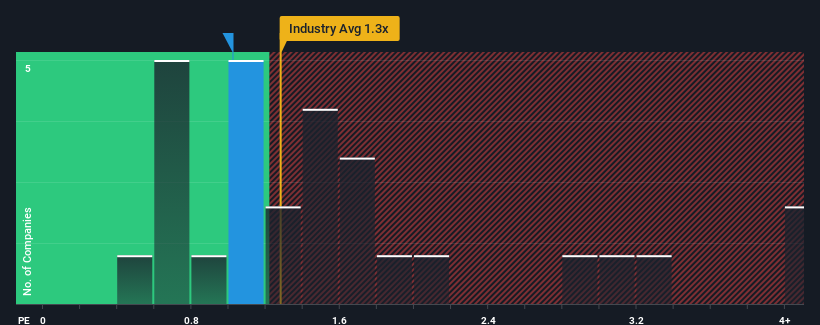

Although its price has dipped substantially, you could still be forgiven for feeling indifferent about Gulf Insurance Group's P/S ratio of 1x, since the median price-to-sales (or "P/S") ratio for the Insurance industry in Saudi Arabia is also close to 1.3x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Check out our latest analysis for Gulf Insurance Group

What Does Gulf Insurance Group's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Gulf Insurance Group has been relatively sluggish. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Gulf Insurance Group will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Gulf Insurance Group?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Gulf Insurance Group's to be considered reasonable.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period was better as it's delivered a decent 14% overall rise in revenue. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 7.2% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 28% per annum, which is noticeably more attractive.

With this in mind, we find it intriguing that Gulf Insurance Group's P/S is closely matching its industry peers. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does Gulf Insurance Group's P/S Mean For Investors?

With its share price dropping off a cliff, the P/S for Gulf Insurance Group looks to be in line with the rest of the Insurance industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Given that Gulf Insurance Group's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

Having said that, be aware Gulf Insurance Group is showing 3 warning signs in our investment analysis, you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade Gulf Insurance Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8250

Gulf Insurance Group

Provides various insurance and reinsurance products and services in the Kingdom of Saudi Arabia.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives