- Saudi Arabia

- /

- Hospitality

- /

- SASE:6002

Herfy Food Services Company Just Missed Earnings And Its Revenue Numbers Were Weaker Than Expected

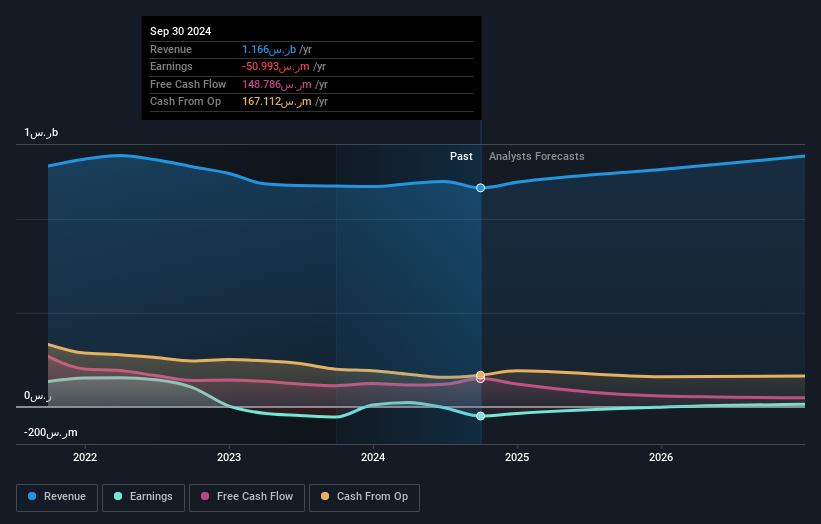

Herfy Food Services Company (TADAWUL:6002) shareholders are probably feeling a little disappointed, since its shares fell 4.2% to ر.س24.48 in the week after its latest quarterly results. Revenues were ر.س279m, 15% below analyst expectations, although losses didn't appear to worsen significantly, with a per-share statutory loss of ر.س0.13 being in line with what the analysts forecast. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Herfy Food Services after the latest results.

See our latest analysis for Herfy Food Services

Taking into account the latest results, the most recent consensus for Herfy Food Services from four analysts is for revenues of ر.س1.26b in 2025. If met, it would imply a notable 8.4% increase on its revenue over the past 12 months. Earnings are expected to improve, with Herfy Food Services forecast to report a statutory profit of ر.س0.51 per share. In the lead-up to this report, the analysts had been modelling revenues of ر.س1.31b and earnings per share (EPS) of ر.س0.49 in 2025. So it's pretty clear that while sentiment around revenues has declined following the latest results, the analysts are now more bullish on the company's earnings power.

The consensus price target fell 5.6% to ر.س25.50, with the analysts signalling that the weaker revenue outlook was a more powerful indicator than the upgraded EPS forecasts. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Herfy Food Services, with the most bullish analyst valuing it at ر.س27.82 and the most bearish at ر.س23.70 per share. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. One thing stands out from these estimates, which is that Herfy Food Services is forecast to grow faster in the future than it has in the past, with revenues expected to display 6.6% annualised growth until the end of 2025. If achieved, this would be a much better result than the 0.5% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 13% per year. Although Herfy Food Services' revenues are expected to improve, it seems that the analysts are still bearish on the business, forecasting it to grow slower than the broader industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Herfy Food Services following these results. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. Even so, long term profitability is more important for the value creation process. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Herfy Food Services' future valuation.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Herfy Food Services going out to 2026, and you can see them free on our platform here.

Plus, you should also learn about the 3 warning signs we've spotted with Herfy Food Services .

Valuation is complex, but we're here to simplify it.

Discover if Herfy Food Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:6002

Herfy Food Services

Herfy Food Services Company establishes, operates, and franchises restaurants in the Kingdom of Saudi Arabia and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives