- Saudi Arabia

- /

- Machinery

- /

- SASE:2160

Investors Shouldn't Be Too Comfortable With Saudi Arabian Amiantit's (TADAWUL:2160) Earnings

Last week's profit announcement from The Saudi Arabian Amiantit Company (TADAWUL:2160) was underwhelming for investors, despite headline numbers being robust. We think that the market might be paying attention to some underlying factors that they find to be concerning.

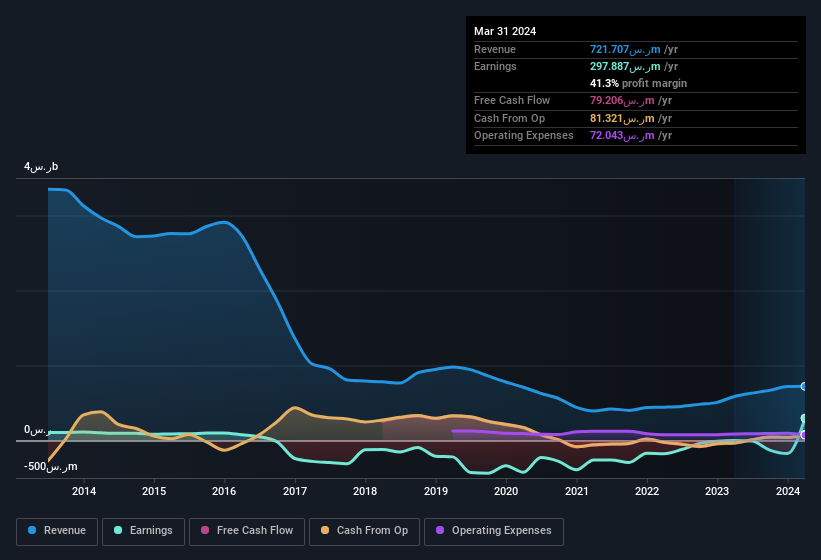

Check out our latest analysis for Saudi Arabian Amiantit

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Saudi Arabian Amiantit issued 350% more new shares over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Saudi Arabian Amiantit's historical EPS growth by clicking on this link.

How Is Dilution Impacting Saudi Arabian Amiantit's Earnings Per Share (EPS)?

Saudi Arabian Amiantit was losing money three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

If Saudi Arabian Amiantit's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Saudi Arabian Amiantit.

Our Take On Saudi Arabian Amiantit's Profit Performance

Saudi Arabian Amiantit issued shares during the year, and that means its EPS performance lags its net income growth. As a result, we think it may well be the case that Saudi Arabian Amiantit's underlying earnings power is lower than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. For example - Saudi Arabian Amiantit has 3 warning signs we think you should be aware of.

This note has only looked at a single factor that sheds light on the nature of Saudi Arabian Amiantit's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:2160

Saudi Arabian Amiantit

Manufactures and sells various types of pipes and related products in Saudi Arabia.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives