Advertisement

- Saudi Arabia

- /

- Electrical

- /

- SASE:1303

Investors Appear Satisfied With Electrical Industries Company's (TADAWUL:1303) Prospects As Shares Rocket 27%

Despite an already strong run, Electrical Industries Company (TADAWUL:1303) shares have been powering on, with a gain of 27% in the last thirty days. The annual gain comes to 256% following the latest surge, making investors sit up and take notice.

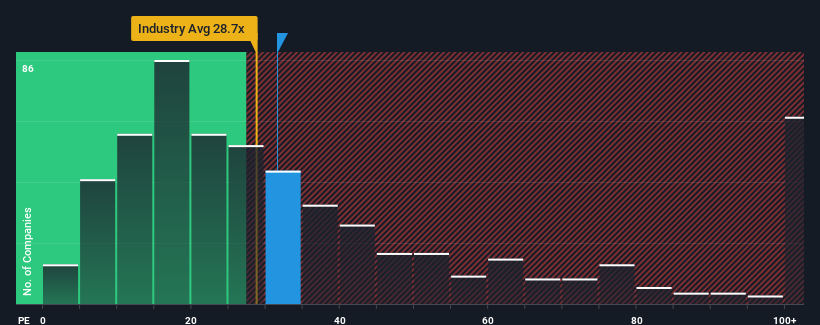

Following the firm bounce in price, given around half the companies in Saudi Arabia have price-to-earnings ratios (or "P/E's") below 27x, you may consider Electrical Industries as a stock to potentially avoid with its 31.5x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Electrical Industries certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Electrical Industries

How Is Electrical Industries' Growth Trending?

In order to justify its P/E ratio, Electrical Industries would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered an exceptional 113% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 745% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 19% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we can see why Electrical Industries is trading at such a high P/E compared to the market. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse.

What We Can Learn From Electrical Industries' P/E?

The large bounce in Electrical Industries' shares has lifted the company's P/E to a fairly high level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Electrical Industries maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Electrical Industries you should know about.

If you're unsure about the strength of Electrical Industries' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Electrical Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:1303

Electrical Industries

Engages in the manufacture, assembly, supply, repair, and maintenance of transformers, compact substations and low voltage distribution panels, electrical distribution boards, cable trays, switch gears, and other electrical equipment.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.7% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.0% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.5% undervalued

BL

Community Contributor