Advertisement

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. That's why when we briefly looked at Novorossyisk Grain Plant's (MCX:NKHP) ROCE trend, we were very happy with what we saw.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Novorossyisk Grain Plant:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

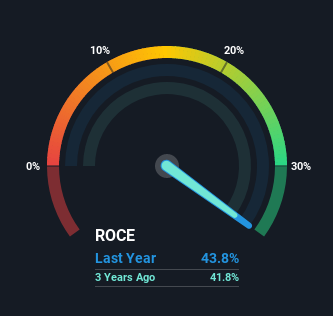

0.44 = ₽4.3b ÷ (₽12b - ₽2.4b) (Based on the trailing twelve months to June 2021).

Therefore, Novorossyisk Grain Plant has an ROCE of 44%. In absolute terms that's a great return and it's even better than the Infrastructure industry average of 7.6%.

View our latest analysis for Novorossyisk Grain Plant

Historical performance is a great place to start when researching a stock so above you can see the gauge for Novorossyisk Grain Plant's ROCE against it's prior returns. If you're interested in investigating Novorossyisk Grain Plant's past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Novorossyisk Grain Plant's ROCE Trending?

We'd be pretty happy with returns on capital like Novorossyisk Grain Plant. Over the past five years, ROCE has remained relatively flat at around 44% and the business has deployed 138% more capital into its operations. With returns that high, it's great that the business can continually reinvest its money at such appealing rates of return. You'll see this when looking at well operated businesses or favorable business models.

Another point to note, we noticed the company has increased current liabilities over the last five years. This is intriguing because if current liabilities hadn't increased to 19% of total assets, this reported ROCE would probably be less than44% because total capital employed would be higher.The 44% ROCE could be even lower if current liabilities weren't 19% of total assets, because the the formula would show a larger base of total capital employed. With that in mind, just be wary if this ratio increases in the future, because if it gets particularly high, this brings with it some new elements of risk.

The Bottom Line

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. And since the stock has risen strongly over the last five years, it appears the market might expect this trend to continue. So while investors seem to be recognizing these promising trends, we still believe the stock deserves further research.

If you'd like to know about the risks facing Novorossyisk Grain Plant, we've discovered 1 warning sign that you should be aware of.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

If you decide to trade Novorossyisk Grain Plant, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Novorossyisk Grain Plant might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About MISX:NKHP

Novorossyisk Grain Plant

Public Joint Stock Company Novorossyisk Grain Plant owns and operates grain terminals in Russia.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor