Advertisement

- Qatar

- /

- Diversified Financial

- /

- DSM:SIIS

Salam International Investment Limited Q.P.S.C (DSM:SIIS) Is Increasing Its Dividend To QAR0.04

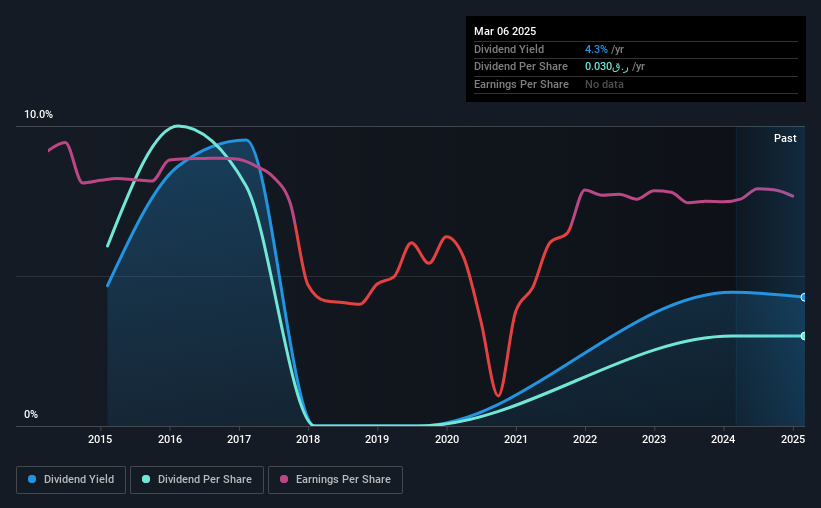

Salam International Investment Limited Q.P.S.C.'s (DSM:SIIS) periodic dividend will be increasing on the 1st of January to QAR0.04, with investors receiving 33% more than last year's QAR0.03. This will take the dividend yield to an attractive 4.3%, providing a nice boost to shareholder returns.

See our latest analysis for Salam International Investment Limited Q.P.S.C

Salam International Investment Limited Q.P.S.C's Future Dividend Projections Appear Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, Salam International Investment Limited Q.P.S.C was quite comfortably earning enough to cover the dividend. This means that a large portion of its earnings are being retained to grow the business.

Over the next year, EPS could expand by 60.1% if recent trends continue. If the dividend continues on this path, the payout ratio could be 51% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2015, the dividend has gone from QAR0.06 total annually to QAR0.03. This works out to be a decline of approximately 6.7% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

The Dividend Looks Likely To Grow

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. Salam International Investment Limited Q.P.S.C has seen EPS rising for the last five years, at 60% per annum. The company doesn't have any problems growing, despite returning a lot of capital to shareholders, which is a very nice combination for a dividend stock to have.

Salam International Investment Limited Q.P.S.C Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 1 warning sign for Salam International Investment Limited Q.P.S.C that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DSM:SIIS

Salam International Investment Limited Q.P.S.C

Salam International Investment Limited Q.P.S.C.

Proven track record second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

PPG Industries set to soar with 9% revenue growth in the next 3 years

Fair Value US$152.76|24.9% undervalued

DM

Community Contributor

Predicting a Steady Future for Crocs with Modest Growth and a 10% Discount Rate

Fair Value US$151.43|33.2% undervalued

JO

Community Contributor