Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies FinTech Ventures S.A. (WSE:FIV) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for FinTech Ventures

What Is FinTech Ventures's Net Debt?

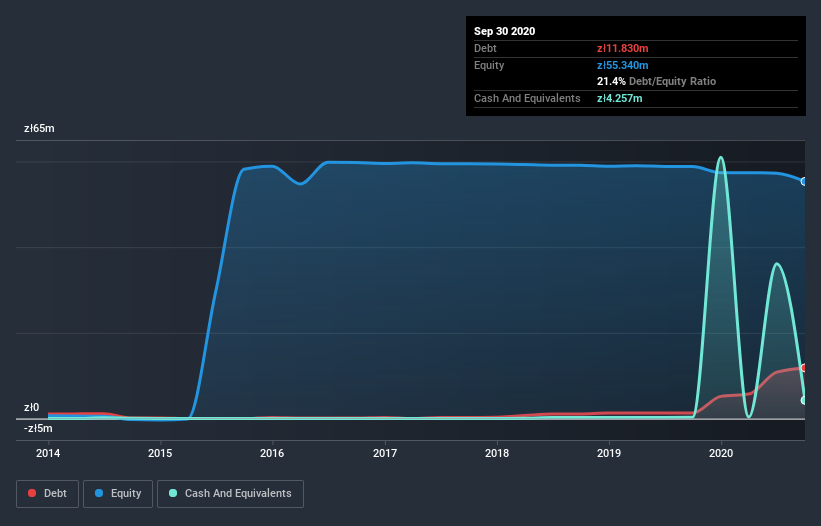

The image below, which you can click on for greater detail, shows that at September 2020 FinTech Ventures had debt of zł11.8m, up from zł1.30m in one year. However, it does have zł4.26m in cash offsetting this, leading to net debt of about zł7.57m.

How Strong Is FinTech Ventures's Balance Sheet?

According to the last reported balance sheet, FinTech Ventures had liabilities of zł13.4m due within 12 months, and liabilities of zł2.24m due beyond 12 months. Offsetting this, it had zł4.26m in cash and zł32.2m in receivables that were due within 12 months. So it actually has zł20.9m more liquid assets than total liabilities.

This surplus strongly suggests that FinTech Ventures has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since FinTech Ventures will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Given it has no significant operating revenue at the moment, shareholders will be hoping FinTech Ventures can make progress and gain better traction for the business, before it runs low on cash.

Caveat Emptor

Importantly, FinTech Ventures had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at zł3.7m. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. So it seems too risky for our taste. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - FinTech Ventures has 5 warning signs (and 3 which are a bit unpleasant) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade FinTech Ventures, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About WSE:LUD

Ludus

Operates an esports platform. The company provides services, such as e-wallet; courses, masterclasses, and private coaching; deals solutions; cashback; FIFA; fitness tracker; marketplace for NFTs; greets that allows communication; and banking solutions.

Adequate balance sheet low.

Market Insights

Community Narratives