Advertisement

Revenues Working Against Mabion S.A.'s (WSE:MAB) Share Price Following 29% Dive

To the annoyance of some shareholders, Mabion S.A. (WSE:MAB) shares are down a considerable 29% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 53% loss during that time.

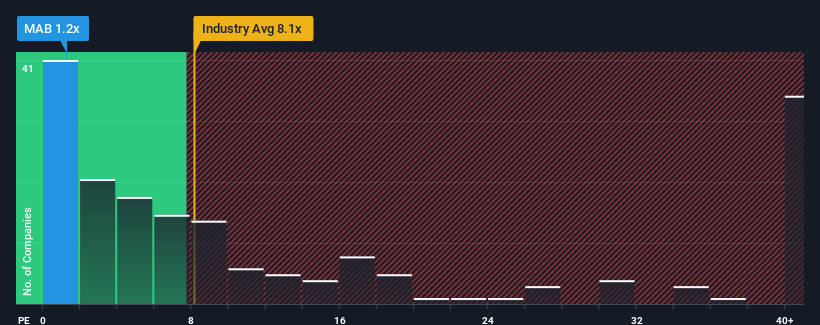

In spite of the heavy fall in price, Mabion may still look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 1.2x, considering almost half of all companies in the Biotechs industry in Poland have P/S ratios greater than 7.4x and even P/S higher than 29x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

View our latest analysis for Mabion

What Does Mabion's Recent Performance Look Like?

Mabion has been struggling lately as its revenue has declined faster than most other companies. It seems that many are expecting the dismal revenue performance to persist, which has repressed the P/S. If you still like the company, you'd want its revenue trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Mabion's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The Low P/S?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Mabion's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 25%. In spite of this, the company still managed to deliver immense revenue growth over the last three years. Accordingly, shareholders will be pleased, but also have some serious questions to ponder about the last 12 months.

Shifting to the future, estimates from the three analysts covering the company suggest revenue growth is heading into negative territory, declining 17% each year over the next three years. Meanwhile, the broader industry is forecast to expand by 73% per year, which paints a poor picture.

With this in consideration, we find it intriguing that Mabion's P/S is closely matching its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From Mabion's P/S?

Having almost fallen off a cliff, Mabion's share price has pulled its P/S way down as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It's clear to see that Mabion maintains its low P/S on the weakness of its forecast for sliding revenue, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless there's material change, it's hard to envision a situation where the stock price will rise drastically.

Plus, you should also learn about these 5 warning signs we've spotted with Mabion (including 1 which is concerning).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:MAB

Mabion

A biotechnology company, engages in the development of various biotech drugs based on monoclonal antibody technology in Poland.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor