Advertisement

- Poland

- /

- Telecom Services and Carriers

- /

- WSE:CPS

Cyfrowy Polsat (WSE:CPS) Has A Pretty Healthy Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Cyfrowy Polsat S.A. (WSE:CPS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Cyfrowy Polsat

What Is Cyfrowy Polsat's Net Debt?

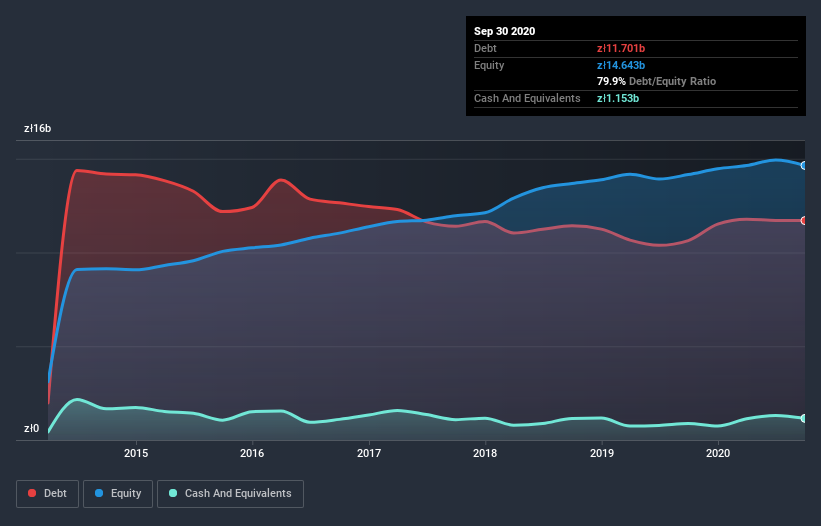

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Cyfrowy Polsat had zł11.7b of debt, an increase on zł10.6b, over one year. However, because it has a cash reserve of zł1.15b, its net debt is less, at about zł10.5b.

A Look At Cyfrowy Polsat's Liabilities

According to the last reported balance sheet, Cyfrowy Polsat had liabilities of zł4.66b due within 12 months, and liabilities of zł13.5b due beyond 12 months. On the other hand, it had cash of zł1.15b and zł2.92b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł14.1b.

This is a mountain of leverage relative to its market capitalization of zł18.3b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Cyfrowy Polsat has a debt to EBITDA ratio of 3.0 and its EBIT covered its interest expense 5.1 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Sadly, Cyfrowy Polsat's EBIT actually dropped 2.5% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Cyfrowy Polsat's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Cyfrowy Polsat actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

When it comes to the balance sheet, the standout positive for Cyfrowy Polsat was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. For example, its level of total liabilities makes us a little nervous about its debt. Looking at all this data makes us feel a little cautious about Cyfrowy Polsat's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Cyfrowy Polsat , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Cyfrowy Polsat, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:CPS

Cyfrowy Polsat

Provides digital satellite platform and terrestrial television (TV), and telecommunication services primarily in Poland.

Good value with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor