Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Lubelski Wegiel Bogdanka S.A. (WSE:LWB) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Lubelski Wegiel Bogdanka

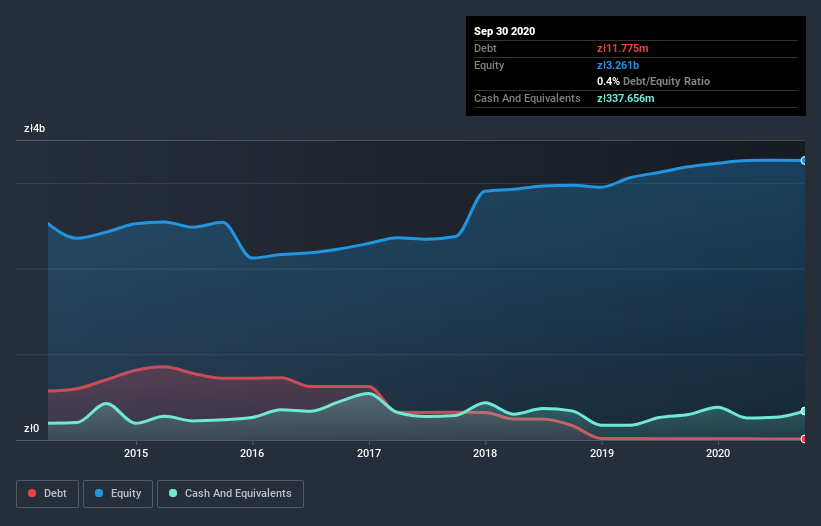

What Is Lubelski Wegiel Bogdanka's Debt?

The image below, which you can click on for greater detail, shows that Lubelski Wegiel Bogdanka had debt of zł11.8m at the end of September 2020, a reduction from zł14.8m over a year. But on the other hand it also has zł337.7m in cash, leading to a zł325.9m net cash position.

How Healthy Is Lubelski Wegiel Bogdanka's Balance Sheet?

We can see from the most recent balance sheet that Lubelski Wegiel Bogdanka had liabilities of zł434.4m falling due within a year, and liabilities of zł677.4m due beyond that. On the other hand, it had cash of zł337.7m and zł226.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł547.7m.

This deficit is considerable relative to its market capitalization of zł867.3m, so it does suggest shareholders should keep an eye on Lubelski Wegiel Bogdanka's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. Despite its noteworthy liabilities, Lubelski Wegiel Bogdanka boasts net cash, so it's fair to say it does not have a heavy debt load!

The modesty of its debt load may become crucial for Lubelski Wegiel Bogdanka if management cannot prevent a repeat of the 66% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Lubelski Wegiel Bogdanka's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Lubelski Wegiel Bogdanka may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Lubelski Wegiel Bogdanka recorded free cash flow worth 71% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing up

Although Lubelski Wegiel Bogdanka's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of zł325.9m. And it impressed us with free cash flow of zł51m, being 71% of its EBIT. So we are not troubled with Lubelski Wegiel Bogdanka's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Lubelski Wegiel Bogdanka , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Lubelski Wegiel Bogdanka, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:LWB

Lubelski Wegiel Bogdanka

Engages in the hard coal mining business in Poland.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|32.1% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|34.7% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|29.9% undervalued

EV

Community Contributor