There are a few key trends to look for if we want to identify the next multi-bagger. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So on that note, OZE Capital (WSE:OZE) looks quite promising in regards to its trends of return on capital.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for OZE Capital:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.015 = zł871k ÷ (zł129m - zł73m) (Based on the trailing twelve months to June 2022).

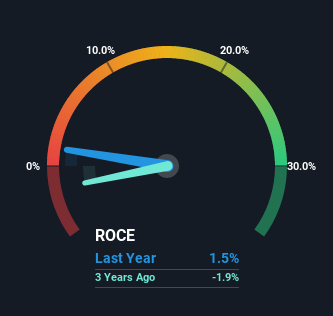

Therefore, OZE Capital has an ROCE of 1.5%. Ultimately, that's a low return and it under-performs the Machinery industry average of 10%.

View our latest analysis for OZE Capital

Historical performance is a great place to start when researching a stock so above you can see the gauge for OZE Capital's ROCE against it's prior returns. If you're interested in investigating OZE Capital's past further, check out this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

We're delighted to see that OZE Capital is reaping rewards from its investments and is now generating some pre-tax profits. The company was generating losses five years ago, but now it's earning 1.5% which is a sight for sore eyes. In addition to that, OZE Capital is employing 84% more capital than previously which is expected of a company that's trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Effectively this means that suppliers or short-term creditors are now funding 56% of the business, which is more than it was five years ago. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

The Bottom Line On OZE Capital's ROCE

In summary, it's great to see that OZE Capital has managed to break into profitability and is continuing to reinvest in its business. Investors may not be impressed by the favorable underlying trends yet because over the last five years the stock has only returned 8.1% to shareholders. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

One more thing: We've identified 3 warning signs with OZE Capital (at least 2 which shouldn't be ignored) , and understanding these would certainly be useful.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:OZE

Excellent balance sheet low.

Market Insights

Community Narratives