Advertisement

In recent weeks, European markets have experienced volatility, with the pan-European STOXX Europe 600 Index declining by about 1.4% amid new U.S. trade tariffs and mixed economic signals. Despite these challenges, the eurozone's private sector has shown resilience with continued growth in services and a rebound in manufacturing, highlighting potential opportunities for discerning investors to explore promising small-cap stocks that may thrive in such an environment.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| AB Traction | NA | 3.81% | 3.66% | ★★★★★★ |

| Nederman Holding | 69.60% | 11.43% | 16.35% | ★★★★★★ |

| FRoSTA | 6.15% | 4.62% | 14.67% | ★★★★★★ |

| Linc | NA | 19.35% | 23.17% | ★★★★★★ |

| Caisse Régionale de Crédit Agricole Mutuel Brie Picardie Société coopérative | 26.90% | 4.14% | 7.22% | ★★★★★★ |

| La Forestière Equatoriale | NA | -58.49% | 45.78% | ★★★★★★ |

| Intellego Technologies | 11.59% | 68.05% | 72.76% | ★★★★★★ |

| Prim | 10.72% | 10.36% | 0.14% | ★★★★☆☆ |

| Castellana Properties Socimi | 53.49% | 6.64% | 21.96% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

FRoSTA (DB:NLM)

Simply Wall St Value Rating: ★★★★★★

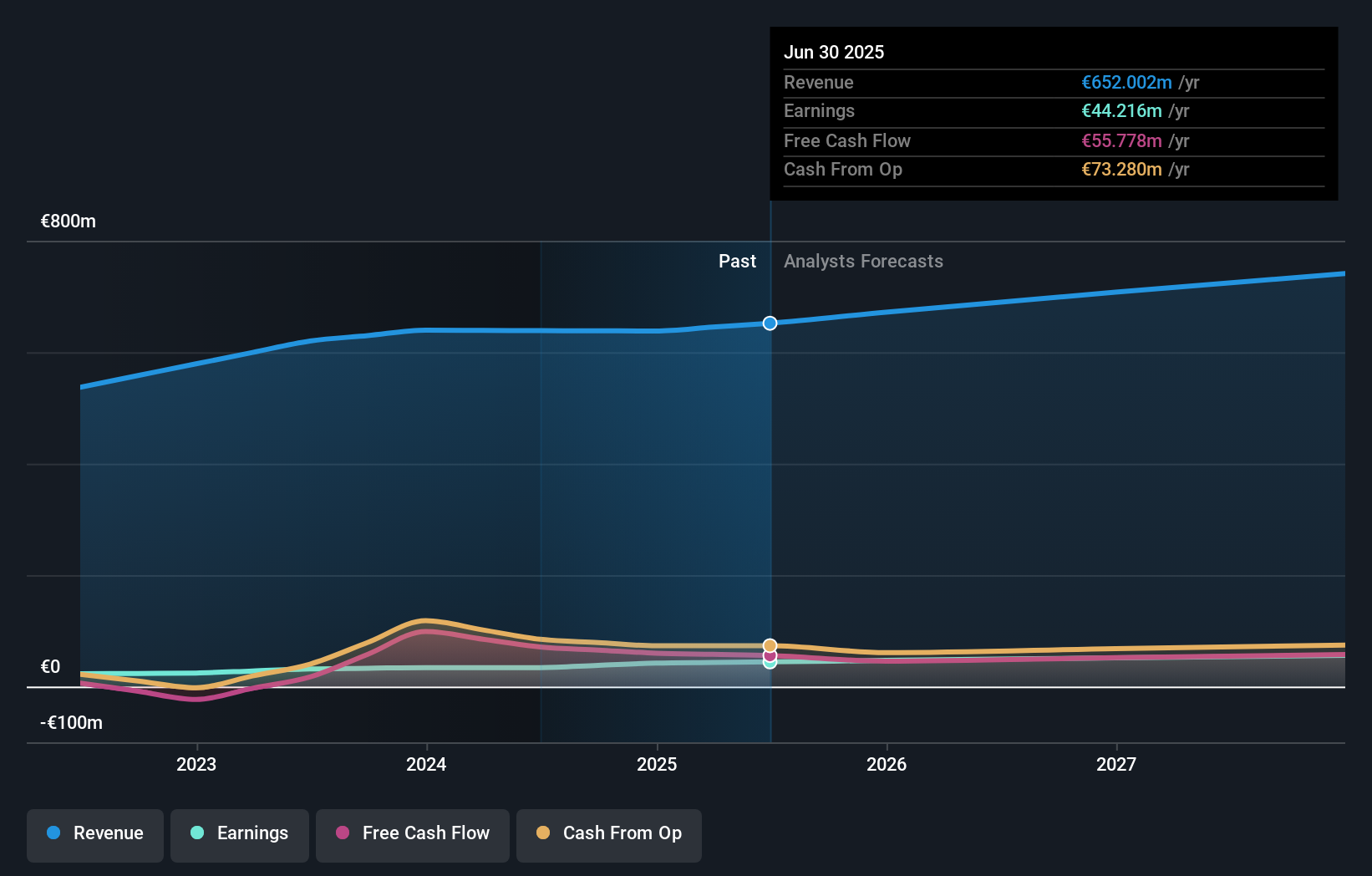

Overview: FRoSTA Aktiengesellschaft, along with its subsidiaries, develops, produces, and markets frozen food products across Germany, Poland, Austria, Italy, and Eastern Europe with a market cap of €534.79 million.

Operations: FRoSTA generates revenue through the development, production, and marketing of frozen food products across several European countries. The company's financial performance is highlighted by its net profit margin trends, which provide insight into its profitability relative to total revenue.

FRoSTA, a notable player in the European food industry, has shown consistent growth with earnings increasing 14.7% annually over the past five years. The company's debt to equity ratio improved significantly from 33.7% to 6.2%, highlighting effective financial management. Despite a slight dip in sales from €639.48M to €638.05M, net income rose from €34.05M to €41.97M, reflecting strong operational efficiency and high-quality earnings performance with basic EPS climbing to €6.16 from €5 last year. The recent dividend announcement of €2.40 per share further underscores FRoSTA's commitment to rewarding shareholders amidst stable financial health.

- Delve into the full analysis health report here for a deeper understanding of FRoSTA.

Examine FRoSTA's past performance report to understand how it has performed in the past.

Placoplatre (ENXTPA:MLPLC)

Simply Wall St Value Rating: ★★★★☆☆

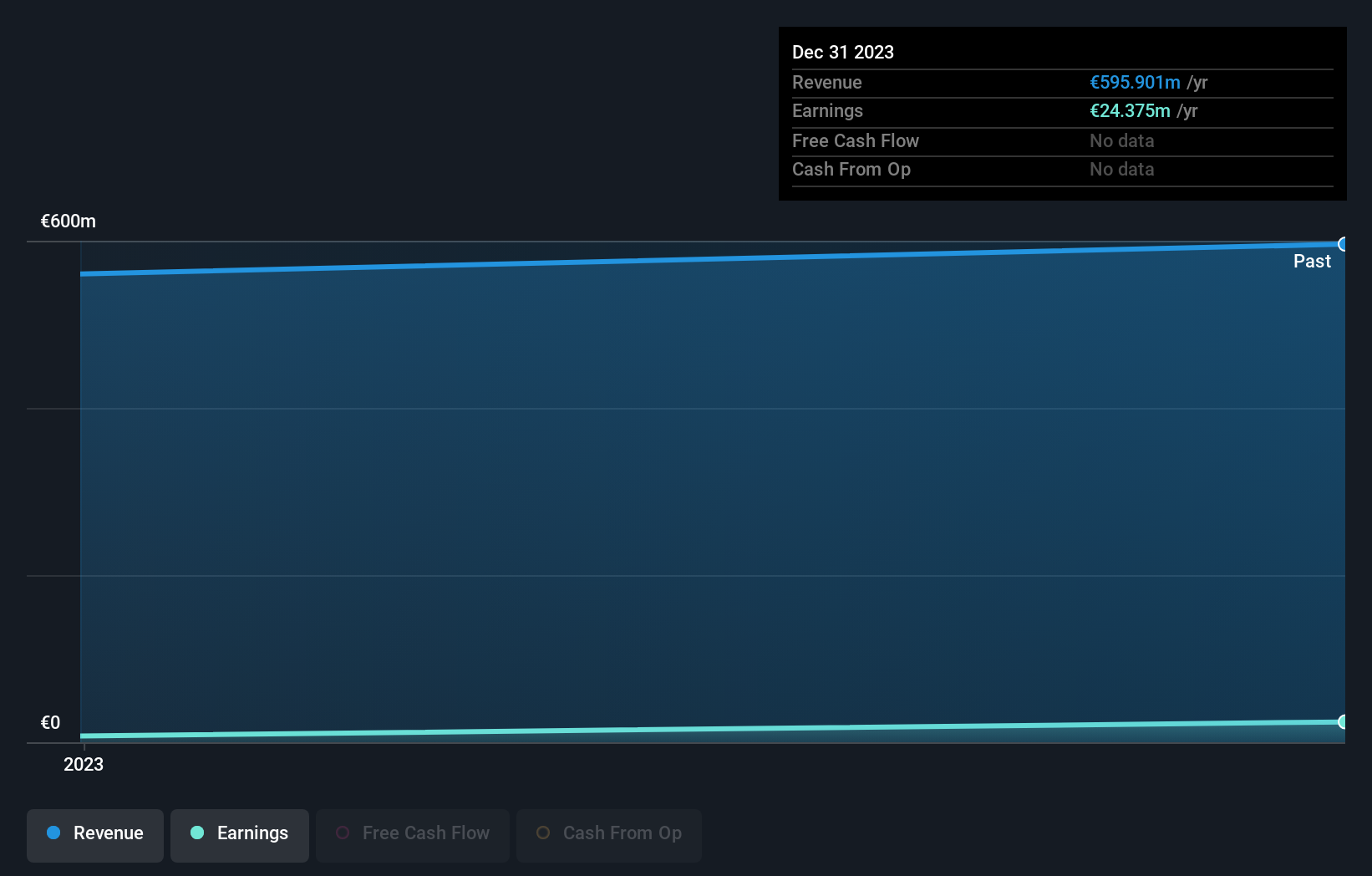

Overview: Placoplatre SA specializes in manufacturing and supplying insulation solutions for both professionals and individuals, with a market capitalization of €672.42 million.

Operations: Placoplatre SA generates revenue primarily from its construction materials segment, totaling €595.90 million.

Placoplatre, a smaller player in the European building materials sector, has demonstrated impressive earnings growth of 226.7% over the past year, outpacing the industry average of -8.9%. The company's net debt to equity ratio stands at a satisfactory 14.8%, indicating sound financial management. While specific cash flow data isn't available, Placoplatre's ability to cover interest payments effectively suggests robust financial health. The firm's high-quality earnings further underscore its potential as a solid investment prospect within its niche market segment.

- Click here and access our complete health analysis report to understand the dynamics of Placoplatre.

Understand Placoplatre's track record by examining our Past report.

Lubawa (WSE:LBW)

Simply Wall St Value Rating: ★★★★★★

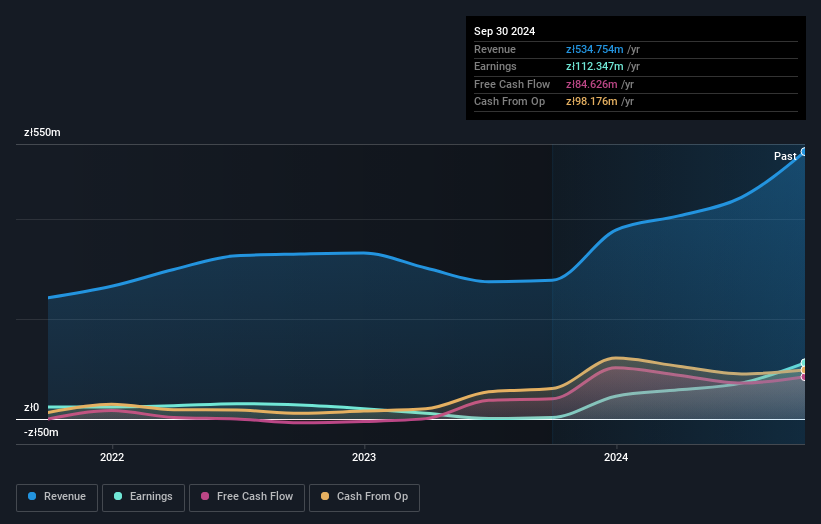

Overview: Lubawa S.A. is a company that produces and distributes products for the army, police, municipal police, border patrol, fire brigade, and special forces both in Poland and internationally, with a market capitalization of PLN 1.47 billion.

Operations: Lubawa generates revenue primarily from Specialist Equipment - Retail, contributing PLN 264.99 million, followed by Fabrics at PLN 180.45 million and Advertising Materials at PLN 142.56 million. The company's net profit margin is a key financial metric to consider when evaluating its performance.

Lubawa's financial performance paints an intriguing picture, with its earnings skyrocketing by 3846%, outpacing the Aerospace & Defense industry's 33% growth rate. This Polish company is currently trading at a significant discount, valued 53.5% below its estimated fair value. Over the past five years, Lubawa has transitioned from a debt-to-equity ratio of 37.8% to being completely debt-free, which likely enhances its appeal to investors seeking stability in financial management. Despite these promising figures and high-quality earnings, potential investors should be aware of the stock's recent volatility over the last three months.

- Dive into the specifics of Lubawa here with our thorough health report.

Gain insights into Lubawa's historical performance by reviewing our past performance report.

Taking Advantage

- Embark on your investment journey to our 350 European Undiscovered Gems With Strong Fundamentals selection here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:MLPLC

Placoplatre

Manufactures and supplies insulation solutions for professionals and individuals.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|3.8% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|64.0% undervalued

OI

Community Contributor