Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Columbus Energy S.A. (WSE:CLC) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Columbus Energy

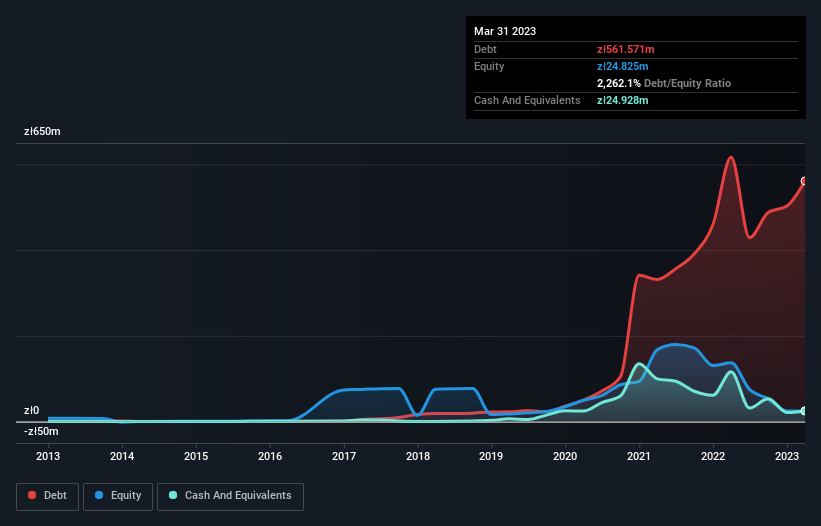

What Is Columbus Energy's Debt?

The image below, which you can click on for greater detail, shows that Columbus Energy had debt of zł561.6m at the end of March 2023, a reduction from zł616.7m over a year. However, because it has a cash reserve of zł24.9m, its net debt is less, at about zł536.6m.

A Look At Columbus Energy's Liabilities

Zooming in on the latest balance sheet data, we can see that Columbus Energy had liabilities of zł545.4m due within 12 months and liabilities of zł194.8m due beyond that. Offsetting these obligations, it had cash of zł24.9m as well as receivables valued at zł121.4m due within 12 months. So it has liabilities totalling zł593.9m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of zł475.2m, we think shareholders really should watch Columbus Energy's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Columbus Energy's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Columbus Energy had a loss before interest and tax, and actually shrunk its revenue by 36%, to zł493m. To be frank that doesn't bode well.

Caveat Emptor

While Columbus Energy's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping zł89m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of zł161m over the last twelve months. That means it's on the risky side of things. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Columbus Energy .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:CLC

Columbus Energy

Provides solar photovoltaics and heat pumps installation and maintenance services in Poland.

Low with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|32.3% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|34.7% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|30.3% undervalued

EV

Community Contributor