Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Columbus Energy S.A. (WSE:CLC) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Columbus Energy

How Much Debt Does Columbus Energy Carry?

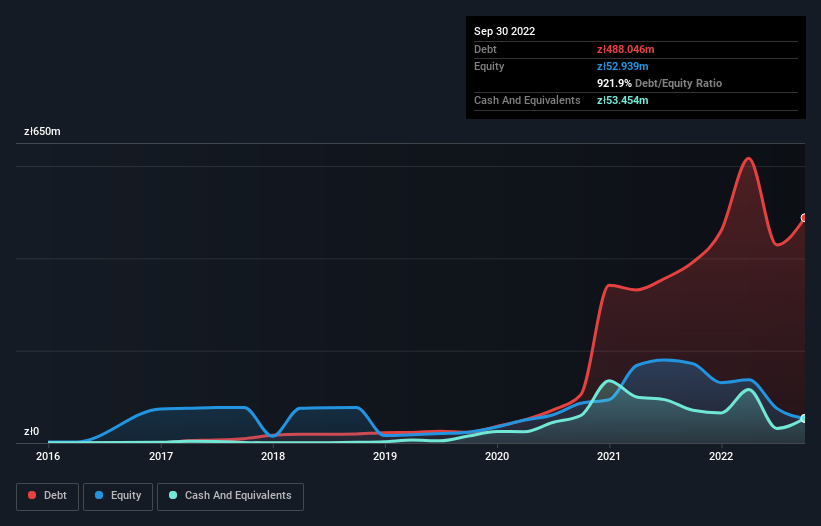

The image below, which you can click on for greater detail, shows that at September 2022 Columbus Energy had debt of zł488.0m, up from zł391.7m in one year. However, because it has a cash reserve of zł53.5m, its net debt is less, at about zł434.6m.

A Look At Columbus Energy's Liabilities

Zooming in on the latest balance sheet data, we can see that Columbus Energy had liabilities of zł695.7m due within 12 months and liabilities of zł209.6m due beyond that. On the other hand, it had cash of zł53.5m and zł95.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł756.2m.

Given this deficit is actually higher than the company's market capitalization of zł583.2m, we think shareholders really should watch Columbus Energy's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Columbus Energy will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Columbus Energy had a loss before interest and tax, and actually shrunk its revenue by 3.3%, to zł663m. We would much prefer see growth.

Caveat Emptor

Importantly, Columbus Energy had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable zł87m at the EBIT level. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through zł198m in negative free cash flow over the last year. That means it's on the risky side of things. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Columbus Energy you should be aware of, and 2 of them are concerning.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:CLC

Columbus Energy

Provides solar photovoltaics and heat pumps installation and maintenance services in Poland.

Low with imperfect balance sheet.