Advertisement

Bank Polska Kasa Opieki (WSE:PEO) Could Be A Buy For Its Upcoming Dividend

Bank Polska Kasa Opieki S.A. (WSE:PEO) is about to trade ex-dividend in the next three days. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. Thus, you can purchase Bank Polska Kasa Opieki's shares before the 6th of May in order to receive the dividend, which the company will pay on the 23rd of May.

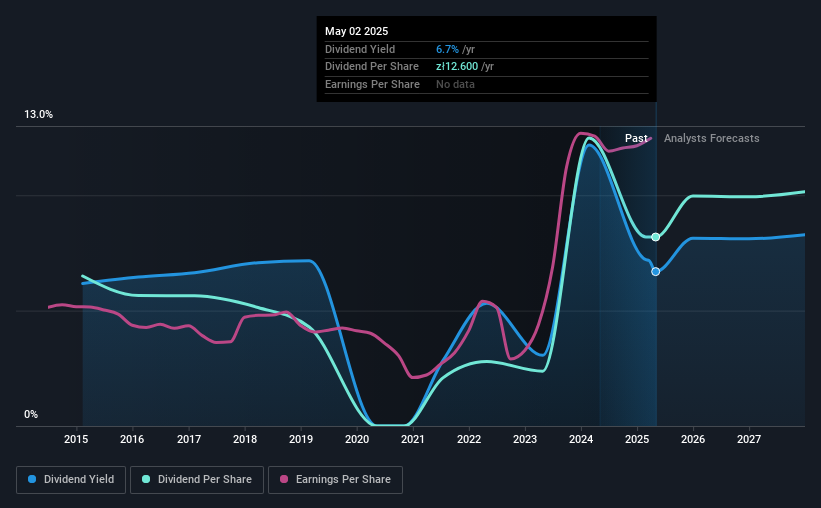

The company's upcoming dividend is zł18.36 a share, following on from the last 12 months, when the company distributed a total of zł12.60 per share to shareholders. Last year's total dividend payments show that Bank Polska Kasa Opieki has a trailing yield of 6.7% on the current share price of zł188.35. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

Our free stock report includes 2 warning signs investors should be aware of before investing in Bank Polska Kasa Opieki. Read for free now.Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Bank Polska Kasa Opieki paid out more than half (51%) of its earnings last year, which is a regular payout ratio for most companies.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

View our latest analysis for Bank Polska Kasa Opieki

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. That's why it's comforting to see Bank Polska Kasa Opieki's earnings have been skyrocketing, up 25% per annum for the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last 10 years, Bank Polska Kasa Opieki has lifted its dividend by approximately 2.3% a year on average. It's good to see both earnings and the dividend have improved - although the former has been rising much quicker than the latter, possibly due to the company reinvesting more of its profits in growth.

To Sum It Up

Is Bank Polska Kasa Opieki worth buying for its dividend? Bank Polska Kasa Opieki has an acceptable payout ratio and its earnings per share have been improving at a decent rate. Bank Polska Kasa Opieki ticks a lot of boxes for us from a dividend perspective, and we think these characteristics should mark the company as deserving of further attention.

On that note, you'll want to research what risks Bank Polska Kasa Opieki is facing. For example, Bank Polska Kasa Opieki has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Bank Polska Kasa Opieki might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:PEO

Bank Polska Kasa Opieki

A commercial bank, provides banking products and services to retail and corporate clients in Poland.

Undervalued established dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor