We Think Shareholders Will Probably Be Generous With Bank Handlowy w Warszawie S.A.'s (WSE:BHW) CEO Compensation

Key Insights

- Bank Handlowy w Warszawie's Annual General Meeting to take place on 19th of June

- Total pay for CEO Elzbieta Czetwertynska includes zł2.44m salary

- The overall pay is comparable to the industry average

- Bank Handlowy w Warszawie's EPS grew by 57% over the past three years while total shareholder return over the past three years was 166%

The performance at Bank Handlowy w Warszawie S.A. (WSE:BHW) has been quite strong recently and CEO Elzbieta Czetwertynska has played a role in it. Shareholders will have this at the front of their minds in the upcoming AGM on 19th of June. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. Here is our take on why we think CEO compensation is not extravagant.

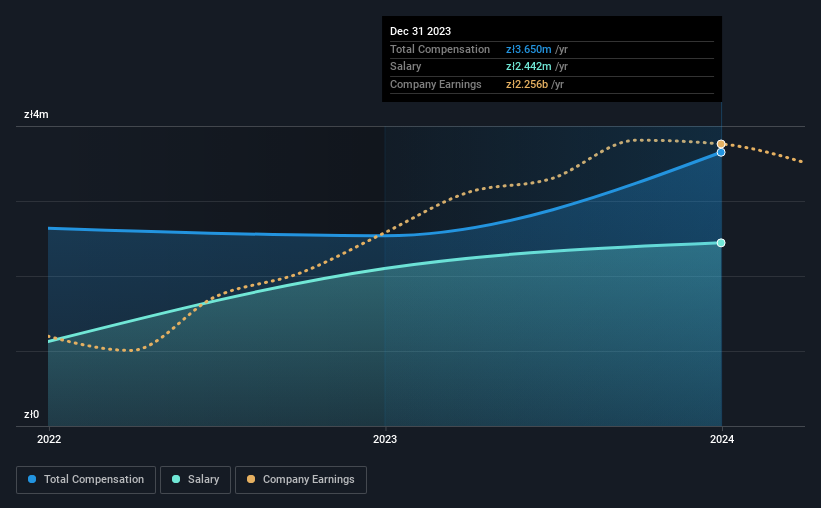

See our latest analysis for Bank Handlowy w Warszawie

How Does Total Compensation For Elzbieta Czetwertynska Compare With Other Companies In The Industry?

According to our data, Bank Handlowy w Warszawie S.A. has a market capitalization of zł13b, and paid its CEO total annual compensation worth zł3.7m over the year to December 2023. We note that's an increase of 44% above last year. We note that the salary portion, which stands at zł2.44m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the Polish Banks industry with market capitalizations ranging between zł8.1b and zł26b had a median total CEO compensation of zł5.0m. From this we gather that Elzbieta Czetwertynska is paid around the median for CEOs in the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | zł2.4m | zł2.1m | 67% |

| Other | zł1.2m | zł436k | 33% |

| Total Compensation | zł3.7m | zł2.5m | 100% |

Speaking on an industry level, nearly 69% of total compensation represents salary, while the remainder of 31% is other remuneration. Our data reveals that Bank Handlowy w Warszawie allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Bank Handlowy w Warszawie S.A.'s Growth Numbers

Bank Handlowy w Warszawie S.A. has seen its earnings per share (EPS) increase by 57% a year over the past three years. Its revenue is up 10% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Bank Handlowy w Warszawie S.A. Been A Good Investment?

Most shareholders would probably be pleased with Bank Handlowy w Warszawie S.A. for providing a total return of 166% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Given the company's decent performance, the CEO remuneration policy might not be shareholders' central point of focus in the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 2 warning signs for Bank Handlowy w Warszawie (1 is significant!) that you should be aware of before investing here.

Switching gears from Bank Handlowy w Warszawie, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you're looking to trade Bank Handlowy w Warszawie, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Bank Handlowy w Warszawie might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:BHW

Bank Handlowy w Warszawie

Provides a range of commercial banking services for individual and corporate clients in Poland and internationally.

Established dividend payer and good value.

Market Insights

Community Narratives