Advertisement

- Philippines

- /

- Food and Staples Retail

- /

- PSE:SEVN

Undiscovered Gems In Asia To Explore This March 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets face challenges with U.S. recession concerns and trade policy uncertainties, Asia's markets have shown resilience, with Chinese stocks rising on stimulus hopes and Japanese indices gaining modestly despite global trade worries. In this environment, identifying promising small-cap stocks in Asia requires a keen eye for companies that can leverage local economic policies and sectoral growth trends to navigate broader market volatility effectively.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Intelligent Wave | NA | 7.78% | 15.50% | ★★★★★★ |

| Lumax International | NA | 4.43% | 5.77% | ★★★★★★ |

| Central Forest Group | NA | 5.93% | 20.71% | ★★★★★★ |

| Otec | 8.17% | 3.43% | 1.06% | ★★★★★★ |

| Ohashi Technica | NA | 4.58% | -14.04% | ★★★★★★ |

| Shangri-La Hotel | NA | 15.26% | 23.20% | ★★★★★★ |

| Donpon Precision | 38.56% | 0.47% | 48.37% | ★★★★★★ |

| HeadwatersLtd | NA | 25.49% | 288.57% | ★★★★★★ |

| Hansae Yes24 Holdings | 80.77% | 1.28% | 9.02% | ★★★★☆☆ |

| Alltek Technology | 166.36% | 7.57% | 13.88% | ★★★★☆☆ |

We'll examine a selection from our screener results.

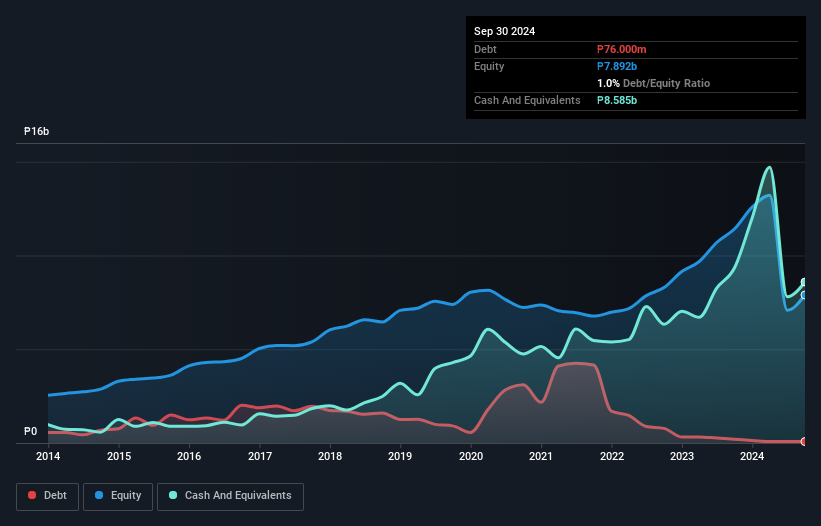

Philippine Seven (PSE:SEVN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Philippine Seven Corporation operates convenience stores in the Philippines with a market capitalization of ₱82.83 billion.

Operations: Philippine Seven Corporation generates revenue primarily from its store operations, amounting to ₱88.61 billion. The company focuses on optimizing its cost structure to enhance profitability, with a gross profit margin of 31.5%.

Philippine Seven, a notable player in the retail sector, has demonstrated impressive financial resilience. Over the past year, its earnings surged by 26%, outpacing the Consumer Retailing industry's growth of 8.8%. The company's debt management is commendable with a debt to equity ratio dropping from 12.4% to just 1% over five years and interest payments well-covered at 6.3 times by EBIT. Despite recent delisting due to inactivity, SEVN's future remains promising with forecasted earnings growth of 17% annually and more cash than total debt, indicating robust financial health and potential for sustained performance.

- Navigate through the intricacies of Philippine Seven with our comprehensive health report here.

Understand Philippine Seven's track record by examining our Past report.

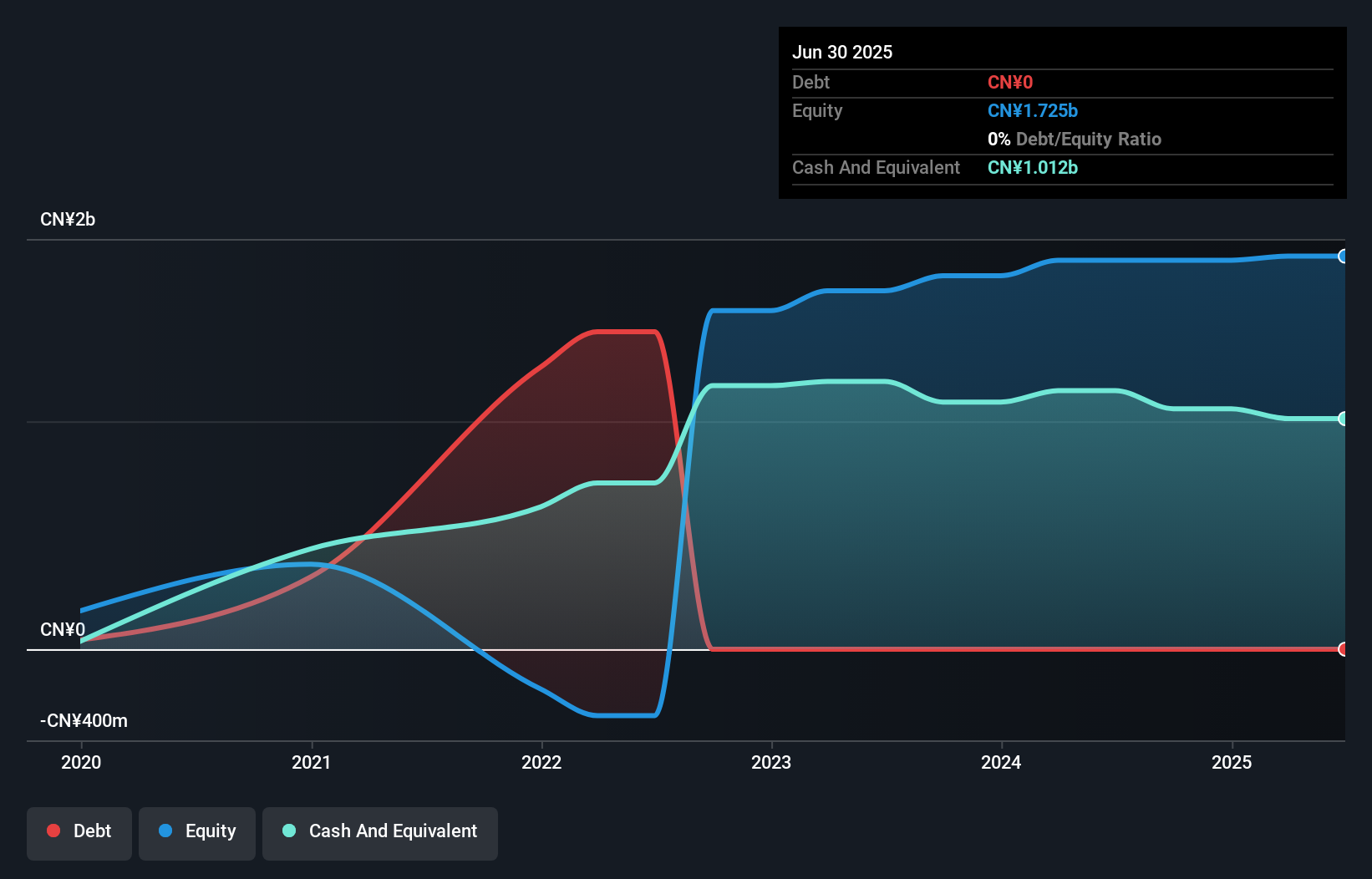

MicroPort NeuroScientific (SEHK:2172)

Simply Wall St Value Rating: ★★★★★★

Overview: MicroPort NeuroScientific Corporation focuses on the research, development, production, and sale of neuro-interventional medical devices in China and globally, with a market capitalization of HK$7.39 billion.

Operations: MicroPort NeuroScientific generates revenue primarily from the sale of surgical and medical equipment, totaling CN¥774.66 million.

MicroPort NeuroScientific has been making waves with its impressive financial performance. Over the past year, earnings grew by 67%, outpacing the Medical Equipment industry's -9% trend. The company is debt-free, enhancing its financial stability and allowing for high-quality earnings. Trading at 32.7% below estimated fair value, it presents a potential opportunity for investors seeking value in smaller companies. Recent guidance suggests net profit could rise between 75% to 100%, driven by increased hospital coverage and overseas revenue growth, alongside enhanced operating efficiency from supply chain improvements and cost-saving measures.

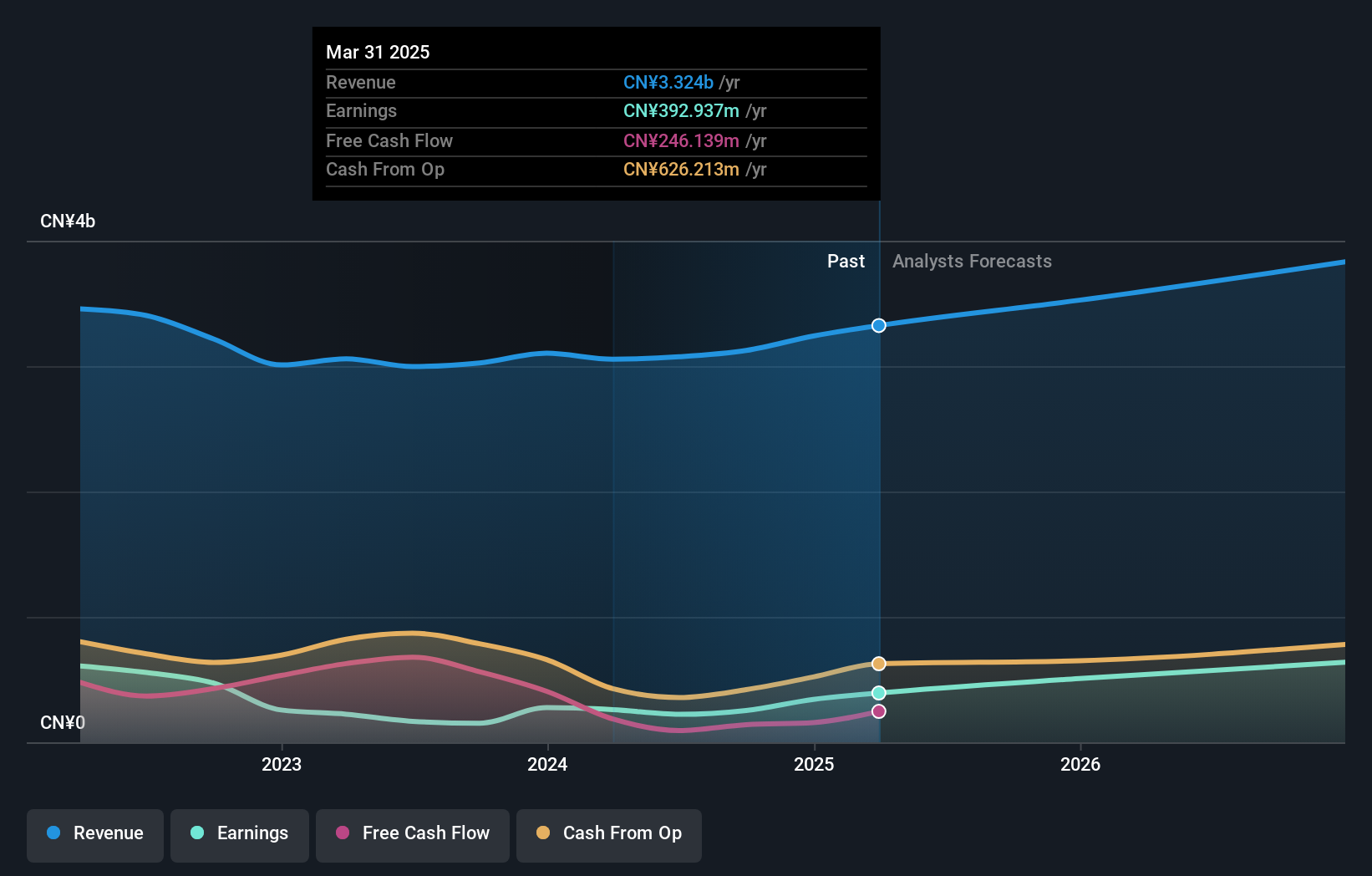

Xiamen Kingdomway Group (SZSE:002626)

Simply Wall St Value Rating: ★★★★★★

Overview: Xiamen Kingdomway Group Company is involved in the manufacturing and sale of nutrition and health products both in China and internationally, with a market cap of CN¥9.44 billion.

Operations: Xiamen Kingdomway Group generates revenue primarily from the sale of nutrition and health products. The company has a market cap of CN¥9.44 billion, reflecting its scale in the industry.

Xiamen Kingdomway Group, a dynamic player in the pharmaceutical sector, has demonstrated robust growth with earnings surging 66.9% over the past year, outpacing industry trends. Its price-to-earnings ratio of 37.2x is attractively below the CN market average of 39.2x, suggesting potential value for investors. The company boasts high-quality earnings and a solid financial footing with more cash than total debt, reflecting prudent management of resources. Over five years, its debt-to-equity ratio improved from 44.4% to 26.8%, enhancing financial stability and positioning it well for future expansion opportunities within its sector.

- Delve into the full analysis health report here for a deeper understanding of Xiamen Kingdomway Group.

Gain insights into Xiamen Kingdomway Group's past trends and performance with our Past report.

Where To Now?

- Get an in-depth perspective on all 2598 Asian Undiscovered Gems With Strong Fundamentals by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:SEVN

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|7.9% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|21.8% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|33.6% undervalued

DZ

Community Contributor