Advertisement

- New Zealand

- /

- Medical Equipment

- /

- NZSE:FPH

Why The 41% Return On Capital At Fisher & Paykel Healthcare (NZSE:FPH) Should Have Your Attention

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at the ROCE trend of Fisher & Paykel Healthcare (NZSE:FPH) we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Fisher & Paykel Healthcare, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

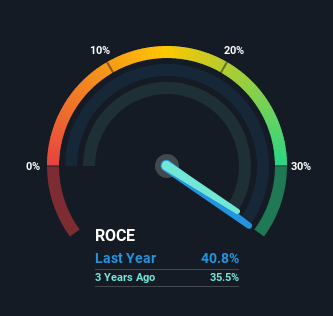

0.41 = NZ$706m ÷ (NZ$2.0b - NZ$314m) (Based on the trailing twelve months to September 2021).

Therefore, Fisher & Paykel Healthcare has an ROCE of 41%. In absolute terms that's a great return and it's even better than the Medical Equipment industry average of 15%.

Check out our latest analysis for Fisher & Paykel Healthcare

In the above chart we have measured Fisher & Paykel Healthcare's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Fisher & Paykel Healthcare.

What The Trend Of ROCE Can Tell Us

Fisher & Paykel Healthcare is displaying some positive trends. Over the last five years, returns on capital employed have risen substantially to 41%. The amount of capital employed has increased too, by 157%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

In Conclusion...

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what Fisher & Paykel Healthcare has. Since the stock has returned a staggering 318% to shareholders over the last five years, it looks like investors are recognizing these changes. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

On the other side of ROCE, we have to consider valuation. That's why we have a FREE intrinsic value estimation on our platform that is definitely worth checking out.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:FPH

Fisher & Paykel Healthcare

Designs, manufactures, markets, and sells medical device products and systems in North America, Europe, the Asia Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor