Advertisement

- New Zealand

- /

- Medical Equipment

- /

- NZSE:FPH

We Think Fisher & Paykel Healthcare (NZSE:FPH) Can Stay On Top Of Its Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Fisher & Paykel Healthcare Corporation Limited (NZSE:FPH) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Fisher & Paykel Healthcare

What Is Fisher & Paykel Healthcare's Net Debt?

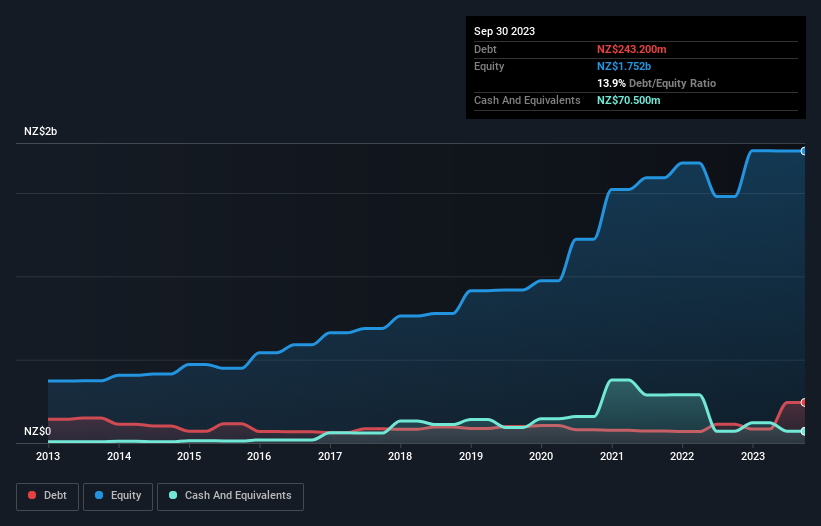

You can click the graphic below for the historical numbers, but it shows that as of September 2023 Fisher & Paykel Healthcare had NZ$243.2m of debt, an increase on NZ$112.4m, over one year. However, it also had NZ$70.5m in cash, and so its net debt is NZ$172.7m.

How Healthy Is Fisher & Paykel Healthcare's Balance Sheet?

According to the last reported balance sheet, Fisher & Paykel Healthcare had liabilities of NZ$286.8m due within 12 months, and liabilities of NZ$351.2m due beyond 12 months. Offsetting these obligations, it had cash of NZ$70.5m as well as receivables valued at NZ$261.9m due within 12 months. So its liabilities total NZ$305.6m more than the combination of its cash and short-term receivables.

Given Fisher & Paykel Healthcare has a market capitalization of NZ$13.9b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. But either way, Fisher & Paykel Healthcare has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Fisher & Paykel Healthcare's net debt is only 0.39 times its EBITDA. And its EBIT covers its interest expense a whopping 87.3 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Fisher & Paykel Healthcare grew its EBIT by 8.5% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Fisher & Paykel Healthcare's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Fisher & Paykel Healthcare recorded free cash flow of 27% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Happily, Fisher & Paykel Healthcare's impressive interest cover implies it has the upper hand on its debt. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. We would also note that Medical Equipment industry companies like Fisher & Paykel Healthcare commonly do use debt without problems. When we consider the range of factors above, it looks like Fisher & Paykel Healthcare is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Fisher & Paykel Healthcare insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:FPH

Fisher & Paykel Healthcare

Designs, manufactures, markets, and sells medical device products and systems in North America, Europe, the Asia Pacific, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor