Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Fisher & Paykel Healthcare Corporation Limited (NZSE:FPH) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Fisher & Paykel Healthcare

What Is Fisher & Paykel Healthcare's Debt?

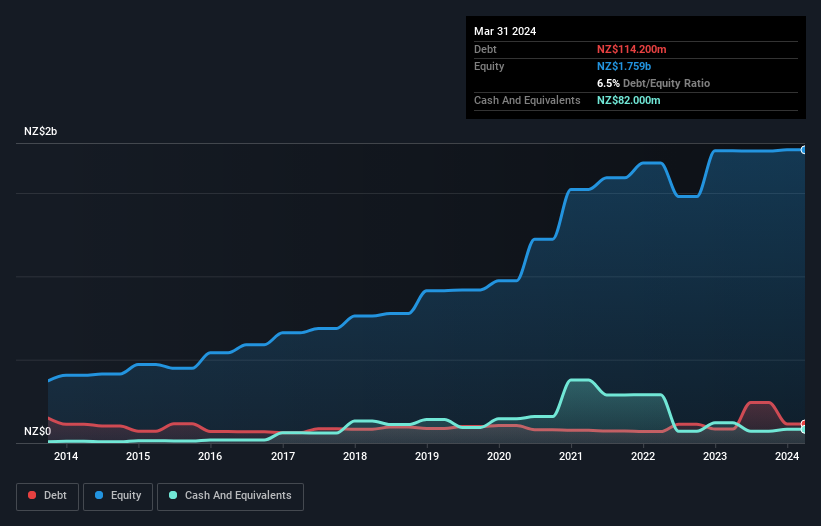

You can click the graphic below for the historical numbers, but it shows that as of March 2024 Fisher & Paykel Healthcare had NZ$114.2m of debt, an increase on NZ$83.3m, over one year. However, because it has a cash reserve of NZ$82.0m, its net debt is less, at about NZ$32.2m.

How Strong Is Fisher & Paykel Healthcare's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Fisher & Paykel Healthcare had liabilities of NZ$385.0m due within 12 months and liabilities of NZ$137.6m due beyond that. Offsetting these obligations, it had cash of NZ$82.0m as well as receivables valued at NZ$266.2m due within 12 months. So its liabilities total NZ$174.4m more than the combination of its cash and short-term receivables.

This state of affairs indicates that Fisher & Paykel Healthcare's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the NZ$18.5b company is struggling for cash, we still think it's worth monitoring its balance sheet. But either way, Fisher & Paykel Healthcare has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With debt at a measly 0.072 times EBITDA and EBIT covering interest a whopping 23.7 times, it's clear that Fisher & Paykel Healthcare is not a desperate borrower. Indeed relative to its earnings its debt load seems light as a feather. Fortunately, Fisher & Paykel Healthcare grew its EBIT by 6.4% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Fisher & Paykel Healthcare can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Fisher & Paykel Healthcare's free cash flow amounted to 23% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Fisher & Paykel Healthcare's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. We would also note that Medical Equipment industry companies like Fisher & Paykel Healthcare commonly do use debt without problems. Taking all this data into account, it seems to us that Fisher & Paykel Healthcare takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Fisher & Paykel Healthcare that you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NZSE:FPH

Fisher & Paykel Healthcare

Designs, manufactures, markets, and sells medical device products and systems in North America, Europe, the Asia Pacific, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Community Narratives