- New Zealand

- /

- Food

- /

- NZSE:LIC

Do These 3 Checks Before Buying Livestock Improvement Corporation Limited (NZSE:LIC) For Its Upcoming Dividend

It looks like Livestock Improvement Corporation Limited (NZSE:LIC) is about to go ex-dividend in the next 4 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. In other words, investors can purchase Livestock Improvement's shares before the 1st of August in order to be eligible for the dividend, which will be paid on the 16th of August.

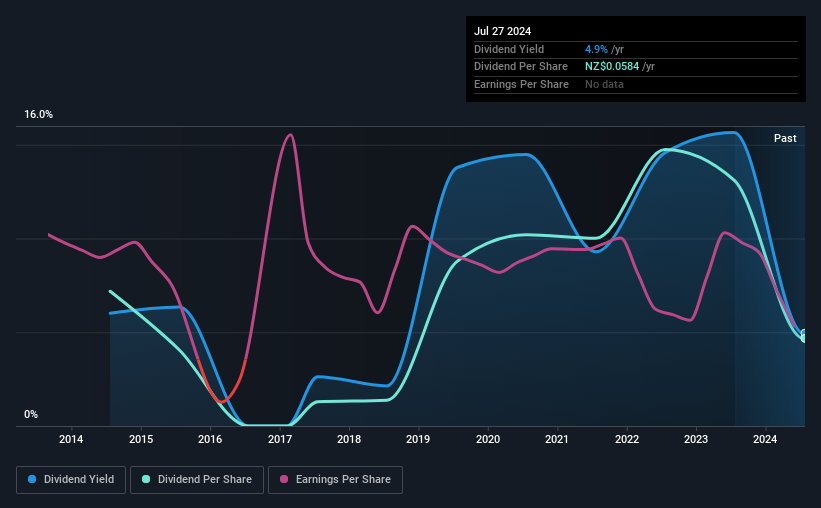

The company's next dividend payment will be NZ$0.0584046 per share, and in the last 12 months, the company paid a total of NZ$0.058 per share. Based on the last year's worth of payments, Livestock Improvement has a trailing yield of 5.0% on the current stock price of NZ$1.18. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Check out our latest analysis for Livestock Improvement

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Livestock Improvement distributed an unsustainably high 117% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Over the last year, it paid out dividends equivalent to 310% of what it generated in free cash flow, a disturbingly high percentage. It's pretty hard to pay out more than you earn, so we wonder how Livestock Improvement intends to continue funding this dividend, or if it could be forced to cut the payment.

Livestock Improvement does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Cash is slightly more important than profit from a dividend perspective, but given Livestock Improvement's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

Click here to see how much of its profit Livestock Improvement paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. Readers will understand then, why we're concerned to see Livestock Improvement's earnings per share have dropped 19% a year over the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Livestock Improvement's dividend payments per share have declined at 4.2% per year on average over the past 10 years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

The Bottom Line

Should investors buy Livestock Improvement for the upcoming dividend? It's looking like an unattractive opportunity, with its earnings per share declining, while, paying out an uncomfortably high percentage of both its profits (117%) and cash flow as dividends. This is a starkly negative combination that often suggests a dividend cut could be in the company's near future. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

So if you're still interested in Livestock Improvement despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. To that end, you should learn about the 6 warning signs we've spotted with Livestock Improvement (including 2 which are a bit concerning).

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NZSE:LIC

Livestock Improvement

Engages in the development, production and marketing of artificial breeding, genetics, farm software, and herd testing services in the dairy industry.

Flawless balance sheet medium-low.