Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Foley Wines Limited (NZSE:FWL) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Foley Wines

How Much Debt Does Foley Wines Carry?

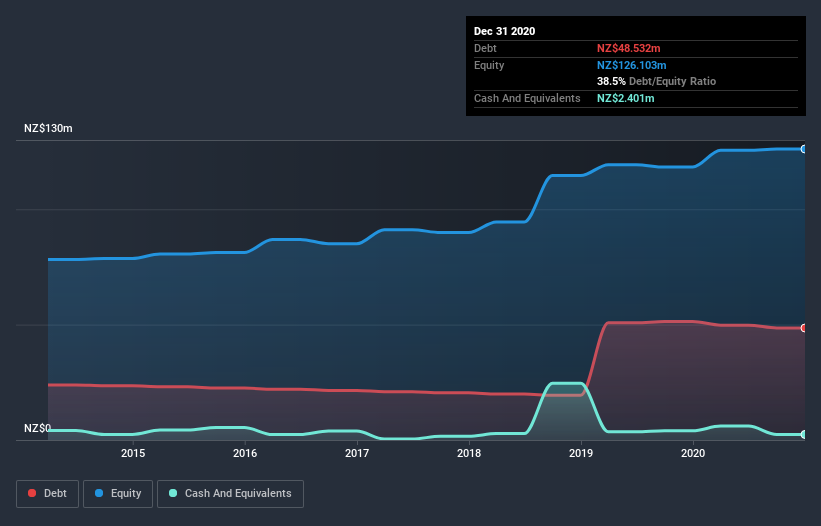

You can click the graphic below for the historical numbers, but it shows that Foley Wines had NZ$48.5m of debt in December 2020, down from NZ$51.3m, one year before. On the flip side, it has NZ$2.40m in cash leading to net debt of about NZ$46.1m.

A Look At Foley Wines' Liabilities

The latest balance sheet data shows that Foley Wines had liabilities of NZ$18.1m due within a year, and liabilities of NZ$62.4m falling due after that. On the other hand, it had cash of NZ$2.40m and NZ$8.28m worth of receivables due within a year. So it has liabilities totalling NZ$69.9m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Foley Wines has a market capitalization of NZ$121.6m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Foley Wines's debt is 3.2 times its EBITDA, and its EBIT cover its interest expense 6.0 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. One way Foley Wines could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 14%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Foley Wines's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Foley Wines recorded free cash flow of 45% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Neither Foley Wines's ability handle its debt, based on its EBITDA, nor its level of total liabilities gave us confidence in its ability to take on more debt. But we do take some comfort from its EBIT growth rate. Looking at all the angles mentioned above, it does seem to us that Foley Wines is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with Foley Wines .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Foley Wines, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:FWL

Foley Wines

An integrated wine company, produces, markets, and sells wines in New Zealand.

Slight and slightly overvalued.

Market Insights

Community Narratives