- United Kingdom

- /

- Specialty Stores

- /

- LSE:WIX

Undervalued European Small Caps With Insider Action In April 2025

Reviewed by Simply Wall St

European markets have faced a challenging environment recently, with the pan-European STOXX Europe 600 Index declining by 1.4% following new U.S. trade tariffs that dampened investor sentiment despite some positive economic updates earlier in the week. Amid this backdrop, identifying promising small-cap stocks can be particularly appealing for investors looking to navigate these uncertain times, as these companies may offer unique growth opportunities and resilience in a volatile market landscape.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Tristel | 22.9x | 3.2x | 41.06% | ★★★★★★ |

| Bytes Technology Group | 22.5x | 5.7x | 12.48% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 45.77% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 27.56% | ★★★★★☆ |

| Savills | 24.1x | 0.5x | 38.25% | ★★★★☆☆ |

| Seeing Machines | NA | 2.0x | 41.61% | ★★★★☆☆ |

| Axactor | NA | 1.0x | 0.40% | ★★★★☆☆ |

| FRP Advisory Group | 12.2x | 2.2x | 11.65% | ★★★☆☆☆ |

| Arendals Fossekompani | 20.8x | 1.6x | 47.58% | ★★★☆☆☆ |

| Elmera Group | 10.9x | 0.3x | -124.95% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

J D Wetherspoon (LSE:JDW)

Simply Wall St Value Rating: ★★★★★☆

Overview: J D Wetherspoon operates a chain of pubs across the UK and Ireland, focusing on offering food and drinks at competitive prices, with a market capitalization of approximately £1.05 billion.

Operations: Revenue is primarily generated from the pubs segment, with a gross profit margin of 11.26% as of early 2025. The cost of goods sold (COGS) represents a significant portion of expenses, amounting to £1.84 billion for the same period. Operating expenses have shown some variability over time, recently recorded at £99.87 million in early 2025.

PE: 10.5x

J D Wetherspoon, known for its extensive pub network, recently reported a rise in half-year sales to £1.03 billion and net income of £32.23 million. They announced an interim dividend of 4 pence per share after a previous nil payout, reflecting improved financial health. Insider confidence is evident from recent share repurchases authorized up to 15% of issued capital. While earnings are projected to grow by 5.84% annually, reliance on external borrowing poses some risk amidst their growth strategy.

- Dive into the specifics of J D Wetherspoon here with our thorough valuation report.

Evaluate J D Wetherspoon's historical performance by accessing our past performance report.

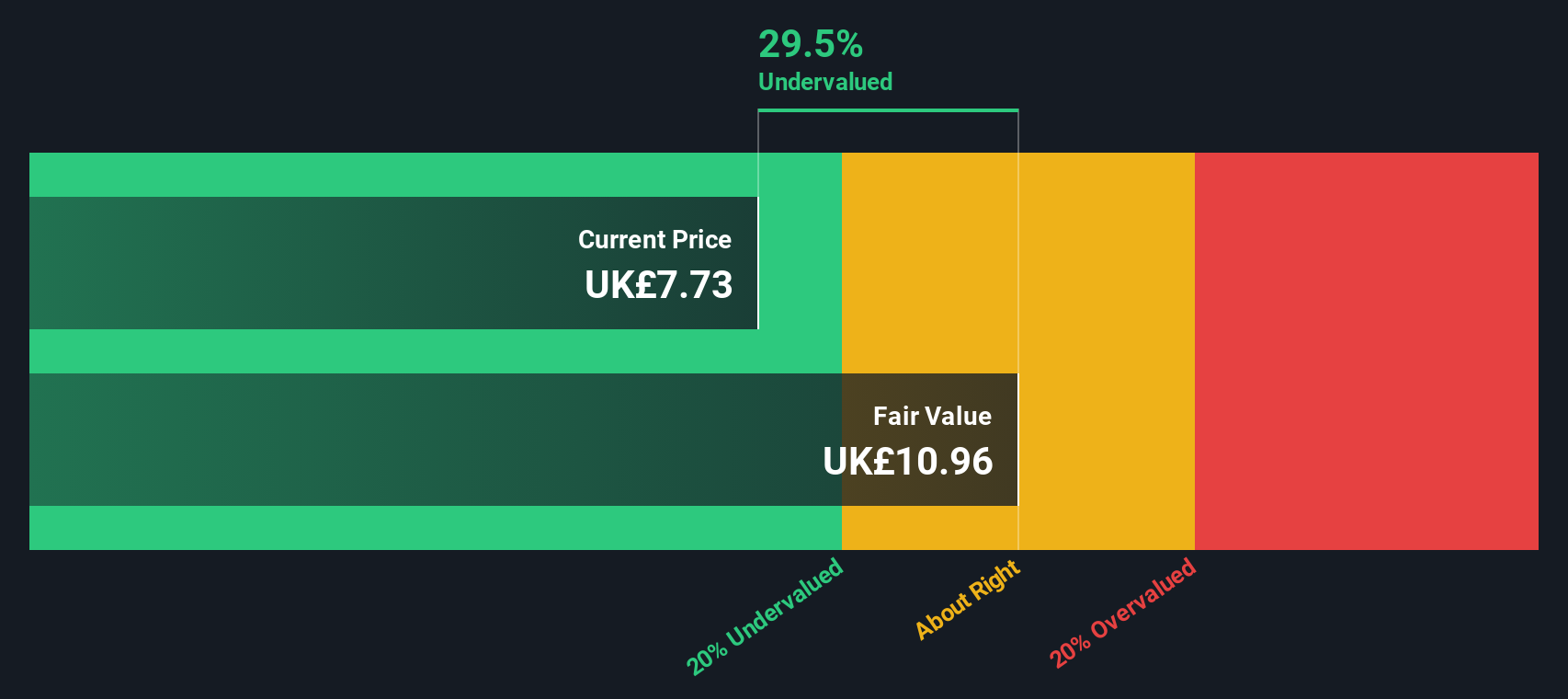

Wickes Group (LSE:WIX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Wickes Group is a UK-based company specializing in the retail of home improvement products and services, with a market capitalization of approximately £0.44 billion.

Operations: The company generates revenue primarily from the retail of home improvement products and services, with recent figures showing £1.54 billion in revenue. Its cost structure includes significant components such as cost of goods sold (COGS), operating expenses, and non-operating expenses. The net income margin has shown variability over the periods, with a recent figure at 1.18%.

PE: 23.8x

Wickes Group, a European small-cap, is navigating challenges with its recent financials showing a dip in net income to £18.1 million from £29.8 million the previous year and profit margins narrowing to 1.2% from 1.9%. Despite these figures, insider confidence is evident through share repurchase plans worth up to £20 million aimed at reducing capital. The company forecasts earnings growth of 29% annually and maintains dividends with a final payout of 7.3 pence per share for FY2024, indicating strategic efforts towards shareholder value amidst external borrowings as its primary funding source.

- Click here to discover the nuances of Wickes Group with our detailed analytical valuation report.

Gain insights into Wickes Group's past trends and performance with our Past report.

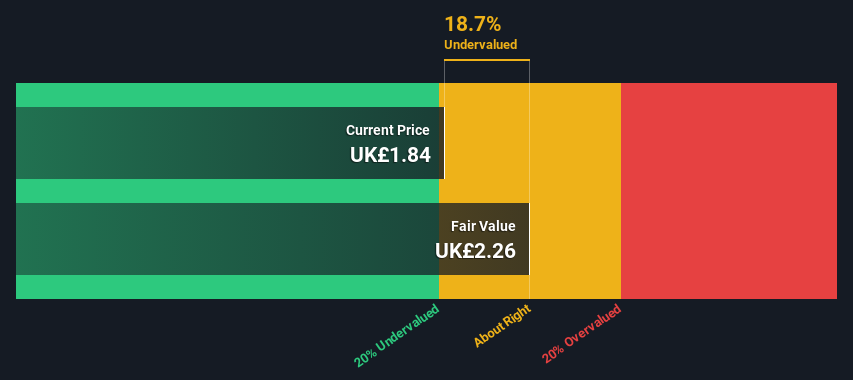

Elmera Group (OB:ELMRA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Elmera Group operates across various segments including Nordic, Business, Consumer, and New Growth Initiatives, with a market capitalization of NOK 10.8 billion.

Operations: The company generates revenue primarily from its Consumer and Business segments, with the Consumer segment contributing the largest share. Over recent periods, it has experienced fluctuations in its gross profit margin, reaching a high of 44.07% in December 2020 and a low of 6.25% in June 2023. Operating expenses have consistently included significant depreciation and amortization costs, impacting overall profitability.

PE: 10.9x

Elmera Group, a small European company, has recently caught attention due to insider confidence demonstrated by their Executive VP & CFO purchasing 10,000 shares for NOK 325,000 in March 2025. Despite facing challenges with external borrowing as its sole funding source, the company reported improved earnings for Q4 and full-year 2024. Sales decreased but net income rose to NOK 206 million from NOK 88 million in Q4 year-over-year. A proposed dividend increase to NOK 3 per share reflects positive future prospects.

- Unlock comprehensive insights into our analysis of Elmera Group stock in this valuation report.

Assess Elmera Group's past performance with our detailed historical performance reports.

Seize The Opportunity

- Gain an insight into the universe of 64 Undervalued European Small Caps With Insider Buying by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Wickes Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wickes Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:WIX

Wickes Group

Operates as a retailer of home repair, maintenance, and improvement products and services in the United Kingdom.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives