If you are holding or eyeing shares of Höegh Autoliners (OB:HAUTO), the latest moves may have prompted a second look. While there has not been a headline-grabbing announcement driving attention, the recent stock activity has nonetheless raised questions about the underlying value and prospects for this Norwegian auto shipping company. For investors used to sharp event-driven surges, this quieter spell might feel like a moment to reassess whether momentum is building beneath the surface.

Stepping back, Höegh Autoliners has seen its shares climb 15% over the past year, which likely reflects shifting expectations rather than a sudden rush of optimism. Despite a strong three-month stretch, which saw a 26% gain, the company’s year-to-date performance is actually down by nearly 6%. This mixed picture comes as Höegh faces challenges in annual revenue and earnings growth, and follows a period of outsized long-term returns that have caught the eye of more valuation-conscious investors.

With that in mind, the real question is clear: Is Höegh Autoliners cheap based on what it has already achieved, or have investors already factored all potential growth into the share price?

Advertisement

Most Popular Narrative: 18.9% Overvalued

The prevailing narrative points to Höegh Autoliners trading well above what is considered its fair value, suggesting investors should tread carefully before expecting further upside from current levels.

Rising tariffs, port fees, and regulatory headwinds in key export markets are expected to structurally increase Höegh's shipping costs and ultimately lower transported volumes. This could directly pressure revenues and potentially compress net margins over time. The global acceleration of electric vehicle adoption, combined with a trend toward more localized production, is likely to reduce long-term transoceanic car exports and diminish the addressable market, weighing on Höegh's future volume growth and top-line expansion.

Is this market pricing too optimistic or could major growth headwinds be ahead? The story hinges on dramatic margin shifts, evolving trade flows, and a future valuation multiple that raises eyebrows. Curious which numbers are behind this bold call? There are key financial assumptions and forecasts driving this high-stakes figure. Discover the exact projections that underpin the narrative's fair value.

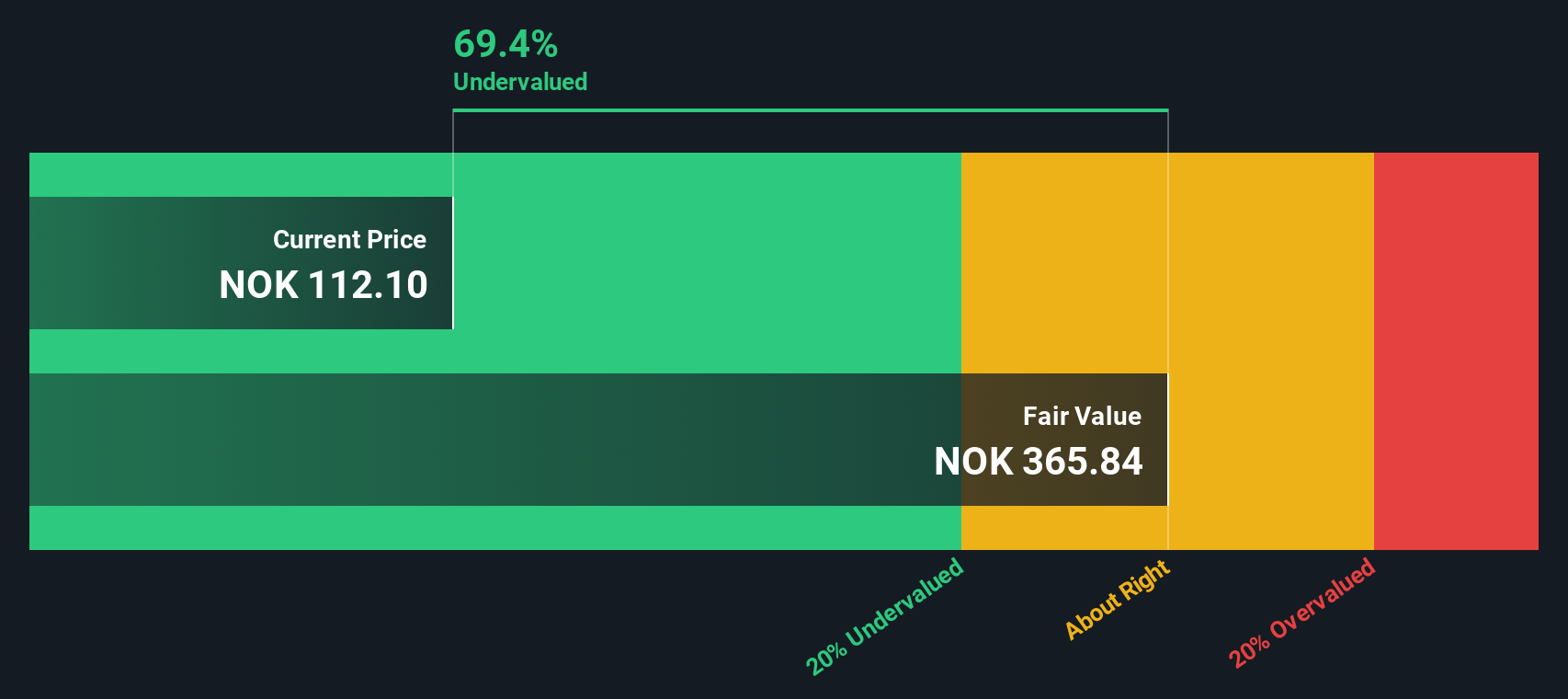

Another View: Discounted Cash Flow Tells a Different Story

Looking from another angle, our SWS DCF model suggests the shares could be trading well below their intrinsic value. This challenges the multiples-based case that the stock is already overvalued. Could the market be missing something?

Stay updated when valuation signals shift by adding Höegh Autoliners to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Höegh Autoliners Narrative

If you would rather take a hands-on approach or have your own perspective to add, it only takes a few minutes to build your own view from the data. Do it your way

A great starting point for your Höegh Autoliners research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Stay ahead of the curve by using Simply Wall Street's powerful tools to spot promising companies in booming industries and fast-changing markets. Uncover hidden gems, sector leaders, and tomorrow’s top performers before the broader market catches on.

Tap into the explosive growth and innovation fueling modern healthcare by screening for healthcare AI stocks.

Capitalize on mispriced opportunities and invest with confidence by targeting stocks undervalued stocks based on cash flows based on their true cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Höegh Autoliners might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.