Advertisement

LINK Mobility (OB:LINK) Margin Compression Challenges Bullish Growth Narratives

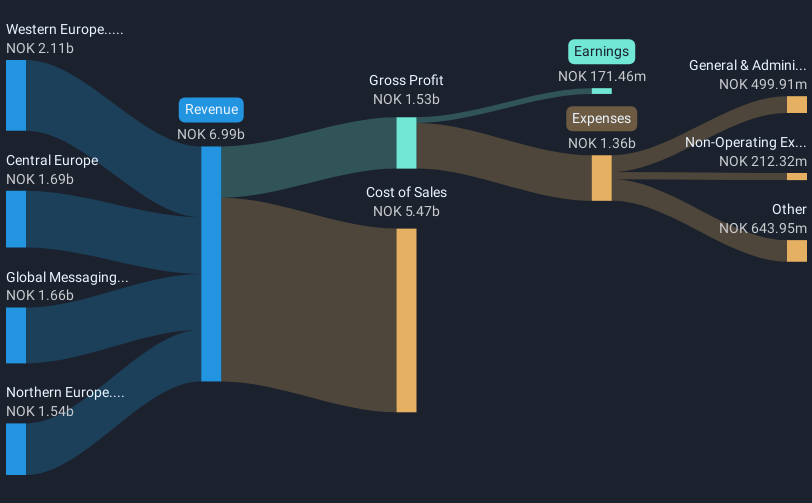

LINK Mobility Group Holding (OB:LINK) has just posted its FY 2025 numbers, with fourth quarter revenue of NOK1.98b and basic EPS of NOK0.10 setting the tone for a year where trailing 12 month revenue came in at NOK7.08b and EPS at NOK0.28. Over recent quarters the company has seen revenue move between NOK1.65b and NOK1.98b, while quarterly EPS ranged from close to zero to NOK0.13, giving investors a mixed but readable picture of earnings power. With trailing net margins sitting in the low single digits and a one off loss still in the rear view mirror, this update keeps the focus firmly on how sustainably the business can turn revenue into profit.

See our full analysis for LINK Mobility Group Holding.With the latest figures in hand, the next step is to line these results up against the key narratives around LINK Mobility, and test where the growth story, margin profile and risk views match the data and where they start to diverge.

See what the community is saying about LINK Mobility Group Holding

TTM net margin at 1.2% with NOK81.6m one off loss in the mix

- Over the last 12 months, LINK generated NOK7.1b of revenue with net margin of 1.2%, compared with 2.5% in the prior year period, and that period also included a one off loss of NOK81.6m that weighed on reported profitability.

- Consensus narrative sees rising demand for higher margin CPaaS and omnichannel products as a key support for future margins. However, the dip from 2.5% to 1.2%, together with the NOK81.6m one off loss, shows that recent profitability is still sensitive to cost items and mix effects, which may make it harder for that margin improvement story to show up cleanly in near term reported numbers.

Quarterly net income swings highlight earnings sensitivity

- Within FY 2025, net income excluding extra items swung between a loss of NOK0.05m in Q2 and a profit of NOK39.3m in Q1 and NOK30.8m in Q4, even though quarterly revenue stayed within a relatively narrow NOK1.65b to NOK1.98b band.

- Bears argue that dependence on legacy SMS and acquisitions makes earnings fragile, and the move from a small loss in Q2 2025 to NOK30.8m profit in Q4 supports the view that earnings are quite exposed to volume, pricing and integration effects. This lines up with concerns about competition, regulation and M&A execution weighing on the stability of the income line.

High P/E of 72.8x despite DCF fair value of NOK64.45

- LINK trades on a P/E of 72.8x versus European software peers at 22.2x and a peer group at 18.9x, even though the current share price of NOK21.90 sits far below a DCF fair value estimate of NOK64.45 and below an analyst price target of NOK41.25.

- Critics highlight this rich 72.8x P/E as a key risk. They argue that if the strong earnings growth forecasts of about 51.8% per year and revenue growth of 12.4% do not come through as expected, the gap to peer multiples could matter more for returns than the upside implied by the DCF fair value and analyst target.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for LINK Mobility Group Holding on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? If this data is sparking a different conclusion for you, shape that view into your own narrative in just a few minutes, Do it your way

A great starting point for your LINK Mobility Group Holding research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Explore Alternatives

LINK Mobility’s thin 1.2% net margin, earnings swings despite steady revenue, and a high 72.8x P/E highlight pressure on profitability and valuation risk.

If those tight margins and valuation worries make you cautious about concentration in one name, spread your research across our 323 resilient stocks with low risk scores and see how steadier profiles compare today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OB:LINK

LINK Mobility Group Holding

Provides mobile and communication-platform-as-a-service solutions.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7060.2% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.226.4% undervalued

32 followersusers have followed this narrative

7 commentsusers have commented on this narrative

10 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0542.8% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.9% undervalued

85 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

WI

Wizkhalifa on PSP Energy Berhad ·

PSP Energy Breaks Key Downtrend, Momentum Building for Further Upside

Fair Value:RM 0.09252.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Indofood CBP Sukses Makmur ·

Blindly Bullish on Indofood CBP Sukses Makmur's 5.3% Revenue Growth

Fair Value:Rp9.05k30.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CSL ·

CSL Investment Thesis

Fair Value:AU$14023.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9724.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1935.7% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0