David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that REC Silicon ASA (OB:REC) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View 4 warning signs we detected for REC Silicon

How Much Debt Does REC Silicon Carry?

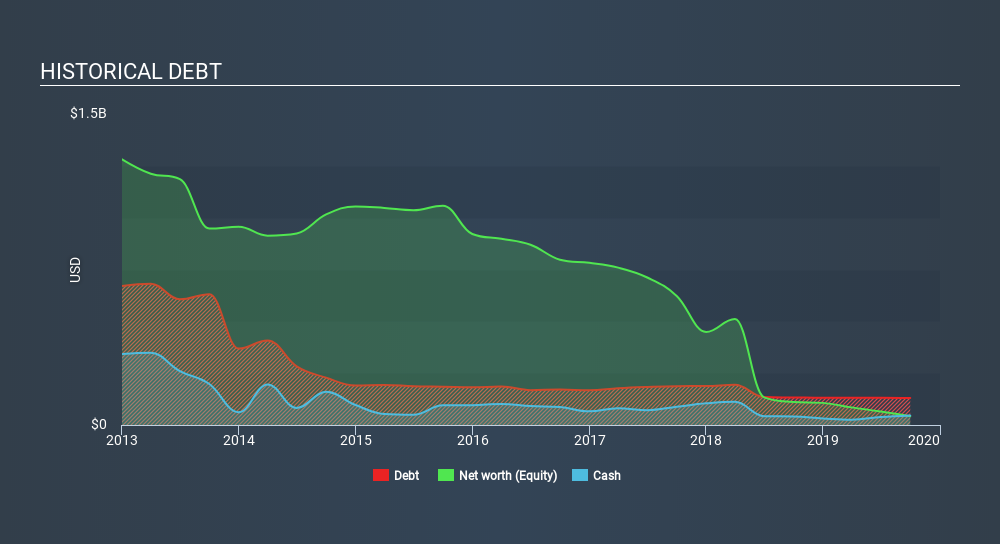

The image below, which you can click on for greater detail, shows that at September 2019 REC Silicon had debt of US$130.5m, up from US$133 in one year. However, because it has a cash reserve of US$46.2m, its net debt is less, at about US$84.3m.

How Healthy Is REC Silicon's Balance Sheet?

According to the last reported balance sheet, REC Silicon had liabilities of US$126.1m due within 12 months, and liabilities of US$171.7m due beyond 12 months. Offsetting this, it had US$46.2m in cash and US$22.8m in receivables that were due within 12 months. So it has liabilities totalling US$228.8m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$78.2m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, REC Silicon would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if REC Silicon can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, REC Silicon made a loss at the EBIT level, and saw its revenue drop to US$177m, which is a fall of 29%. To be frank that doesn't bode well.

Caveat Emptor

While REC Silicon's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping US$60m. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely, given it is low on liquid assets, and burned through US$8.8m in the last year. So we consider this a high risk stock and we wouldn't be at all surprised if the company asks shareholders for money before long. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for REC Silicon which any shareholder or potential investor should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OB:RECSI

REC Silicon

Produces and sells silicon materials for the solar and electronics industries worldwide.

Undervalued with high growth potential.