This Is Why Gjensidige Forsikring ASA's (OB:GJF) CEO Can Expect A Bump Up In Their Pay Packet

Shareholders will be pleased by the robust performance of Gjensidige Forsikring ASA (OB:GJF) recently and this will be kept in mind in the upcoming AGM on 24 March 2021. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. In our analysis below, we discuss why we think the CEO compensation looks acceptable and the case for a raise.

See our latest analysis for Gjensidige Forsikring

How Does Total Compensation For Helge Baastad Compare With Other Companies In The Industry?

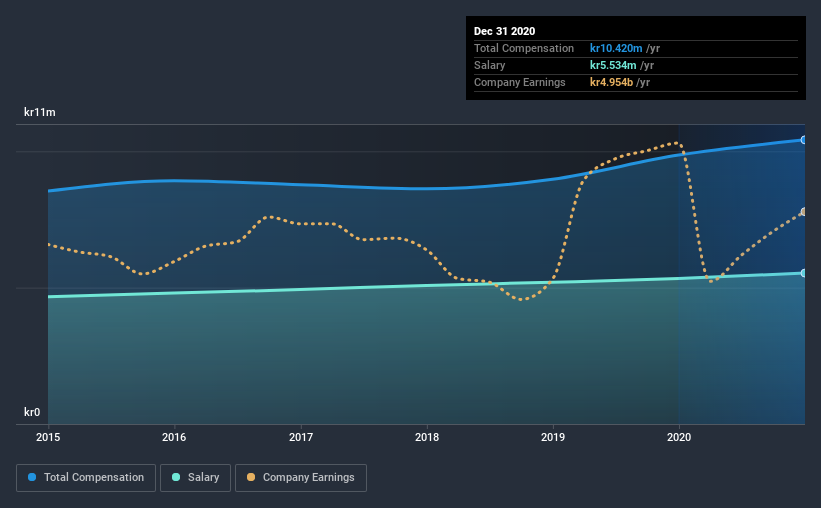

According to our data, Gjensidige Forsikring ASA has a market capitalization of kr102b, and paid its CEO total annual compensation worth kr10m over the year to December 2020. That's a fairly small increase of 5.7% over the previous year. We note that the salary of kr5.53m makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations over kr68b , the reported median total CEO compensation was kr43m. That is to say, Helge Baastad is paid under the industry median. Moreover, Helge Baastad also holds kr14m worth of Gjensidige Forsikring stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | kr5.5m | kr5.3m | 53% |

| Other | kr4.9m | kr4.5m | 47% |

| Total Compensation | kr10m | kr9.9m | 100% |

On an industry level, roughly 45% of total compensation represents salary and 55% is other remuneration. Gjensidige Forsikring is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Gjensidige Forsikring ASA's Growth

Gjensidige Forsikring ASA's earnings per share (EPS) grew 6.8% per year over the last three years. Revenue was pretty flat on last year.

We'd prefer higher revenue growth, but it is good to see modest EPS growth. So there are some positives here, but not enough to earn high praise. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Gjensidige Forsikring ASA Been A Good Investment?

Boasting a total shareholder return of 65% over three years, Gjensidige Forsikring ASA has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. If it continues on the same road, shareholders might feel even more confident about their investment, and have little to no objections concerning CEO pay. Rather, investors would more likely want to engage on discussions related to key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Gjensidige Forsikring that investors should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you decide to trade Gjensidige Forsikring, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Gjensidige Forsikring, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:GJF

Gjensidige Forsikring

Provides general insurance and pension products in Norway, Sweden, Denmark, Finland, Latvia, Lithuania, and Estonia.

Reasonable growth potential with proven track record and pays a dividend.