- Norway

- /

- Oil and Gas

- /

- OB:HUNT

We Believe That Hunter Group's (OB:HUNT) Weak Earnings Are A Good Indicator Of Underlying Profitability

Hunter Group ASA's (OB:HUNT) stock wasn't much affected by its recent lackluster earnings numbers. Our analysis suggests that they may be missing some concerning details underlying the profit numbers.

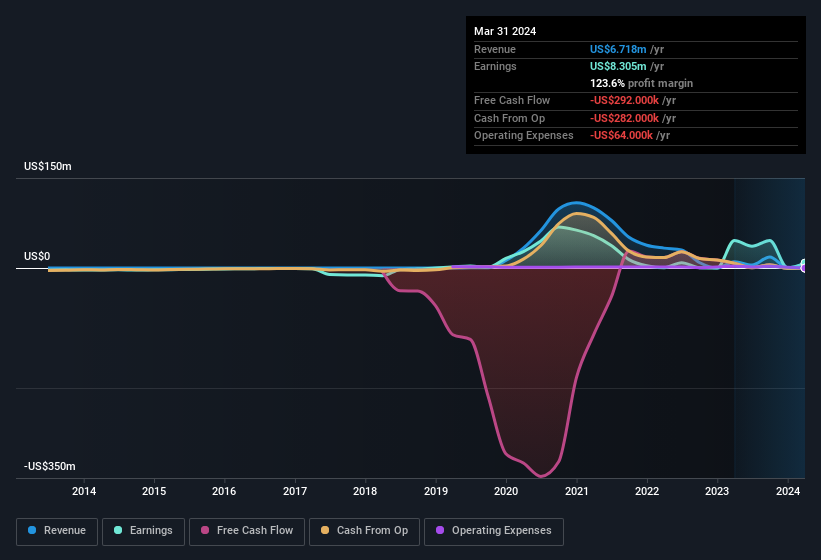

View our latest analysis for Hunter Group

Examining Cashflow Against Hunter Group's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to March 2024, Hunter Group recorded an accrual ratio of 3.24. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of US$292k, in contrast to the aforementioned profit of US$8.31m. We saw that FCF was US$8.0m a year ago though, so Hunter Group has at least been able to generate positive FCF in the past. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Hunter Group.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. Hunter Group expanded the number of shares on issue by 369% over the last year. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Hunter Group's EPS by clicking here.

A Look At The Impact Of Hunter Group's Dilution On Its Earnings Per Share (EPS)

Hunter Group's net profit dropped by 85% per year over the last three years. And even focusing only on the last twelve months, we see profit is down 82%. Sadly, earnings per share fell further, down a full 97% in that time. So you can see that the dilution has had a fairly significant impact on shareholders.

If Hunter Group's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Hunter Group's Profit Performance

In conclusion, Hunter Group has weak cashflow relative to earnings, which indicates lower quality earnings, and the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). On reflection, the above-mentioned factors give us the strong impression that Hunter Group'sunderlying earnings power is not as good as it might seem, based on the statutory profit numbers. So while earnings quality is important, it's equally important to consider the risks facing Hunter Group at this point in time. To help with this, we've discovered 6 warning signs (3 can't be ignored!) that you ought to be aware of before buying any shares in Hunter Group.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

If you're looking to trade Hunter Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hunter Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:HUNT

Hunter Group

An investment company, primarily focuses on the shipping and oil service investments in Norway and internationally.

Flawless balance sheet slight.

Market Insights

Community Narratives