Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Everfuel A/S (OB:EFUEL) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Everfuel

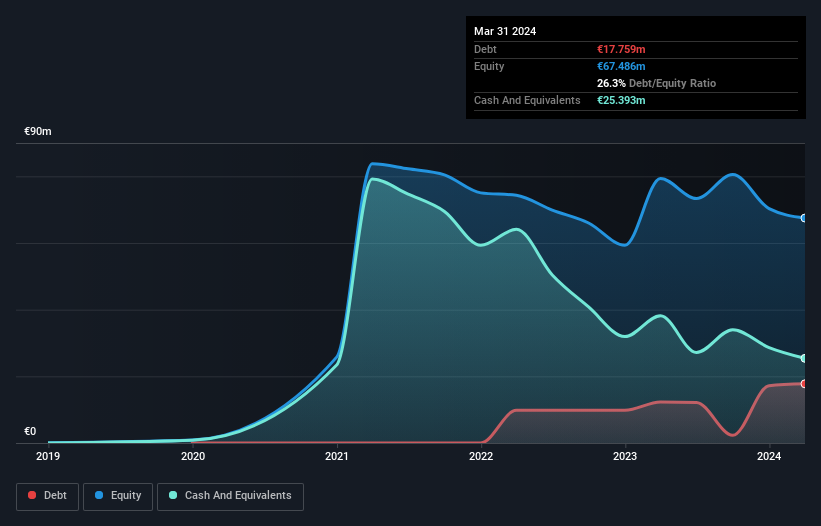

How Much Debt Does Everfuel Carry?

The image below, which you can click on for greater detail, shows that at March 2024 Everfuel had debt of €17.8m, up from €12.3m in one year. However, it does have €25.4m in cash offsetting this, leading to net cash of €7.63m.

How Strong Is Everfuel's Balance Sheet?

The latest balance sheet data shows that Everfuel had liabilities of €37.0m due within a year, and liabilities of €3.08m falling due after that. Offsetting these obligations, it had cash of €25.4m as well as receivables valued at €6.35m due within 12 months. So its liabilities total €8.34m more than the combination of its cash and short-term receivables.

Of course, Everfuel has a market capitalization of €93.6m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Everfuel boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Everfuel's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Everfuel wasn't profitable at an EBIT level, but managed to grow its revenue by 88%, to €5.4m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Everfuel?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Everfuel had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through €38m of cash and made a loss of €25m. With only €7.63m on the balance sheet, it would appear that its going to need to raise capital again soon. With very solid revenue growth in the last year, Everfuel may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Everfuel that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Everfuel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:EFUEL

Everfuel

Operates as an integrated green hydrogen fuel company in Denmark, the Netherlands, and Germany.

Low with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor