Advertisement

- Norway

- /

- Oil and Gas

- /

- OB:BNOR

These Analysts Just Made A Notable Downgrade To Their BlueNord ASA (OB:BNOR) EPS Forecasts

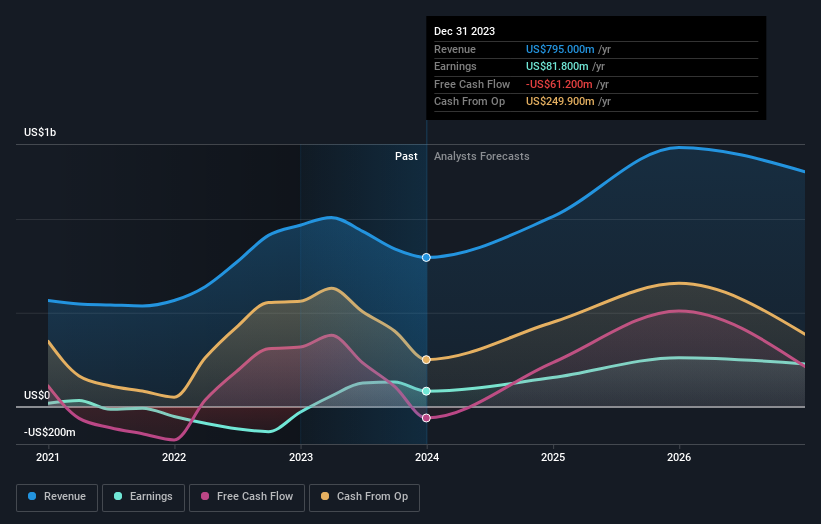

One thing we could say about the analysts on BlueNord ASA (OB:BNOR) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

After this downgrade, BlueNord's three analysts are now forecasting revenues of US$1.0b in 2024. This would be a sizeable 27% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to leap 87% to US$5.87. Previously, the analysts had been modelling revenues of US$1.2b and earnings per share (EPS) of US$8.10 in 2024. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a pretty serious decline to earnings per share numbers as well.

View our latest analysis for BlueNord

Despite the cuts to forecast earnings, there was no real change to the kr651 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We can infer from the latest estimates that forecasts expect a continuation of BlueNord'shistorical trends, as the 27% annualised revenue growth to the end of 2024 is roughly in line with the 33% annual revenue growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue shrink 3.2% annually. So it's clear that not only is revenue growth expected to be maintained, but BlueNord is expected to grow meaningfully faster than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for BlueNord. Unfortunately, they also downgraded their revenue estimates, and our data indicates sales are expected to outperform the wider market. Even so, earnings per share are more important to the intrinsic value of the business. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on BlueNord after the downgrade.

A high debt burden combined with a downgrade of this magnitude always gives us some reason for concern, especially if these forecasts are just the first sign of a business downturn. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

You can also see our analysis of BlueNord's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

Valuation is complex, but we're here to simplify it.

Discover if BlueNord might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:BNOR

BlueNord

An oil and gas company, engages in the production and development of resources that support the energy transition towards net zero in Norway, Denmark, the Netherlands, and the United Kingdom.

High growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor