Advertisement

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. So on that note, Bonheur (OB:BONHR) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Bonheur is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.15 = kr2.9b ÷ (kr25b - kr5.1b) (Based on the trailing twelve months to June 2023).

Therefore, Bonheur has an ROCE of 15%. In absolute terms, that's a satisfactory return, but compared to the Industrials industry average of 7.5% it's much better.

See our latest analysis for Bonheur

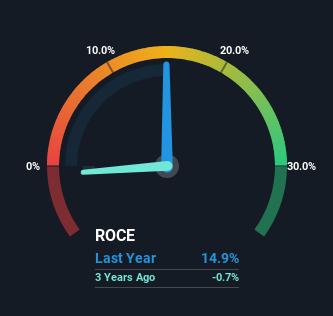

Historical performance is a great place to start when researching a stock so above you can see the gauge for Bonheur's ROCE against it's prior returns. If you'd like to look at how Bonheur has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

So How Is Bonheur's ROCE Trending?

Bonheur has not disappointed with their ROCE growth. More specifically, while the company has kept capital employed relatively flat over the last five years, the ROCE has climbed 269% in that same time. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. The company is doing well in that sense, and it's worth investigating what the management team has planned for long term growth prospects.

On a related note, the company's ratio of current liabilities to total assets has decreased to 21%, which basically reduces it's funding from the likes of short-term creditors or suppliers. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books.

What We Can Learn From Bonheur's ROCE

In summary, we're delighted to see that Bonheur has been able to increase efficiencies and earn higher rates of return on the same amount of capital. Since the stock has returned a staggering 131% to shareholders over the last five years, it looks like investors are recognizing these changes. In light of that, we think it's worth looking further into this stock because if Bonheur can keep these trends up, it could have a bright future ahead.

One final note, you should learn about the 2 warning signs we've spotted with Bonheur (including 1 which makes us a bit uncomfortable) .

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Bonheur might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:BONHR

Bonheur

Engages in the renewable energy, wind service, and cruise businesses in the United Kingdom, Norway, Europe, Asia, the Americas, Africa, and Internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor