- Netherlands

- /

- Capital Markets

- /

- ENXTAM:CVC

Top 3 Growth Companies With High Insider Ownership On Euronext Amsterdam

Reviewed by Simply Wall St

As global markets face renewed fears about economic growth, the Dutch market has not been immune to these concerns, with major indices reflecting a cautious sentiment. However, in this environment of uncertainty, companies with high insider ownership often signal strong confidence from those who know the business best. In this article, we explore three growth companies listed on Euronext Amsterdam that exhibit significant insider ownership. These firms stand out not only for their potential for expansion but also for the vested interest their leadership teams have in ensuring long-term success.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 36.7% | 82.7% |

| Ebusco Holding (ENXTAM:EBUS) | 33.2% | 107.8% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 77.1% |

| MotorK (ENXTAM:MTRK) | 35.7% | 108.4% |

| CVC Capital Partners (ENXTAM:CVC) | 20.2% | 32.6% |

| PostNL (ENXTAM:PNL) | 35.6% | 36.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

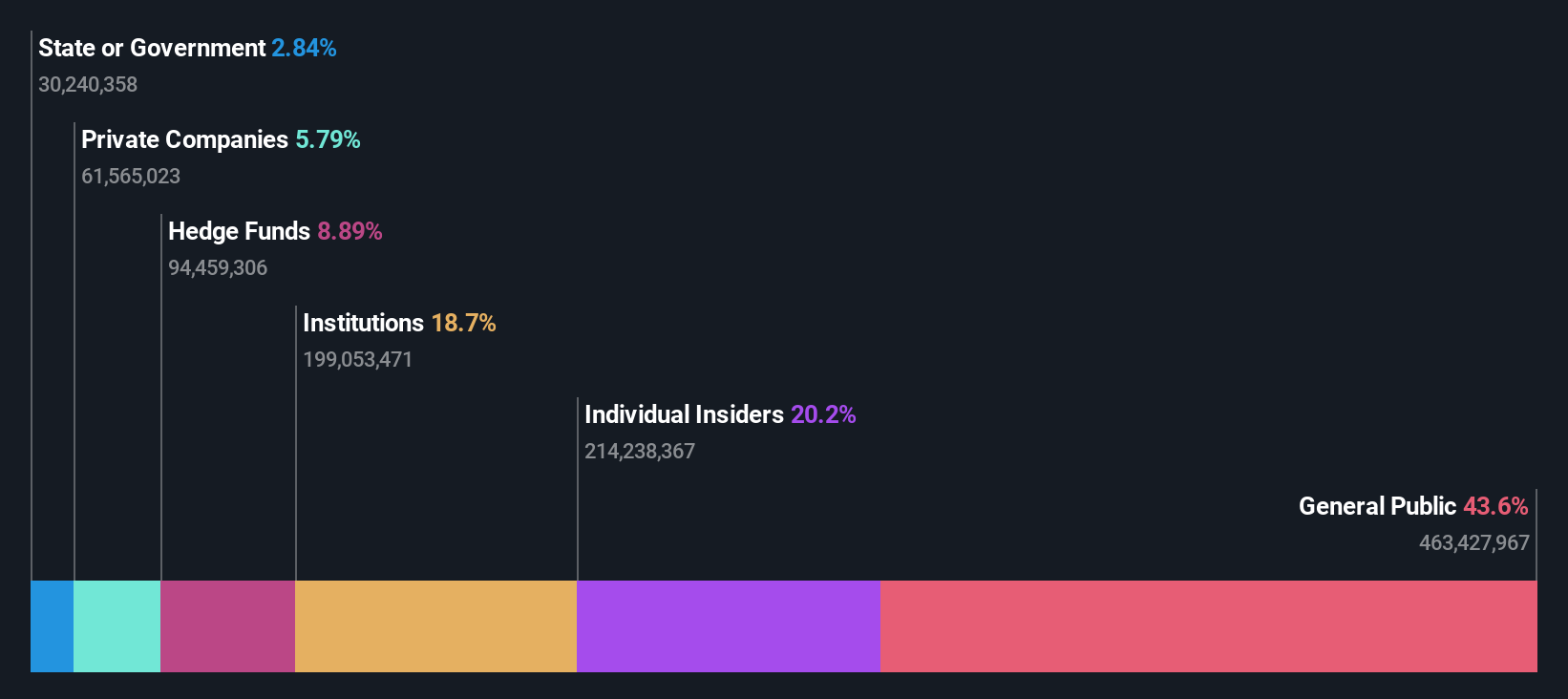

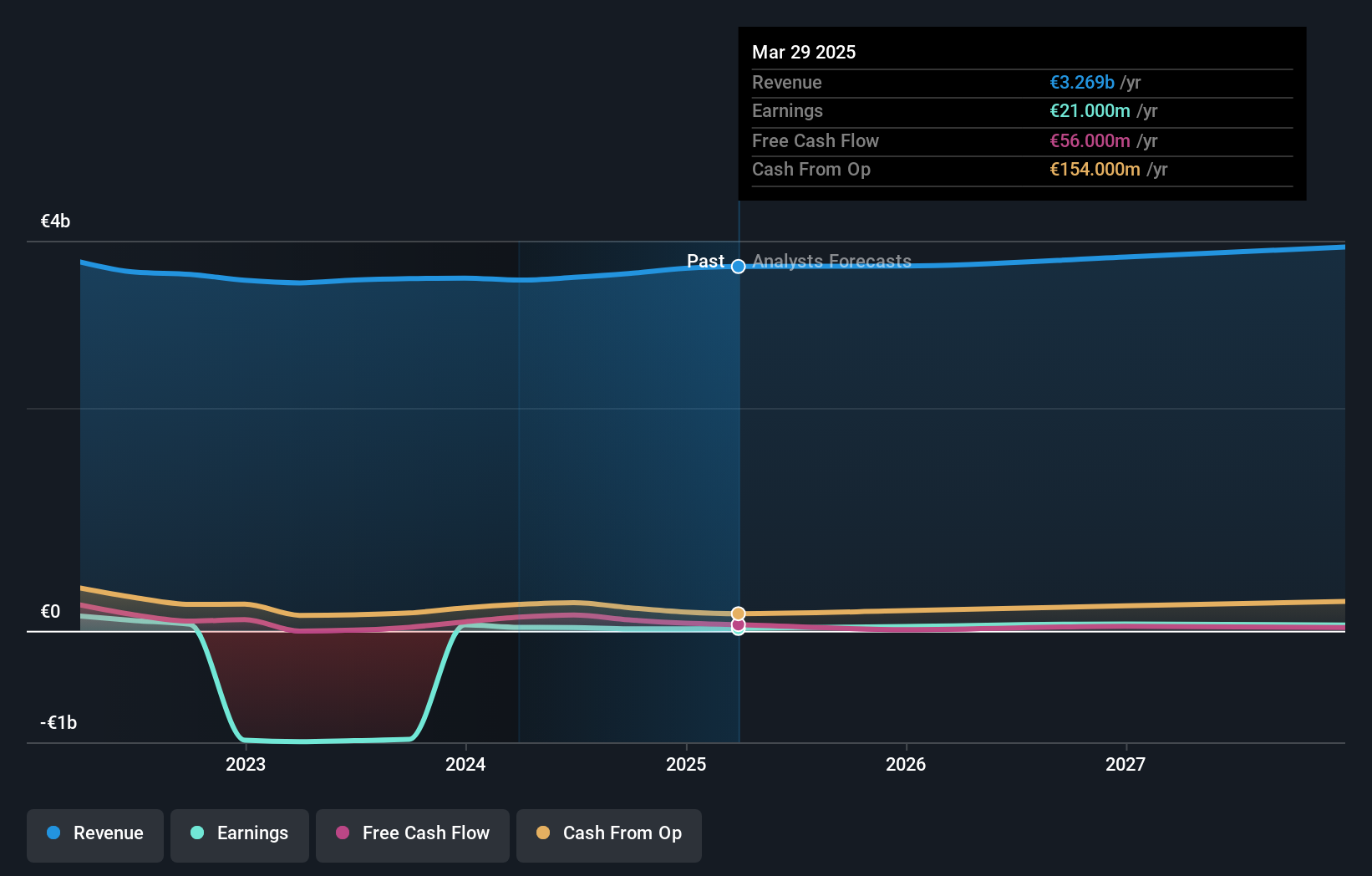

CVC Capital Partners (ENXTAM:CVC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CVC Capital Partners plc is a private equity and venture capital firm focusing on middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts with a market cap of €20.20 billion.

Operations: The firm's revenue segments include middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts.

Insider Ownership: 20.2%

CVC Capital Partners, a major private equity firm in the Netherlands, is forecast to grow earnings at 32.6% annually, significantly outpacing the Dutch market's 18.9%. Despite its high debt levels, CVC is trading at a 30.5% discount to its estimated fair value and has no substantial insider selling recently. Recent activities include leading bids for DB Schenker and Aavas Financiers, reflecting strong insider confidence and strategic growth initiatives.

- Click to explore a detailed breakdown of our findings in CVC Capital Partners' earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of CVC Capital Partners shares in the market.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. designs, develops, manufactures, assembles, markets, sells, leases, and services reverse vending machines to collect and process used beverage containers primarily in the Netherlands, North America, and Europe with a market cap of €305.76 million.

Operations: Envipco Holding N.V. generates revenue through the design, development, manufacturing, assembly, marketing, sales, leasing, and servicing of reverse vending machines for used beverage container collection and processing across the Netherlands, North America, and Europe.

Insider Ownership: 36.7%

Envipco Holding, with high insider ownership, is forecast to grow earnings at 82.7% annually and revenue at 35.5%, significantly outpacing the Dutch market. The company recently became profitable and reported Q2 sales of €26.57 million, up from €16.48 million a year ago, despite a net loss reduction to €0.532 million from €1.8 million. Recent AGM decisions include appointing new board members and changing auditors, reflecting strategic governance updates amidst volatile share prices.

- Unlock comprehensive insights into our analysis of Envipco Holding stock in this growth report.

- According our valuation report, there's an indication that Envipco Holding's share price might be on the expensive side.

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. provides postal and logistics services to businesses and consumers in the Netherlands, rest of Europe, and internationally, with a market cap of €598.01 million.

Operations: The company's revenue segments include Parcels (€2.28 billion) and Mail in The Netherlands (€1.35 billion).

Insider Ownership: 35.6%

PostNL, a growth company with high insider ownership, reported Q2 2024 sales of €793 million, up from €768 million a year ago. Despite this increase, net income slightly declined to €10 million from €11 million. The company has substantial debt and its dividend yield of 5.04% is not well covered by earnings. However, PostNL's earnings are forecast to grow at 36.38% annually over the next three years, significantly outpacing the Dutch market's growth rate of 18.9%.

- Take a closer look at PostNL's potential here in our earnings growth report.

- Our valuation report unveils the possibility PostNL's shares may be trading at a discount.

Next Steps

- Investigate our full lineup of 6 Fast Growing Euronext Amsterdam Companies With High Insider Ownership right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:CVC

CVC Capital Partners

A private equity and venture capital firm specializing in middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature, recapitalizations, strip sales, and spinouts.

High growth potential and slightly overvalued.