- Netherlands

- /

- Professional Services

- /

- ENXTAM:WKL

How Wolters Kluwer’s AI Tax And Clinical Tools Push (ENXTAM:WKL) Has Changed Its Investment Story

Reviewed by Sasha Jovanovic

- Earlier this week, Wolters Kluwer Tax & Accounting Germany launched SteuerSparErklärung Online, a browser-based tax filing platform that uses the AI assistant “Alma” to answer natural-language tax questions, while Wolters Kluwer Health’s Ovid Synthesis was adopted by the American Board of Medical Specialties Portfolio Program as an official quality improvement workflow tool.

- Together, these moves highlight Wolters Kluwer’s push to embed AI and cloud delivery into everyday professional workflows across both tax preparation and clinical quality improvement.

- We’ll now examine how this push into AI-enabled cloud tax filing shapes Wolters Kluwer’s broader investment narrative and long-term growth drivers.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Wolters Kluwer Investment Narrative Recap

To own Wolters Kluwer, you need to believe in its ability to keep shifting from print and on‑premise licenses toward AI‑enabled, cloud subscription tools that deepen customer stickiness. The new AI tax and clinical workflow launches support that shift, but they do not meaningfully change the near term drag from declining print and nonrecurring revenues, or the execution risk around cloud migration and customer adoption.

The Ovid Synthesis collaboration with the American Board of Medical Specialties looks especially relevant, as it embeds Wolters Kluwer’s cloud software directly into clinicians’ quality improvement workflows and certification processes. This sort of integration can reinforce recurring revenue and help offset pressure from print declines and transactional revenue stagnation, but it also raises the stakes if healthcare customers become more sensitive to competing AI tools or pricing.

Yet while AI and cloud deepen Wolters Kluwer’s moat, investors should also keep in mind the growing risk that...

Read the full narrative on Wolters Kluwer (it's free!)

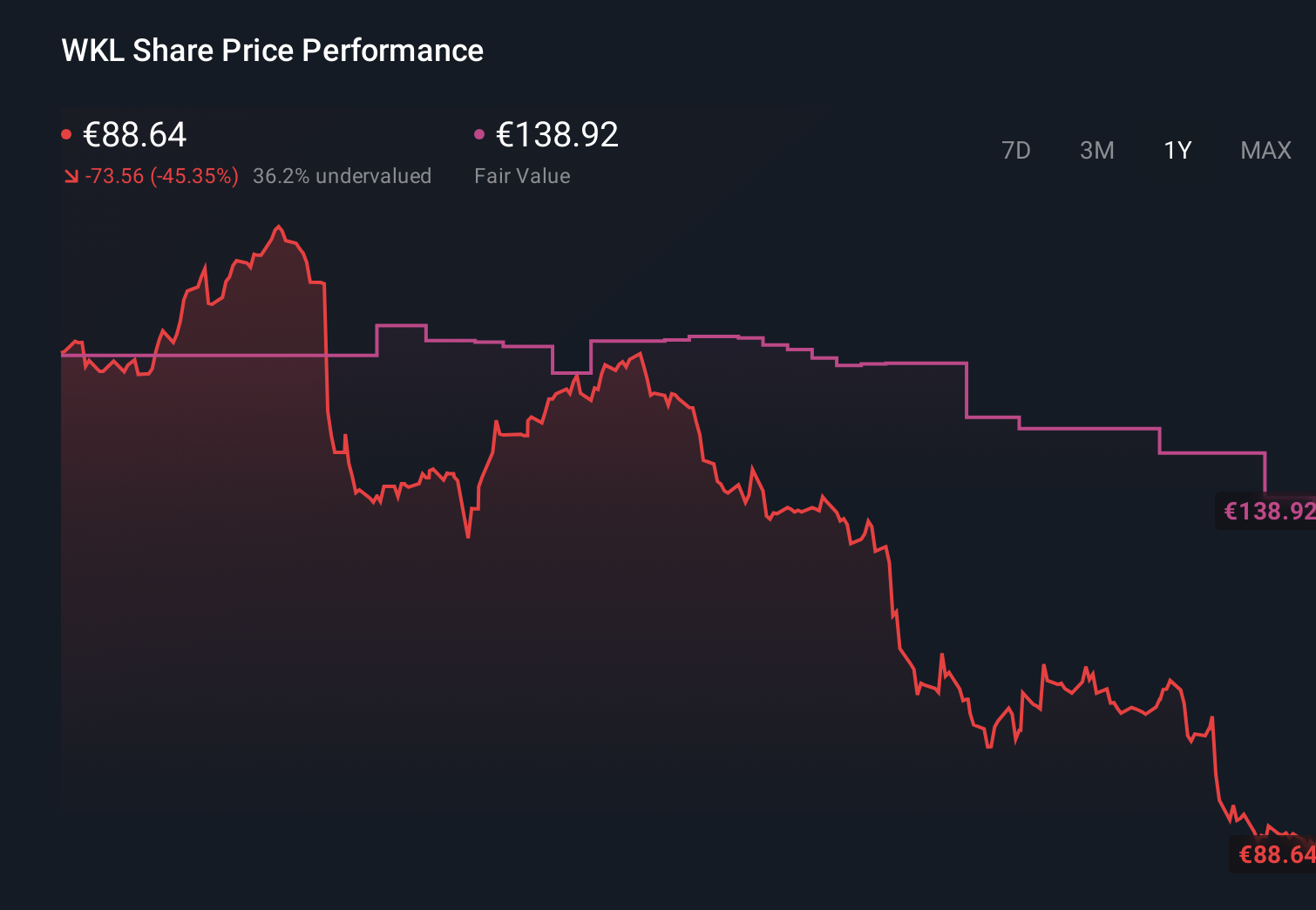

Wolters Kluwer's narrative projects €7.1 billion revenue and €1.4 billion earnings by 2028. This requires 5.2% yearly revenue growth and an earnings increase of about €0.3 billion from €1.1 billion today.

Uncover how Wolters Kluwer's forecasts yield a €138.92 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Seven members of the Simply Wall St Community see Wolters Kluwer’s fair value between €131.09 and €193.25, underlining how far opinions can spread. Against that backdrop, the ongoing shift from on‑premise licenses to SaaS and cloud, and the adoption risks that come with it, could be a key factor shaping how the company’s performance aligns with any of these views over time.

Explore 7 other fair value estimates on Wolters Kluwer - why the stock might be worth over 2x more than the current price!

Build Your Own Wolters Kluwer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wolters Kluwer research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wolters Kluwer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wolters Kluwer's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Wolters Kluwer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTAM:WKL

Wolters Kluwer

Provides professional information, software solutions, and services in the Netherlands, rest of Europe, the United States, Canada, the Asia Pacific, Africa, and internationally.

Very undervalued with proven track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)