Advertisement

Maxis Berhad (KLSE:MAXIS) has announced that it will pay a dividend of MYR0.04 per share on the 23rd of December. This makes the dividend yield 4.4%, which will augment investor returns quite nicely.

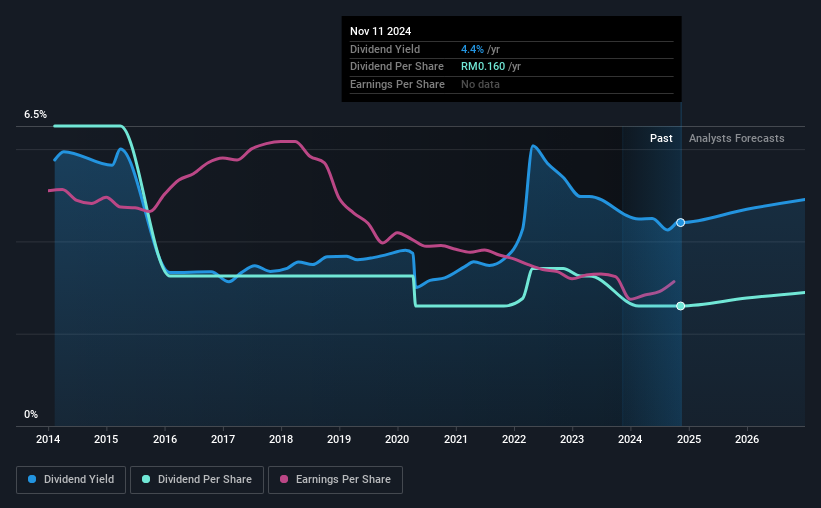

See our latest analysis for Maxis Berhad

Maxis Berhad's Payment Could Potentially Have Solid Earnings Coverage

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Prior to this announcement, the company was paying out 111% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 56%. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

Looking forward, earnings per share is forecast to rise by 71.3% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 59% which would be quite comfortable going to take the dividend forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the annual payment back then was MYR0.40, compared to the most recent full-year payment of MYR0.16. Doing the maths, this is a decline of about 8.8% per year. A company that decreases its dividend over time generally isn't what we are looking for.

Maxis Berhad May Find It Hard To Grow The Dividend

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. It's not great to see that Maxis Berhad's earnings per share has fallen at approximately 4.6% per year over the past five years. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

Maxis Berhad's Dividend Doesn't Look Sustainable

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 2 warning signs for Maxis Berhad that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MAXIS

Maxis Berhad

An investment holding company, provides a suite of converged telecommunications, digital, and related services and solutions in Malaysia and internationally.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor