We Think Cuscapi Berhad (KLSE:CUSCAPI) Needs To Drive Business Growth Carefully

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So should Cuscapi Berhad (KLSE:CUSCAPI) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business's cash, relative to its cash burn.

View our latest analysis for Cuscapi Berhad

Does Cuscapi Berhad Have A Long Cash Runway?

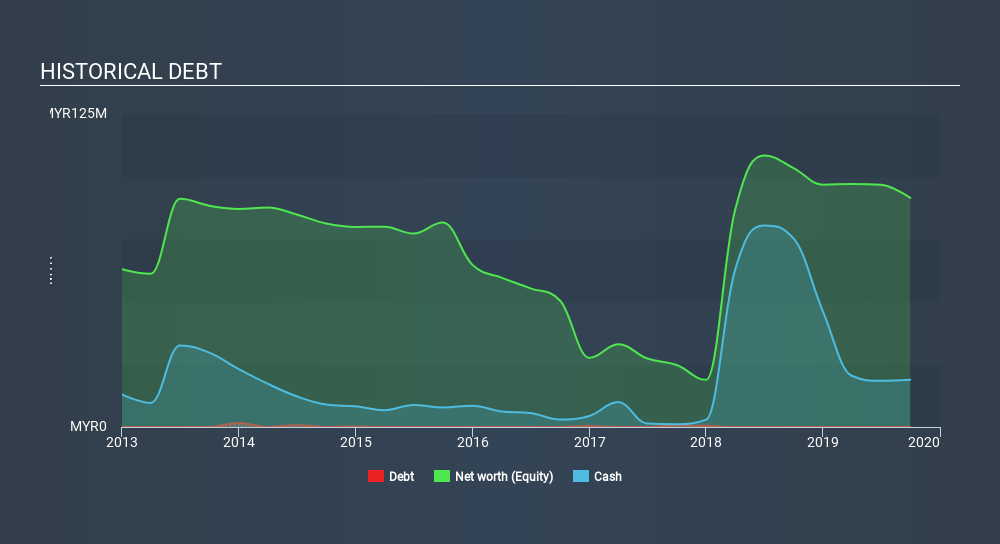

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at September 2019, Cuscapi Berhad had cash of RM19m and no debt. Looking at the last year, the company burnt through RM29m. Therefore, from September 2019 it had roughly 8 months of cash runway. That's quite a short cash runway, indicating the company must either reduce its annual cash burn or replenish its cash. The image below shows how its cash balance has been changing over the last few years.

How Well Is Cuscapi Berhad Growing?

Some investors might find it troubling that Cuscapi Berhad is actually increasing its cash burn, which is up 26% in the last year. Also concerning, operating revenue was actually down by 16% in that time. Taken together, we think these growth metrics are a little worrying. In reality, this article only makes a short study of the company's growth data. You can take a look at how Cuscapi Berhad has developed its business over time by checking this visualization of its revenue and earnings history.

How Easily Can Cuscapi Berhad Raise Cash?

Cuscapi Berhad revenue is declining and its cash burn is increasing, so many may be considering its need to raise more cash in the future. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of RM150m, Cuscapi Berhad's RM29m in cash burn equates to about 19% of its market value. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

Is Cuscapi Berhad's Cash Burn A Worry?

On this analysis of Cuscapi Berhad's cash burn, we think its cash burn relative to its market cap was reassuring, while its cash runway has us a bit worried. Summing up, we think the Cuscapi Berhad's cash burn is a risk, based on the factors we mentioned in this article. For us, it's always important to consider risks around cash burn rates. But investors should look at a whole range of factors when researching a new stock. For example, it could be interesting to see how much the Cuscapi Berhad CEO receives in total remuneration.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:CUSCAPI

Cuscapi Berhad

An investment holding company, engages in the software development business in Malaysia and rest of the South East Asia.

Flawless balance sheet and fair value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)