Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:EMETALL

Eonmetall Group Berhad (KLSE:EMETALL) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Eonmetall Group Berhad (KLSE:EMETALL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Eonmetall Group Berhad

How Much Debt Does Eonmetall Group Berhad Carry?

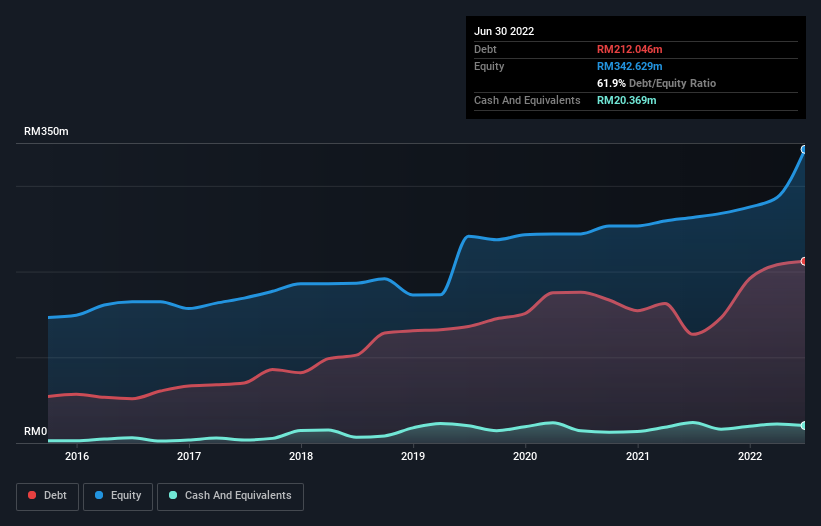

You can click the graphic below for the historical numbers, but it shows that as of June 2022 Eonmetall Group Berhad had RM212.0m of debt, an increase on RM126.8m, over one year. On the flip side, it has RM20.4m in cash leading to net debt of about RM191.7m.

How Healthy Is Eonmetall Group Berhad's Balance Sheet?

According to the last reported balance sheet, Eonmetall Group Berhad had liabilities of RM289.1m due within 12 months, and liabilities of RM41.1m due beyond 12 months. On the other hand, it had cash of RM20.4m and RM130.7m worth of receivables due within a year. So it has liabilities totalling RM179.2m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's RM172.9m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Eonmetall Group Berhad's debt is 4.3 times its EBITDA, and its EBIT cover its interest expense 6.2 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Pleasingly, Eonmetall Group Berhad is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 103% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Eonmetall Group Berhad will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, Eonmetall Group Berhad saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Mulling over Eonmetall Group Berhad's attempt at converting EBIT to free cash flow, we're certainly not enthusiastic. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Eonmetall Group Berhad's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for Eonmetall Group Berhad you should be aware of, and 2 of them don't sit too well with us.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Eonmetall Group Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:EMETALL

Eonmetall Group Berhad

An investment holding company, manufactures and sells metalwork machinery, industrial process machinery and equipment, and steel products.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor