Advertisement

Asia Poly Holdings Berhad (KLSE:ASIAPLY) Soars 31% But It's A Story Of Risk Vs Reward

Asia Poly Holdings Berhad (KLSE:ASIAPLY) shareholders would be excited to see that the share price has had a great month, posting a 31% gain and recovering from prior weakness. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 5.6% over the last year.

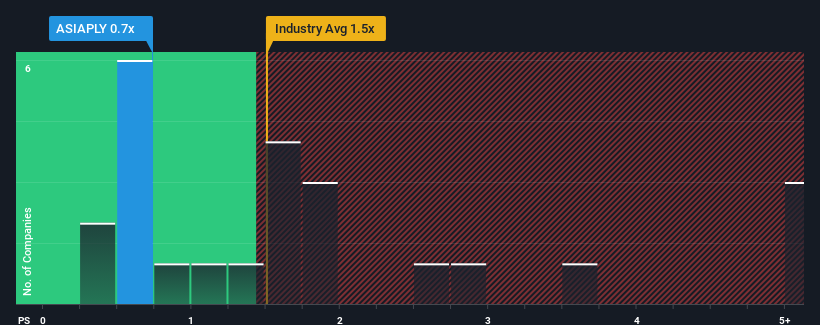

Even after such a large jump in price, considering around half the companies operating in Malaysia's Chemicals industry have price-to-sales ratios (or "P/S") above 1.5x, you may still consider Asia Poly Holdings Berhad as an solid investment opportunity with its 0.7x P/S ratio. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Asia Poly Holdings Berhad

How Asia Poly Holdings Berhad Has Been Performing

The revenue growth achieved at Asia Poly Holdings Berhad over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Asia Poly Holdings Berhad's earnings, revenue and cash flow.How Is Asia Poly Holdings Berhad's Revenue Growth Trending?

Asia Poly Holdings Berhad's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 20%. The strong recent performance means it was also able to grow revenue by 38% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 5.5% shows it's noticeably more attractive.

With this in mind, we find it intriguing that Asia Poly Holdings Berhad's P/S isn't as high compared to that of its industry peers. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Key Takeaway

Asia Poly Holdings Berhad's stock price has surged recently, but its but its P/S still remains modest. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We're very surprised to see Asia Poly Holdings Berhad currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see robust revenue growth that outpaces the industry, we presume that there are notable underlying risks to the company's future performance, which is exerting downward pressure on the P/S ratio. It appears many are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Asia Poly Holdings Berhad (2 can't be ignored!) that you need to be mindful of.

If you're unsure about the strength of Asia Poly Holdings Berhad's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ASIAPLY

Asia Poly Holdings Berhad

An investment holding company, engages in the manufacture and sale of cell cast acrylic sheets.

Slight with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor